1/1/2015

guest I don't think these predictions can be stated as a fact today, currently TSLA only produces a rounding error of worldwide cars. Toyota and VW Group will each produce about 10+ million cars a year by the time TSLA introduces its Gen III car in 2017.

More general, the IT and car industry can't be compared directly imho. The other two disruptors mentioned (Gates and Jobs) both worked in IT. In IT, you can scale up production and distribution very quickly, that's hard to do in the car sector, it will take TSLA years to scale production and add more factories. (In extreme cases, such as eletronic software, the marginal cost of another unit in manufacturing and distribution is close to zero or zero).

Even assuming everything goes great for TSLA (tech licensing, stationary batteries, Gen III introduction etc.) all these revenue streams are far in the future and have to be discounted to present value. Damodaran, a noted expert on company valuation, arrived at a valuation of $68 billion using his assumptions, in present value, that's "only" around $8-9 billion - right now TSLA's market cap is above 20 billion as we all know. For more details, see my entry here:

Short-Term TSLA Price Movements - Page 1055�

1/1/2015

guest tftf you must be one of those people who who couldn't envision Tesla being where they are at now 1 year ago. You were proved wrong. Now you don't believe Tesla will make the next steps to become the biggest car manufacturer in the world? You will be proved wrong again...these next steps in comparison will be much easier for them to overcome than everything they've overcome in the past 5 years.

As long as their product remains the best in the world I have no doubt they can execute to get where Sleepy says they go.

goodluck with your short position as us longs don't mind taking your money in the long run.�

1/1/2015

guest Believe it or not, I was long TSLA one year ago when it was trading below $30 (and don't regret selling when it reached my PT this year). I can switch my opinion depending on company valuation. This is not about me, however. Please take a look at the link and the numbers provided by Damodaran, few analysts did such a proper and detailed DCF analysis - and even provided for free to the general public. He also added general lessons and potential pitfalls regarding young companies:

Musings on Markets: Many a slip between the cup & the lip: From forward value to value per share today

In contrast to me, he certainly has no incentive to "talk the stock down" as he states himself:

(quote from link above)

Anyway, whenever I'm long I read what the shorts have to say and vice-versa. So I spent some time on this forum and presented my views.�

1/1/2015

guest

I am long Tesla. TSLA is nearly 100% of my portfolio and I believe they have a shot at being the world's largest automaker. From where I sit, tftf was merely pointing out that this outcome is not a certainty. And guess what, it's not. A lot can happen between now and 2018, much as I believe in Tesla and believe they can keep up the jaw-dropping execution.

I don't think it's constructive to jump down the throat of anyone who has a differing take on Tesla's prospects. I, for one, would prefer a forum where we could exchange differing opinions civilly.�

1/1/2015

guest You don't regret missing out on huge gains? I've seen other former longs who bailed out too soon and can't come to terms with what the stock has been doing, and will do in the future.�

1/1/2015

guest Exactly, I was simply trying to explain a different viewpoint using numbers: Damodaran is an independent academic (not a short-seller) and a noted expert on company valuation. I think it would be useful to have a detailed look at his blog entries, some people may not be familiar with the follow-up entry Damodaran wrote a few days after his initial two blog entries on TSLA, it's linked above.

I was not here to pick fights. On a "fan" forum such as this one, I assume 90%+ of people are probably long TSLA, however: This can lead to a dangerous herd thinking and over-optimistic group mentality regarding TSLA's valuation and outlook, especially after the run TSLA already had in 2013.

It may be useful to hear a dissenting voice. Damodaran (which I frequently linked here) knows a thing or two about valuation. This doesn't mean you have to follow him (or anyone else) blindly - but I think he presented more useful number crunching and deeper analysis than most analysts covering TSLA's valuation - long or short. And it's all available for free on his blog. But apparently that's "trolling". Does this mean Professor Damodaran is (also) a troll, since I'm just linking to his numbers ?

With that said and no intention to start arguments: 42 entries were enough to present my points and point to a few links with (imho) red flags regarding TSLA's current market valuation. So long and thanks for all the fish arguments! We will see in a few year.

PS: @JRP3. I have been in the markets long enough not to get emotional over trading or investment opportunities. I never marry a stock, a new opportunity comes along each and every day in the markets.

PPS: @PeterJA. I was just pointing out size and production differences in the car market, not implying TSLA would be the largest manufacturer by 2017. I know that's impossible, in fact that is one my arguments: the car market is very different than, say, the IT market where a disruptor such as GOOG or AAPL can disrupt the sector in just 3-5 years with a new search engine or mobile phone. For example, it took all the Japanese and Korean car manufacturers aggregated (even with hidden and open subsidies from the governments in Japan and South Korea!)a few decades, not just a few years, to mount a successful assault on Detroit...

2000: GOOG marketshare in search engines

2005: GOOG marketshare in search engines

2008: AAPL marketshare in smartphones

2013: AAPL marketshare in smarthones

2013: TSLA marketshare in cars

2018: TSLA marketshare in cars

I will let you fill in the numbers...

@PeterJA: Regarding the $68 billion and cost of capital. I already noted above why I think Damodaran's default cost of capital numbers are appropriate and the low 1.5% yield in May 2013 was only possible because the yield was linked to a convertible bond, not a "normal" corporate bond, again here:

Short-Term TSLA Price Movements - Page 1055�

1/1/2015

guest tftf, I don't follow your logic. You quoted Sleepy saying: "Tesla will be the biggest car manufacturer in the world, and it will happen a lot sooner than you expect."

You disagreed, using the following arguments:

as if Tesla's current size is somehow relevant to its potential size.

as if Sleepy said Tesla will be the world's largest in 2017, which he did not. Obviously, Tesla is unlikely to sell millions of Gen3s in the year the car is launched.

If that is your thought process, I have to be skeptical of your conclusions.�

1/1/2015

guest DHA,

dont kid yourself, not everyone on here is as honest and innocent as you might hope. It's ok in my book to take some jabs at these trolls from time to time, though some argue that it encourages them more (hence the saying "don't feed the trolls").�

1/1/2015

guest Julian Cox wrote a brief critique of Professor Damodaran's assumptions, and has promised a more detailed critique. You can find the former here:

Short-Term TSLA Price Movements - Page 1033�

1/1/2015

guest Exactly.

He says that TSLA is worth $6b-$8b according to his calculations. TSLA will have ~$5b in sales in next year. There is not one logical investor in the world that thinks TSLA deserves a 1.5x forward price/sales ratio; for a $billion company growing sales by 100% year over year over year over year. 15x forward price/sales ratio (and a $75b market cap) would be a lot more logical than 1.5x. Not saying that it deserves 15x, but I could understand someone trying to make that argument. 1.5x is just trolling.

And for all those non-believers out there, in the absolute worst case (excluding any force majeure events) Tesla will have $3.5b. There is no way you can justify a 2x price/sales ratio. You have to be a troll to write this.

BTW, DCF's are garbage: extremely sensitive to inputs. And nobody has the right inputs, not even Elon himself.�

1/1/2015

guest My father instilled in me the belief that I could accomplish anything I set my mind to. The high mileage of life has tempered my passion and beliefs. The last several years, I worked as a solar power inspector for the City of Los Angeles. I made it a point to ask each of customers why they had invested in solar. One very elderly lady made a tremendous impression on me. She emphatically stated: "I am changing the world." Elon Musk, is by stated goal "changing the world."

I thinks this begs the question. Can we change the world? Can an individual, through his actions, change the world? At nigh on sixty years of age, I have grown to realize what you do matters. Your actions ripple throughout the world. Elon Musk, and the Tesla community (we) are changing the world. Changing the world is a passionate, angst-filled, acrimonious business.

In my quiet reflections, I am astonished at the level of civility. Especially, considering the fortunes that have changed hands, and those that will.�

1/1/2015

guest Very well written Jack.

Are we related? My Dad told me the same thing!

Each and every Roadster and Model S owner out here is autonomously changing the world. Elon is our catalyst.

The world needs more catalysts.

Whenever I listen to John Lennon's song, Imagine, I want to add to the lyrics, ...

Imagine no oil

I wonder if you can

No gas stations, refineries or pollution

A brotherhood of man

Imagine all the people

sharing solar / wind energy...

The beauty of this is that our goals are realistic, obtainable and inevitable.

The rest of his song, while admirable ... utopia.�

1/1/2015

guest And yet Tesla is already disrupting the industry by building a car that is so universally well received that OEM's such as GM are admittedly studying what Tesla is doing. The ultimate time frame may be longer but the potential for disruption is no less.�

1/1/2015

guest Just returned from a party in OC where I was talking to a friend of a friend of mine who owns a company that turbo-charges engines for the auto majors in LA. Naturally Tesla came into the conversation. He thinks electrics are the future and his time in the business is limited.

It is hard to be fully convinced yet if Tesla will become the largest automaker 15 years from now but they have all the ingredients for a good shot at it if they want to be. They more likely will grab a 2% to 5% market share ($ 90 to $100 billion annual revenue by then for Tesla), which can still make them a very large market cap company if they are still growing.. $200 Billion + market cap, IMO.�

1/1/2015

guest Tesla is definitely at a defining point these next few years. I am long TSLA so I am hoping they are the apple of the auto industry. They don't need to sell the most products as long as they can maintain a high end product that people are willing to pay a premium for. Apple seems to be doing okay even after losing market share. Yes there stock is down from its all time high, but that high was unreasonable and had no basis. All us long investors should hope Tesla is the next apple, they're up about 6000% over the past decade, hopefully TSLA will do the same for us and well be driving "free" teslas for years to come.�

1/1/2015

guest If the point of this thread is to refine our thinking about the right valuation of Tesla, then reasoned arguments from both sides should be welcome. I think cautious/skeptical viewpoints are too often dismissed out of hand, with some hostility in the tone of the responses. This turns this thread into mutually reinforcing backslapping for everyone who has "seen the light". This is a pity, because this forum used to be a great source of insight into the stock.

I firmly believe that Elon is changing the world. Even accepting that premise, I am uncertain about what stock price for Tesla is supported today. The following are uncertainties that must be taken into account:

* The probability of success (it is not 100% - business success is always a combination of skill and luck)

* The role of Tesla in that changed world (some companies have changed the world without retaining a lucrative market share)

* The strength of the IP, and the possibility that alternative technological platforms could leapfrog it in the EV market

* Production and supply chain ramp-up - how long to go from 25k/year to 100k and 1m per year? This is hugely underestimated on this forum I think.

* Competitive response (yes, it is pathetic now, but the investor graveyard is full of people who believed that competition would not wisen up)

* Political risks (backlash against EV incentives too early)

* Dillution

* Freak risks (something happens to Elon, factory fire, safety issue with tech, etc. etc.)

On top of all this, I have no idea what a realistic success scenario looks like - 400k or 4 million cars in 10 years? What is ASP? What are the margins? And I need to keep in mind that a decent 10% rate of return over those 10 years means that today's share price should be only ~40% of what it will be then.

Taking all this together, I am very uncertain whether Tesla's great prospects are worth $10bn, $25bn or $100bn or more.

The higher the stock price rises, the higher is the probability that we have passed the right level. (Please do not argue with this, because it is an obvious truth of investing.) The real goal of this thread should be to come up with estimates of what each share is worth. This is a territory that I have not seen any of the bulls (Sleepyhead and so forth) venture into. The reason is of course that it is extremely hard and any numbers you put in will be very uncertain. However, the right response to that uncertainty is not to dismiss DCF models, but to run them again and again with different assumptions to understand the dynamics of the valuation based on the key assumptions. I get really worried when price/sales ratios come up, because that is a valuation metric that has been misused grossly in the past.�

1/1/2015

guest Great points, DonPedro.�

1/1/2015

guest While I agree that the voice of reason ought to be a central part of this community. We also take a narrow view of Teslas' products and future. In one sense, the name Tesla Motors should be changed to simply Tesla. As an energy storage company Tesla is capable of disrupting far more than the automotive and petroleum industries.

I see the electric utility industry as the proverbial dinosaur. Distributed generation will very quickly become distributed entrepenuership. The largest solar companies in America are Walmart, and Costco. Both companies state that their investments in solar power provide them with a competive edge. Interestingly, as firms invest in renewable energy and green technologies their stock values increase.

LED lighting, electrical energy efficiency products, renewable energy, and energy storage will enable businesses and individuals to control their own energy futures. The transformation to a "Solar Electric Economy" will provide Tesla with phenomenal product growth. We have only scratched the surface.�

1/1/2015

guest Don Pedro, I agree. Civil debate of information, and the way we each look at that information, is a good thing. While I am bullish on TM and feel that it is still an excellent investment I know that much of the valuation is based on continuing to deliver products flawlessly. TM has done this so far and I believe it will continue to execute the stated long term plan very well.

While I have been part of this and the TM forum for only sevral months, I find myself spending more time here versus the TM forum because of the almost maniacal 'troll hunting' that goes on at that forum.

Just as we have all argued for open dissemination of information about production rates, etc., we should also welcome opinions that differ from our own as part of that open dissemination of information.�

1/1/2015

guest I don't think any of us have an issue with well reasoned counter arguments. However they have been few and far between.�

1/1/2015

guest Posted this at the alternative thread, but I guess its also important here: France is banning fracking, which is good. "And that�s not just talk. France has ambitious goals for a low-carbon future and is currently considering a tax on carbon emissions and a nuclear tax. Revenue would go to renewables and energy efficiency standards. France plans to cut fossil fuel use by 30 percent by 2030, at the same time that it de-emphasizes the nuclear power that provides three quarters of the nation�s energy." This is what I have been talking about, countries will follow Norway and the others that will benefit renewable energy and EV cars.

Read more at http://cleantechnica.com/2013/10/14/frances-ban-fracking-absolute/#C9ktwo7mkrLTUr5Q.99�

1/1/2015

guest Again, it would be easier to have a discussion about valuation, not "pro" and "counter". I may be "pro" at a share price of $160 and "counter" at a share price of $220.

I thought the article tftf brought up is very interesting, and it would require a better refutation than "don't trust DCFs". To summarize the article:

1. Give Tesla a 90% chance to have the sales of Audi and the margins of Porsche in 10 years

2. Assume also that to get there they will need to issue a lot of equity to finance growth

3. Take into account that we buy the shares to make more than 1.5% per year (the author suggests 10%, which he says is a typical expected return on similar shares)

4. Take into account that there are many outstanding options (employees etc.) that will dillute existing shares

Then he gets this low valuation of $8bn.

To support a higher value today, you would have to disagree with some of these assumptions. Dismissing the framework is silly - there is no better framework available on this forum.

On my part, I would make several success scenarios. The capital requirements should be matched in each - quite good growth could be funded internally, while hyper-growth would require Tesla to raise a lot of capital. The terminal value should then be a probability-weighted average of the success scenarios. I would also add a value to non-car business opportunities (supercharger network, grid storage).

I think that 90% probability of astonishing success is an aggressive assumption - 70-80% might be more realistic (but what do I know).

I would also use a lower discount rate, but I would certainly not buy the shares to make less than 6-8% a year.

I haven't gone through this exercise, but an example could look something like this:

Value in 10 years

20% for $500bn, with 50% dilution from raising capital

30% for $200bn, with 40% dilution

20% for $60bn, with 20% dilution

10% for $30bn, with no dilution

This gives a terminal value of $98,6bn after adjustment for dilution.

Discounted by a 7% rate of return makes that a present value of $50,1bn.

Taking out debt gets us to $49.7bn.

Then the exercise price on outstanding options adds $21.20 * 25.06m = $0.5bn, but at the same time dilutes present shareholders by 25.06m on 121.45m shares.

I then end up with a valuation of ($49.7bn + $0.5bn) * 121.45/(121.45+25.06) = $42.6bn. This example then supports a share price of $351.

Note, however, that this example makes some pretty exuberant assumptions about the future of the company. We have assumed that there is a 50/50 chance of Tesla becoming one of the biggest companies on the planet. The first scenario I set up came up with something close to today's share price.

Note also that for both these optimistic scenarios (which support investing in the stock), the best days are nevertheless gone. We have had a return of 5x in half a year now. The scenario above say that we can get 2x over 10 years, on top of a typical mutual fund rate.

I would love to hear your probability-weighted success models, which is clearly what drives the valuation.�

1/1/2015

guest

We had a thread dedicated to this. FWIW, I don't recall Damodaran having any scenario analysis, so I would not critique his model by introducing probability-weighted scenarios. NTTAWWT, but it sorta muddies the discussion.

The factors he implicitly or explicitly includes that are most relevant and obviously in contrast to likely future progress are, IMO:

1) pace of Operating Margin improvement, which Aswath has bumping along from an irrelevant -2% from the last 12 months, to 12% in 10 years. The reality is EBIT margins are already (in year 1 of his analysis) equal to where he models that number only reaching in Year 6. (I use lease-adjusted figure here b/c this is a FCFF model and cash EBIT margins are the relevant figure in this type of analysis). Increased EBIT margin all along the timeline substantially reduces the need for the capital raising.

2) Pace of revenue growth - Aswath uses a typical high growth in early years, low growth in later/mature years approach. With Tesla this leads to bad output because revenue will exhibit much less homogeneous growth rates because platform introductions introduce step-changes in revenues from year to year. Additionally, Tesla's revenue growth in year 1 is severely underestimated, because it works off a base that looks to Last 12 months, which includes a 6 month period where production was closer to 0 than current run-rates. NTM revenue is likely to be closer to $2.5 Billion, a 90% growth rate, versus the 70% growth rate in his model. and so on, with the Model X launch in year 3, and the Model E launch in year 6/7.

3) ROIC - In this world of cash flow modeling that we've entered here, ROIC is probably at once the most important and least estimate-able metric in the model. This is IMO the key debate point over which TSLA from $160 will live or die. If this turns out to be just another auto manufacturer with huge capital intensive spending needs and low returns on that investment, then that will mean low ROIC, because tesla will have lower margins, higher annual reinvestment needs, and negative free cash flow for many years versus what is needed to justify current prices. On the other hand, if tesla ends up with substantial brand power and well-spent R&D, that will lead to sustainable and high EBIT margins, lower reinvestment needs, positive free cash flow earlier on, and therefore high ROIC and less need for dilution from capital raises.

When I putz around with his model and insert margin and reinvestment rates that are more in line with a brand power and R&D intensive vs. capX intensive firm, the outputs change quite dramatically.�

1/1/2015

guest Agree with most of what you wrote so could you share your estimate based on his model, but with more realistic numbers. A conservative, medium and optimistic approach would probably be the three model points to use for estimates.�

1/1/2015

guest Yes, and that is why I said DCF's are useless. I don't want to go into debating this topic, but they really are useless if you are trying to come up with a fair stock valuation for a stock such as TSLA. You can use a DCF to say that a stock cannot be worth $XXX.xx, but you cannot use a DCF to say that a stock is worth $YYY.yy. Prof. Damodaran even came out with a follow-up article where he presented 3 seperate cases that all led to a TSLA valuation above $200. Using that same DCF model. Example, if you ran a DCF on CSCO in 2000, then you would realize that the company would have to grow sales to $4 trillion within 10 years to justify its valuation. That is when DCF's come in handy, and not to come up with a fair value today.

Wall St. analysts come up with a price target in their head and then force the numbers into a DCF to match the price target, so they can say, "see my DCF model says it is worth $ZZZ.zz." It is not the other way around, which makes DCF's useless.

Oh, did I mention that DCF's are useless if you are trying to use a DCF to come up with a price target? DCF's are only good for academic purposes.

Sorry for being so blunt here, but I am trying to save you guys the headache (and wasted time) of running a DCF model to come up with an investment decision.

@DonPedro - thanks for being the voice of reason here and your posts are very well articulated, very reasonable, and greatly appreciated. When you look at tftf's latest post, it might even seem reasonable. But when you look at his whole body of work, then you know that he is just trolling.

I know that price/sales ratios are dangerous but in the case of a high margin, fast growth, but still small EPS business, such as Tesla they do make sense. Especially since the company is running pretty much at break even. Price/Sales ratio is the perfect metric to use for Tesla right now; or at least significantly better than using a P/E ratio, price/cars sold ratio, or whatever other ratio FUD analysts use to say the Tesla is overvalued.

And lastly, I wanted to point out that DaveT has made several extremely long posts about his expectations for TSLA's future stock price, and I (and many others) have done so as well. We all laid out a case where the stock could realistically reach $500 within a few years, and even more after that. I don't feel like writing the same things over and over again, because they get lost somewhere on page 697 of the short-term thread and nobody ends up reading them. That is why I started writing my own blog articles, so that people can easily find what I think, if they are interested in those kinds of things.

Let me just lay out a simple valuation for TSLA:

2013

24K cars sold

$2.5b revenue

$1 EPS

2014

50K cars sold

$5b revenue

$5 EPS

2015

100K cars sold

$10b revenue

$12 EPS

2016

150K cars sold

$16b revenue

$18 EPS

2017

250K cars sold

$22b revenue

$25 EPS

2018

500K cars sold

$30b revenue

$30 EPS

Therefore in less than 5 years time you are looking at the fastest growing giga-size company in the world, which will command at least a 30x PE ratio (since Toyota right now has about 25x PE of the top of my head) and a $900 share price.

If you don't believe my numbers (which will certainly turn out to be incorrect) then plug in your own and come up with your own valuation. This is the proper way to value TSLA the stock, and not by using a DCF model.

In order to figure out if TSLA is a good investment, then you should be looking at how much the share price will be trading at at some point in the future and then calculate the APR to see if the potential reward is worth the risk. In my calculations I get a 400% return in 5 years. In my book that is worth the risk, so I invest in TSLA. If I thought I would only get 100% return in 5 years, then I would never buy TSLA, because the risk is high, with such an inflated share price using TTM data.

You cannot value a company such as TSLA using a DCF model. You cannot try to discount cash flows to present value to get a "fair" valuation to decide whether the stock is a good buy. You should be forward looking and doing the math the same way I presented above.

Put your own numbers into my "model" and come up with your own valuation.

BTW, based on my "model" you can clearly see that at the end of 2014 the forward (i.e. 2015) sales will be at $10b with an EPS of $15. If you apply a forward P/E ratio of 30x or a forward price/sales ratio of 5x then you can see a clear path to getting a $400 price by the end of 2014.

There you have it, my 12 month price target for Tesla is $400 and as long as there are no force majeure events or fundamental changes in the global economy, I am comfortable with my price target and I base my investment decisions on what I think will happen.

Do your own due diligence, and don't let people like Damodaran or sleepyhead influence your investment decisions. Just please do not use a DCF to argue TSLA's valuation.�

1/1/2015

guest Sleepy, please copy your long posts and articles (including this one and your China article) to your TMC blog. I am very interested in them, but don't know where they are, and I don't want to support a site (Investnaire) that takes down your work without warning.�

1/1/2015

guest I wrote that a couple weeks back, when i was fiddling around with Damodaran's spreadsheet. I didn't save any of it tho, sorry. You can adjust to your heart's content though, here. Just for kicks I put in 1) a 6% EBIT margin in year zero (which he has slowly rising to 12% in year 10), 2) adjusted the sales/capital rate (the measure of required capital intensity to create an additional dollar of sales) to 2.5 (the global auto parts average) from his 1.4 (the global auto mfrs average), and 3) adjusted the tax rate to 25% (Ford's tax rate) instead of his 35% (just a default so far as i can tell).

The output with these 3 adjustments went from his original $67 to a new present value of $214.

This is all to say not that TSLA is worth $214 or $67, but that the model is not some solid proof' of overvaluation or any such nonsense that the media made it out to be at the time.

I believe if you are trying to invest successfully for the long-term in an innovative disruptor, then scenario analysis is the wrong tool to use. You will almost always find the current price overvalues an intrinsic value estimate that incorporates low/mid/high estimate of future success. This is the case for a number of reasons, not least of which is that successful disruptive firms have a habit of so far exceeding any 'reasonable' estimate of future success.�

1/1/2015

guest View attachment TSLA v2.0.xlsx

I've attached a spreadsheet that outlines TSLA's performance through 2022 in what I think are going to be the demand figures moving forward. There's multiple tabs that either outline the Conservative/Aggresive/SuperAggresive demand models, plus other miscellaneous stuff that I'm working on with historical data.�

1/1/2015

guest One thing that people fail to realize about Tesla is that it's real potential is in battery storage. A lot more margin with a lot less hassle and a lot bigger addressable customer base than selling cars.�

1/1/2015

guest OK, fair enough. I appreciate the balanced responses, and I will withdraw much of my criticism.

I will not flaunt credentials, but I have a decent background for doing valuations. I think you make a poor case against DCF (you say you don't want to debate, but since you go on to do so I will respond):

Your argument, if I understand it correctly, is that you can get different results with the DCF, based on which assumptions you put in. That criticism applies just as strongly to ratios such as P/E and P/S. The problem with all valuation approaches is that fundamentally, we are so uncertain about Tesla's future. The uncertainty about assumptions is not a property of DCF, it is a property of TSLA.

When you do a P/E, you just hide all that uncertainty in a ratio. The real strength of P/E is to benchmark the share price of one company to another that is similar. Tesla is, as we all agree, quite different from other companies. Therefore, ratios are just as uncertain as other methods.

You may throw out there that Tesla "should have a forward P/E of at least 30" and justify it with a comparison to Toyota, but that depends on an incredible amount of factors. To mention a few: Where is Toyota right now in its earnings cycle, will the market P/Es be at record levels then (as they are now), will the capital structure be comparable, etc. etc. I would posit that a reasonable argument could be made for any forward P/E between 12 and 40. Then add some uncertainty about the terminal revenues and about the margins, and there you go - you have the same uncertainties as in DCF. Ignoring/hiding those uncertainties does not mean they are not there.

Also, ratios pretend that stuff such as employee stock options, dilution and capital requirements do not exist. If you are going to use ratios, at least you must find a way of accounting for these factors.

I know many traders believe this. What I will agree is that DCF used poorly is worse than ratios used poorly. Many people see the complexity of the DCF spreadsheet, and think they have gotten a very precise result. Of course the certainty about the result cannot be greater than the certainty of the assumptions. However, people overuse ratios because they are so convenient and because they are hard to attack (how are you going to have a reasonable discussion about the P/E of Tesla in 2023? That must be the most speculative discussion ever).

This will not become more true by repeating it. The only argument you have raised against DCF remains sensitivity to assumptions, which as described above is also a property of P/E and other ratios. This is actually quite obvious - you can't get around "garbage in, garbage out".

It is nice that ratios work for you, but I do not find your arguments against DCF convincing at all. In any case, there is no reason to impose One Right Valuation Method on the forum. I will feel free to critique assumptions made in your ratio analyses, and I welcome critique of my assumptions for a DCF. All in mutual respect.

- - - Updated - - -

Yes, I agree very much (assuming you refer to grid storage). That is an opportunity that is very hard to value. One could think in this way: Imagine a startup with this technology already deployed at some sites, having a cooperation with Tesla Motors and being led by brilliant entrepreneur Elon Musk. What kind of valuation does it get for its Series C round? I would guess around $0.5-1bn. The VCs would target an IPO at $2-5bn in 3-5 years, and want to earn a 5x in case of success. But this is purely speculative - without knowing anything about the business model, target market size, costs and supply chain, you cannot say much about a business (there is some info in the thread where we discussed this, but I doubt it would be enough to do a valuation).�

1/1/2015

guest DCF is widely used by venture capitalists for valuation purposes of young and growing companies in addition to other tools. I don't think Sand Hill Road is for academics outside of reality. Somehow, the IRR of an investment has to be calculated. One shouldn't blame the tool for the output: Strictly speaking, the discounting should only reflect the time value of money, the cash flows should be adjusted to reflect the risk, for example using scenario analysis (risk and the time value of money should not be mixed). Damodaran did this in part in a follow-up using three additional revenue scenarios for TSLA.

I also take offense when I'm accused of trolling. Everybody can have a look at my 42 posts on this forum, I discussed the following topics:

1. Valuation numbers for TSLA using DCF analysis, mainly linking to work from Professor Damodaran (whose third blog entry on TSLA wasn't discussed here afaik, so I linked to it). I don't think any (bullish or bearish) paid TSLA analyst has posted such a detailed analysis - especially not for free on the Internet and including a spreadsheet (and later on a updated spreadsheet with three scenarios). If you know of any, please post it, thank you.

2. The high risks associated with the Gen III (mass-market) strategy and the question/suggestion why TSLA isn't raising more money while it's still available for cheap to execute on this strategy - or as an additional cushion for unknowns or new markets in tech licensing/stationary batteries, imho one can never have enough liquidity in the capital-intensive car industry; I also discussed an alternative, lower risk strategy: TSLA remaining a high-end niche manufacturer (Tesla becoming the Porsche equivalent in EVs).

3. The general risks in many stock markets as of late 2013 affecting TSLA and other momentum stocks (cheap FED money/quantitative easing drying up one day, other macro risks, current cycle could be ending soon with stock markets reaching 2007 highs again on nominal levels, eg. see here: A testament to the resilience of markets: World stock market capitalization is nearly back to pre-recession, pre-crisis levels | AEIdeas )

If you consider these three topics trolling, so be it. I only had the intention to add useful (granted critical, but reasonable) content concerning TSLA. In ending, I want to re-iterate once more that it can very useful imho to always hear/review the opposite view to one's holdings/positions when investing (minimize behavioral bias). It helped me a lot in the past - and that's why I was a reader on this forum and will continue to be, but won't be posting anymore.�

1/1/2015

guest Just a few peripheral observations-

Yes, building 500K/yr is different than 20K to 40K a year and is a non-trivial exercise. However, this is known stuff done by the likes of GM, Chrysler and Ford to name a few. If Tesla can pull off the unknown stuff like zero to 20K for MS then I have faith the same people can put their mind to poaching the right talent and replicating the feats of others. Not easy but doable.

If Tesla can pull off having Panasonic, Samsung and the like funding the increase in battery production to allow for 500k/yr of G3 then I am much more willing to believe in magic and, specifically, Tesla's ability to fund G3 without going to the market today. My fear was they were not going to the market today for a first bite at the $8B needed for battery capacity. I suspect the Q3 call will have input on future battery production given the recent raw materials production increases and Elon's comments on batteries not being an issue moving forward. If so, the issue will be put to bed.

WRT differing opinions, I appreciate and need them to learn. Please keep'm coming.�

1/1/2015

guest I think the big question about the pace of scaling up production. Scaling up very fast makes it hard to self-fund the expansion, and it also puts a strain on the supply chain that is hard to imagine if you don't work with this stuff.

I suspect Elon's base case is a somewhat slower buildup than people imagine. That is consistent with self-funding and with maintaining quality and margins during the growth. This is supported by the fact that Elon is referring to GenIII development as something they have briefly touched on lately (I don't remember the exact quote).

On the other hand, he is not one to let growth opportunities slip. I suspect that if the share price remains high, he may be tempted to try and grow even faster. But then he will have to raise cash - even Elon cannot conjure up cash magically.�

1/1/2015

guest

I'm not entirely sure Elon envisions a slow buildup of Gen 3. Keep in mind he has a standing bet that half of car production will be EV by 2030. And we all know by this point not to bet against Elon.

2014 production numbers will be very telling on the company's ability to scale up as they "test the depth of MS demand." Next, the roll out of the Model X will show how well they learned from the MS launch. Which I expect will scale up much more quickly and smoothly. If we look back at the Roadster days, no one could have predicted that Tesla could go from niche specialty car maker to legitimate mass production car company so quickly. Part of Elon's strength is his ability to make amazing business decisions at opportune times, which is not luck, but his ability to "play chess in 3D," as others have put. The last secondary offering was basically conjuring up cash magically, it was incredibly brilliant the way it was done. So, while many of the hurdles on the gen3 path seem insurmountable, I won't be surprised to see several more brilliant/unforeseeable business decisions up Elon's sleeve.�

1/1/2015

guest Just finished watching the latest SpaceX video. Elon is one-upping NASA...............and I'm irrationally exuberant. Really?

Energy generation, consumption, and efficiency (managed energy use) are core technologies of space travel. Tesla is the dove-tailing of Space X, Solar City, and Tesla Motors. The short argument is that Tesla doesn't have a moat. Tesla Motors is not a car company. It is the cornerstone of the "Solar Electric Economy".�

1/1/2015

guest I don't necessarily disagree. My point was only that I was recently surprised by his comments in a video posted on this forum, where he referred to GenIII development as something they had barely touched yet. That changed by outlook, because I thought they were seriously working on it already.

Also keep in mind that the Model X got postponed?, not accelerated.�

1/1/2015

guest Early projections were ~20k sales of Model S in 2013 and 35k combined Model S and X sales in 2014... I think Tesla postponed X solely because it became apparent that Model S most likely will sell more then 35k units in 2014, so there was no point in introducing X at the end of 2013.

And Tesla was, is and probably would be supply constrained, especially in terms of available battery cells production volume.�

1/1/2015

guest Panasonic is adding production lines in under 9 months, As far as I understand the production lines are highly automated and the material inputs are simple. The addition of cell capacity is expensive, but can be rapid and I think that government support for that would be available if necessary. What I'd be concerned about is getting supply for all of the other parts. The bigger the suppliers, the faster they can expand.�

1/1/2015

guest To clarify, Tesla production is not battery supply constrained in near to medium term. Panasonic is increasing their output at Suminoe plant to 300 million cells by the end of this year (linked below), which will cover more that 42,000 Model S. this dove tails with Tesla ramping up production to 800 cars per week in Q4. The Suminoe factory was originally designed to have two phases (linked below). Phase II will double capacity from 300 to 600 million cells, enough to cover 84,000 Model S's.

In addition to above Panasonic is also expanding production of small cells in at least one other plant in Osaka Perfecture.

As It Increases Production, Tesla Worries About Battery Supply - NYTimes.com

Panasonic's New Lithium-Ion Battery Plant to Start Mass Production Next Month | Headquarters News | Panasonic Global�

1/1/2015

guest This is still consistent with my point. I am guessing that the reason they are in no apparent rush to develop the GenIII is that they will be production constrained for Models S and X for quite some time.�

1/1/2015

guest Fun With Numbers

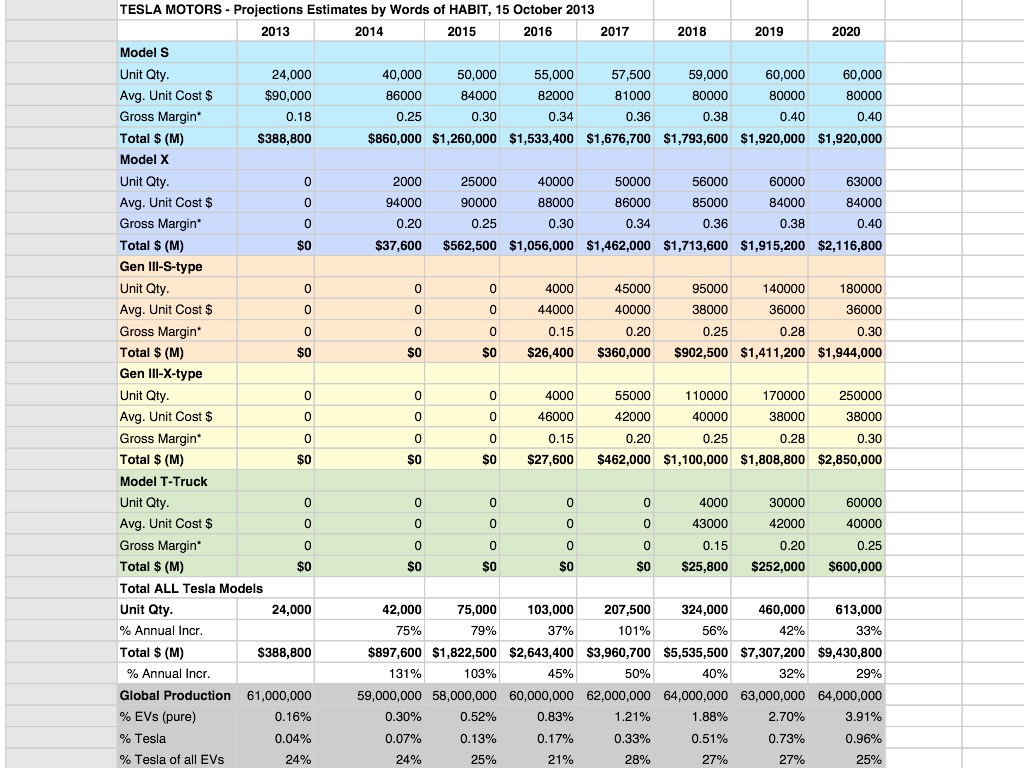

The contributors at TMC are awesome. Always a good read guys.

My guesstimate for Tesla is not as high as Sleepyhead, but here goes. All comments are appreciated, as this is my first attempt and I learn something new every day.

The simple spreadsheet below shows how Tesla can generate >$9B in Gross Profit on selling >600 thousand cars by 2020 while capturing less than 1% of the global auto market share. * Gross Margin excludes ZEV credits. The EV Revolution will not happen over night. Exponential growth figures really start to kick in after 2020. It will get really fun then. Time is on our side (just ask Shell). I believe.

�

�

1/1/2015

guest DCF: Less than 0.01% of investors know how to create a DCF

My method: more than 99.9% of investors can use it

DCF: Takes several hours to create

My method: took me less than 5 minutes

DCF: finds a fair value of today's stock price

My method: tries to see where the stock price is headed, so that you can make informed decisions.

Other than that, both methods are garbage in/garbage out.

It's just that my method is significantly better because anybody can use it and anybody can understand it.

I worked for the top ranked research shop and I can tell you that DCF's are useless; I already explained how analysts use DCF's. The only reason companies use them, that I can think of, is to protect themselves. If they lose a lot of money or give bad advice, they can show that they did all of the analysis.

In the time it takes you to create a DCF, I can research a dozen different companies and potentially find the next great investment, while you are plugging away at your 7% discount rate; and wondering whether you should have used a 6% or maybe 8% instead.

If you guys want to make money in the markets the read a lot, and then read some more. Don't be sitting in spreadsheets all day, that is wasting precious time that could be spent on reading. Read, research, look at financials, charts, and then read some more.

Use your time wisely.�

1/1/2015

guest �

1/1/2015

guest It's fun to make assumptions about future products, and it's a good exercise to see where things could go, however, it is difficult to make accurate predictions because there are so many factors that could change from now until the product is released.

But since the Model S has been selling for a bit we at least have some metric to go by to predict future trends. So considering your chart for the Model S, I think the average unit price is way too low. The Model S will be released in China starting in 2014 and so far reports are showing it to start at 1M rmb ($163k usd), so going forward there will be a large chunk of MS cars (depending on demand in China) that will be selling well over 100k. We will also see the roll out of more options and add ons that will add up. And also, lets not discount inflation over time. I'm not sure what this all calculates out to, but low 80's just seems way to low to me, and I would expect that to trend higher over time, not lower.

In the way of gross margin, I think 40% gross margin is very optimistic. Not saying it can't be done, but I want to see how gross margin changes over the course of 2014 before I judge how high it can go. I would be very happy with anything over 30%.

Thanks for the great chart, will be fun to come back to our guesses in the future to see how it goes.�

1/1/2015

guest �

1/1/2015

guest Words,

I believe demand for G3 will be much higher than the production numbers you show. If Tesla can supply and ramp to meet demand, I believe you will see much more aggressive deliveries.�

1/1/2015

guest Thanks for everyone's posts - it's a little refreshing to come back to the long-term thread after spending maybe a little too much time on the short-term and debt ceiling threads.

I could have included a bunch of the preceding posts, but the 3d chess comment resonated. What happens to projections and cash flow if everything is moved up 6 months?

When Model X was postponed:

1) Cars were coming off the line at about 200/wk,

2) There was a reservation list, but not a good idea of demand in the US, much less the rest of the world,

3) There were significant challenges with the supply chain to produce more cars,

4) TESLA not only had a negative balance sheet with $225 million in cash and $460 million in debt, they had negative gross margins on the cars they were producing....etc, etc. etc. They would have been fools to stay with their proposed 2013 rollout of X.

Contrast that to now:

1) Cars coming off the line at 7-800/week or 38-42k/year (as per Craig cfOH) - in the Q2 conference call Elon said they were going to solve the supply chain problems by Q1 or Q2 of 2014...I think he was sandbagging and they are, for the most part, solved - including the good information in previous posts about battery production coming online for 50-80k per year.)

2) Very good feel for demand in US and better feel for demand in Europe and Asia - I believe Elon is supply, not demand constrained. 42k of Model S in 2014 seems doable (with some reports of a goal of 51k).

3) A positive balance sheet, with over $750 million in cash, profitable quarters, approaching 25% margins and the potential to reduce some of the outstanding $460 million of debt if some of the convertible bondholders convert to stock - (note: the bond trading activity for the convertible bonds looks to be between 20-50% less than before the conversion date (http://finra-markets.morningstar.com/BondCenter/BondTradeActivitySearchResult.jsp?ticker=C593595&startdate=09/02/2012&enddate=09/02/2013). Increased Brand recognition, new stores, free marketing, supercharger rollout, experience with global deliveries, etc. etc.

Which gets me back to the 3d chess. I think Elon et al were prudent to delay Model X rollout until "late" 2014 in March of this year. Barring some engineering challenge, I think they would be fools not to accelerate the rollout to "early" or "mid" 2014 as part of their guidance for 2014. I think when Elon is talking about production rates, margin and supply chain, he is solving for S + X, while the analysts believe he is solving for S. If it is solving for S + X then that = $ for shareholders as a "mid" 2014 rollout would potentially mean 42,000 S + 10 - 15,000 X =52-57k production for 2014 and a bigger lever to move the logistics, plants, supply chain, etc for gen3.

Fun to think about....�

1/1/2015

guest Agreed here..

I am an average mid income household - already committed to Gen 3

Have had a discussion with a few others - and after checking out Tesla - they too are committed to Gen 3 as soon as it hits market.

The average person (Like me) currently has no clue what Tesla is all about...The few that do think it is a $ 90,000.00 car - out of their reach

(I knew nothing about Tesla 3 months ago)

Once the average consumer gets educated - they will be lining up in droves for the Gen 3...

All the Camry, Accord, Mazda 6 people will have to seriously consider the Tesla

Production will be the limiting factor.

Just my 2 cents�

1/1/2015

guest Very fun indeed...�

1/1/2015

guest None of these points are in any contradiction to my proposition, which is that a properly done DCF is valuable. And I would say that 99.9% of investors have no idea what they are doing when they use a P/E, either (as evidenced by a gazillion "short TSLA" articles on Seeking Alpha).

I really don't see this point. Both are valuation methods, so they are doing the same. The difference is that ratios depend on heuristics while DCF depends on detailed assumptions (both approaches with their very important pitfalls). The only difference in the output is that by using P/Es taken from the current market, you get a market bias (which is what you want for doing a long/short strategy - e.g. long TSLA short TM) - but not necessarily if you are only going to going long without a hedge.

This is like saying the violin sounds horrible, because you've heard the neighbor's daughter practice. You put a 20-something with some Excel skills to value a company, you get what you deserve.

I think there is a lot to P/E analyses, but the best is to be fluent in many tools. I think the DCF analysis we started the discussion on here contained some interesting assumptions that could potentially be very important to a valuation of TSLA, and that your P/E analyses would completely ignore. Is it really your view that it is irrelevant for Tesla's share price whether the capital requirements for expansion will be $0 or $43bn*), or whether there are 0 or 25 million employee options outstanding? If not, then saying that a P/E is all that matters is to have a big blind spot.

These days I am not interested in other companies than TSLA, so I am happy to spend some time getting my judgments right. If you want to base your decisions on what you can do in a few minutes, that is fine for you. But it is not a good basis for dismissing information.

*) I am not saying I agree with the assumptions of Prof. Damodaran, just pointing out that the P/E analysis more or less assumes that these assumptions don't matter.

- - - Updated - - -

Very fun. What I am wondering about is how this will be solved for S + X + GenIII (or should we say S + X + E now?).

The paradoxical conclusion (at least on 1st order logic) is that as long as they are production constrained on S + X, they would postpone the GenIII. Think about it - is it more profitable to sell 30k more S/X a year or 30k more GenIII?

I think this is why they don't seem to be in a hurry to develop the GenIII. If they went full steam ahead on it now, they would be ready with it before they would be able to satisfy that extra demand. Better to ramp up only on S+X as long as there is sufficient demand. In the mean time, batteries only get cheaper and superchargers get more numerous, which improves the value proposition for the GenIII.�

1/1/2015

guest DP,

I think the initial demand for G3 will dwarf S and X. It will be a huge discontinuity in production capacity thus a push one year either way is not important. Irrespective of S and X volume, Telsa will either be prepared for an order of magnitude increase in production or they will not. I think G3 production is directly tied to cell availability and little else.�

1/1/2015

guest [post on impact of gov't shutdown was moved to Government Shutdown/Debt Limit - Issues and Timelines for Investors ]�

1/1/2015

guest Considering Audi's stock price remained constant the last 2 or 3 years, and assuming it wouldn't grow very much in the next 10 years either, what happens if you apply DCF to it?�

1/1/2015

guest I am not quite sure what you are asking here... Could you rephrase your question?�

1/1/2015

guest It seemed to me that one of the assumptions was that Tesla would grow to the size of Audi (with Porsche's margins), and then calculate the future stock price on the assumption that Tesla would just remain at that level, without further expectations of growth. (The scenario that EVs will remain a niche product, more or less).

So I am wondering how this method, in general, evaluates the share price of a company that has a certain level of revenue, but doesn't grow anymore.�

1/1/2015

guest I asked a few pages back, but never got an answer. Does anyone think that the government shutdown also affected Teslas ability to produce/sell cars? Registrations, customs what not. As I've understood a lot of things were standing still during the shutdown and it's a full 2 weeks of Q4. Just curious.�

1/1/2015

guest not sure about customs and international shipments, but with regard to US registrations, they are run by a state agency (in california it is the DMV), so they were not affected.

surfside�

1/1/2015

guest Yesterday I had a friend who is a long time skeptic break down and tell me he's thinking about getting one and wanted a test drive. I gave him one and he said he's sold and now has to convince his wife (sounded like me in summer 2012 when I first test drove it).

Today, brought it to the car wash...an old lady comes up to me when I'm about to get in after they dry it and tells me her friend just got one this week and she's excited to test drive her friend's car this weekend. She has a hybrid Lexus SUV and I told her she's going to get one once she test drives the S...she agreed because it looks so nice...but I told her it looks nice but the drive is what will sell her, she said she knows because of her hybrid SUV smooth driving...I just chuckled inside knowing its not even close.

these are everyday examples of excitement that can't be quantified in DCF...probably not in any spreadsheet either...basically as many cars as Tesla can produce I believe they will sell for the foreseeable future. There's at least a 3-5 year headstart in batter technology Tesla has here and by the tme someone catches up Tesla will be a generation of technology ahead of them. They can even increase the price further if they'd like to squeeze more margins if need be.�

1/1/2015

guest The DCF approach is even better with stable companies than with growth companies (or depending on your POV, is less unreliable for mature companies). DCF is premised on the efficient market hypothesis that a company's value today is equal to the expected value of future cash flows. With a stable company, the assumptions needed to estimate future cash flows are less heroic. Also, because one applies a discount factor to future earnings, the flat profile of a mature company's earnings doesn't depend as much on the discount rate you apply (which, properly considered, should include risk factors, which are also hard to estimate).

Long and the short of this: I think a DCF model for valuing Audi stock is reasonable, but not so for TSLA.�

1/1/2015

guest It seems to me, trying to understand this, that in addition, if you compare the DCF value to an ordinary stock price, you would be comparing apples to oranges. Under the assumption that Audi's revenue remains constant in the future, the DCF value of its stock price would probably be much lower than the actual stock price. Meaning, if I understand this correctly, that the DCF value is much lower than the prices one might compare it to (if one doesn't know it is a DCF value). One might discount the value twice, if you follow my thought. A percentage of 10% per year was mentioned, which to me suggests that DCF "prices in" a certain growth factor (and one might not be aware of that). If that is the case, and one hears the DCF value of a theoretical company with constant revenue, one would think its price will go down, whereas in reality, it might remain constant.�

1/1/2015

guest I agree. They will be sold out for a long time. I am expecting they announce they are spending what is needed to expand the production capacity to 50k a year. It seems obvious that soon, that will be the bottleneck.

Interesting article. The stuff Elon does for fun is amazing and this particular thing will get Tesla a ton of press coverage.

Elon Musk to make James Bond submarine car a reality - Oct. 17, 2013�

1/1/2015

guest Let me try to explain valuation models this in simplified terms:

A P/E analysis first assumes something about what kind of company you have, typically by comparison with others. Then it assumes that for this kind of company, each $ of earnings corresponds to a certain company value. Upthread, for instance, Sleepyhead used Toyota as the basis of comparison, and then "added some" ("if each $ earnings in Toyota is worth $25 market price, then it should be at least $30 for Tesla). Used this way, the method does not really look at fundamentals - if Toyota is overpriced, then the value you find for Tesla will be overpriced as well. However, instead of using comparison you can build a P/E up from fundamentals - for instance you can assume a typical discount rate to find that a company with flat earnings for the foreseeable future should have a P/E around 7.

A DCF analysis looks at the present value of a company for an investor who buys and holds it forever. That investor cares about how much dividends the company will be able to pay (this is the fundamental basis for all share prices), which also is largely reflected in earnings. So you project the earnings for the foreseeable future, and then you figure out how much that is worth in today's money. So this metric looks directly at the fundamental value of the company, based on assumptions.

(A P/S analysis, by the way, assumes that each $ of sales should correspond to a certain stock price. While it can be used for an occasional reality check, it disregards even the profitability of the company (in addition to all the other simplifications of the P/E). It was used during the dotcom era to defend sky-high valuations of unprofitable growth companies. Most of them never reached profitability. However, comparing to companies of equal profitability with P/S gives exactly the same result as a P/E.)

No, DCF is not premised on efficient markets. It provides an estimate of the fundamental value of the company, regardless of the efficiency of markets.

Efficient markets only come into the picture if assume that long term fundamentals are reflected in the share price (which I think is a basic premise of this thread, regardless of which method you use to assess those fundamentals).

Yes, it is easier to value a stable company, but DCF does not make it simpler or harder. With DCF will scratch your head over what to assume about future cash flows, and correspondignly with P/E you will scratch your head over which P/E number to chose. Each method has advantages and disadvantages in this respect:

- With DCF, it is easy to get an answer that is "exactly wrong". You fill in a spreadsheet with assumptions of what the capital requirements will be in 2022 and stuff like that, basically pulling the figures out of your ass. Then you show the spreadsheet to someone, and they think "wow, how detailed he has worked that out" and believe they have The Right Answer. On the other hand, the advantage is the understanding you get by checking and varying the assumptions. By trying different scenarios, you can learn a lot about which assumptions are the key ones, and then you can make some scenarios (and ideally, as I advocate for high-uncertainty situations, you do a probability-weighted average of those). For instance, Prof. Damodaran's model showed that his assumptions for capital requirements and employee options were quite important, while some others were not. To a certain extent you can say that the model is nothing, the modeling is everything.

- A P/E hides the assumptions in a black box. If you for instance use a comparison with Toyota, you are basically assuming that the value drivers of Tesla and Toyota are similar. You disregard the possibility that the future earnings trajectory may be quite different, that there may be fundamental differences in capital structure, capital intensity, hidden liabilities, brand value, tax rates, ZEV credits, new business opportunities etc. (or at least you assume that all these factors even out and on average don't matter). As used by Sleepyhead, it is even worse, because he is using a ratio comparing the Toyota of today to the Tesla of 2018. A skilled P/E user such as Sleepyhead will try to take the potential differences into account and guesstimate a correction. Just as with DCF, an unskilled user will mindlessly apply a ratio without knowing what he is really assuming. This is the garbage in/garbage out factor playing out alike for both methods. But I would say that the disadvantage even for Sleepyhead is that he can easily overlook some factors that could be important in the analysis. Also with P/E it is important to make scenarios for a company like Tesla, because your One Main Predicition will most likely not hit the mark. And finally, P/Es are very cyclical. Today's levels have only been surpassed twice since 1880, so may not be sustainable. Using comparative ratios in this market may give a result that overshoots fundamentals.

Actually this is wrong. Risk factors (as in "uncertainties about future cash flows") should go into the cash flow model - either by making the projection a "middle-of-the-road" scenario or by doing multiple scenarios and then do a weighted average based on probabilites. The only risk that should go into the discount factor is the cyclical risk (so-called beta). The discount rate will always be contentious, but for a stock where the debate is whether the right value is $50 or $1000, other assumptions will be much more important than whether to use 7% or 10%. In any case, this assumption is hidden any P/E ratio you might use, so even if you don't see it you are still assuming a certain time value of money (you just don't know which).

I think the exact opposite: Audi is a know quantity, and you won't go very wrong with a P/E. With Tesla, there is more value in digging into the underlying assumptions, which is what you do with a DCF.

You are right that using DCF today's value will be lower than tomorrow's, but that is the expected behaviour of stocks. If you predict that the stock should be at $500 in 2030, you most probably should not buy it at $300 today (because it would only give you 3.1% annual return). DCF factors this in, so that when it outputs a value for today, it takes into account that you want the stock to rise at a certain minimum rate to want to hold it. So when you look at the per share result from a DCF, you compare it to today's stock price - if the DCF is higher, that indicates that you might earn more than the time value of money by investing.

I hope this clarifies a bit. I am a bit surprised that there is an almost ideological debate about different valuation methods. They are all tools in a toolbox - use them correctly and when appropriate. Or feel free not to.�

1/1/2015

guest In the discussion for updated orders page that now has for US the power folding mirrors in the tech package so there's some update in the cars features that also increased the tech package price slightly. However what was interesting for me was that I looked for the EU order page to see if that's progressed there as well (it's not) and while doing that noticed that the Performance 85 model has "Delivers in 5-6 months" now as the estimate. I ordered 1 month ago and then it said "Delivers in January" which made it ~4 months meaning that the EU queue length has gone up or Tesla is planning to produce less cars per month for EU. I'd bet more on the fact that the interest has gone up with actual deliveries and the queue has gotten longer. If we factor in a steady increase in production capacity this bodes real well for 2014 deliveries in EU.�

1/1/2015

guest Elon has said before that there is a direct relationship between deliveries in an area and subsequent orders there. Sort of a moment of cold fusion for Tesla. I wonder with the initial rush of cancellations late last year and early this year now being over (when people were asked to configure after years of holding a reservation), perhaps Tesla has a much better picture of a percentage of reservations that translate into orders/deliveries. May so strong a projection they might begin to share that number with us - you know, 'We delivered 6,500 Model S' in Q3 and exited with the highest backlog ever, XX,000 reservations on the books." Would be nice to know.�

1/1/2015

guest Moderator's note: ?a few posts moved to Short Term Social Chat�

1/1/2015

guest +1 DonPedro - The DCF is the best way to value TSLA because it is an extreme growth stock. As you correctly noted there are many things about Tesla's P/L that are drastically different from any other company. Compare Tesla to other automakers and you find Tesla has no marketing budget, sells cars at full retail price vs. wholesale, has revenue that is increasing at the rate of a dot.com, etc. Those can be modeled. They won't all be accurate but you can ballpark a reasonable expectation and have more clarity on Tesla's future than w/o a DCF.

BTW, Prof. Damodaran's DCF has many faults. IMHO the biggest are: stating Tesla's sales will be comparable to Audi's. Audi sold 1.45 million cars in 2012. Many of us believe that the Gen III platform will result in many more sales than that number once capacity infrastructure is in place. The second is comparing Tesla margins to Porsche. Sorry, but Porsche sells their cars wholesale and Tesla sells at full retail. Tesla's margins will be much higher than Porsche's. Lastly, it's impossible to forecast Tesla's development and potential Supercharger Access revenue. If Tesla maintains their battery technology lead over the rest of the industry then it will be inevitable that the other automakers will be forced to buy Tesla's batteries and motors or at least to license the technology. And if that happens there is a reasonable expectation that they pay Tesla so that their own cars can access the Tesla Supercharger network which will be fully implemented and will have the advantage of being first to market and therefore having the best locations. My last point may not come to fruition. But if it does, then Tesla gets a HUGE P/E for they will dominate the auto industry.�

1/1/2015

guest mmmkay, but it was intended neither for the short term thread audience nor as a social chat topic. So, you know, there's that...�

1/1/2015

guest AT&T announcement is leading me down the road of apps and a Tesla App Store.....a new revenue stream. Many apps will be using the cell network. Tesla has to have data plans in place before they can allow Apps to go live.

My guess, an app for your Model S could be $5 on the low, higher depending on functionality. I have not seen any research estimates from the big banks taking into account App Store Revenue.

Overly simplistic math on Tesla App Store Revenue:

2014 : 25,000 cars x avg 3 app purchases @ $5 = $375K revenue

2017 : 175,000 cars x avg 4 app purchases @ $5 = $3,500K revenue

2020 : 750,000 cars x avg 4 app purchases @ $5 = $15,000K revenue

Not huge but it would be high margin. Something fun to think about!�

1/1/2015

guest The cost of the car in foreign to US countries is higher due to Value Added Tax (12-17%?) Consumption Cost (15%-25%?) and Custom Duties (10%?). The $162,000/Model S for China would not equate to $162,000 back to Tesla, for which my figures are based. I recall EM stating Tesla would not exploit the demand in other Countries unlike other auto manufacturers. Therefore I foresee average more in line with $90,000/Model S. With Battery costs decreasing 5-10% per year, and added efficiencies of mass production, margins will increase and Tesla will be able to pass on some of these savings to the customer to increase demand as well as increase battery range. I agree that for the Gen. III car, 30% margin will be a good number to beat.�

1/1/2015

guest No VAT in Norway, but higher sales price. Some might be due to higher salary and transportation costs, but there's no guarantee that they don't make a higher margin on these cars.�

1/1/2015

guest lolachampcar, I certainly hope so, and believe my figures to be cautiously optimistic. For example, Mr. Irwin is throwing 300,000 - 500,000 for '17. I have no doubt the demand will be North of my assumptions, however the supply constraint is another story. I would much prefer Tesla to ramp up more slowly (understatement) to avoid quality control issues. They shouldn't be following those like Toyota who announced this week yet another recall of close to 900,000 vehicles. Ramping up from 24,000 (expected '14) to over 600,000 (my forecast '20) represents a 25X increase in production in just seven years. This is still enormous. I didn't go past '20 in my chart, but that is when the production numbers really take off. Applying another 25X increase over 7 years would equate to 15,000,000 vehicles by '27, but even the longest term Tesla Bull would call this a "pie in the sky".

Best,

Words of HABIT�

1/1/2015

guest I think you are more or less confirming my impression, as I am not doubting the abstract value of going through the process of computing such a number. DCFs seem to have the tendency to imply the expectation of a quite high annual return (10%), setting a quite high standard as a general number. So one really needs to be aware of that expectation being part of the number already, as its effect can easily be higher than than 2x (and 5x for 2030).

I'm saying this aside from several larger concerns I saw regarding the specific assumptions of the DCF we were discussing (for example, significantly, regarding the cost (and time) of getting to mass production level, and the dilution it would require... or not). But then, that is where you obtained very different results.�

1/1/2015

guest I am not sure if this should be in the short or long term thread but here it lands.

Part of Elon's options package is for Tesla to achieve 30 percent margins for four consecutive quarters. I think it is apparent to all here that Elon will push hard to meet all the milestones necessary for his maximum payout. I dont think he will push hard because he is greedy but because this is what was laid out to him as a set of goals for him to reach and he is very goal oriented. I think he is pushing hard to exit q4 at 30 percent gross margins so he can have his 4 quarters in 2014.

At the end of Q4 they will begin producing in limited numbers the first Model X's. These will all be signature Model X's and will be in very low volume so I don't think that will pull down gross margin. Once we get into Q1 2015 and start producing the Model X in volume gross margins will take a negative hit initially. Just like the Model S I think in time they will get in back to the levels that the Model S will be at and maybe higher but with each model they introduce I believe it will drag their gross margins down temporarily.

When they start volume production of Gen 3 I think it may be very difficult to hold a 30 percent margin at least not until it has been produced for many years. For these reasons I think Elon and company will be pushing hard to get as close to 30 percent GM going into Q1 as possible.

Would love to hear others thoughts on this.�

1/1/2015

guest Great points blakegallagher. Additionally, Elon has alluded to not wanting to run 2 companies long-term and you can tell by the way he talks that SpaceX and putting people on Mars is his biggest personal goal. Tesla's goal of "accelerating the advent of electric vehicles" is much more vague and appearing much more inevitable every day. I believe long-term Elon sees Tesla as a means to raise capital for several Mars missions and begin colonizing the planet. The couple billion extra dollars he stands to make if he unlocks all his options will be needed for these missions.�

1/1/2015

guest Aside from that, there's another benefit to his options package for Tesla. Remember that financing guarantee? Elon is personally backing it. Achieving his targets is beneficial for the company because his asset value would increase substantially.�

1/1/2015

guest If you haven't read it yet recommend doing, there are plenty of short and long term indicators in the Q/A and Elon's statements to affect the near term movement of the stock! Especially nice to hear that Panasonic is committing to 1200 cars a week production rate, no dates but bodes well for 2014 speculations.

11/20 Munich Tesla Event with Elon Musk�

1/1/2015

guest More people realise the fact that if you drive a Taxi, then you should choose Tesla.

http://www.rogalandsavis.no/nyheter/article6934348.ece (norwegian)�

1/1/2015

guest Yeah, when I last took a cab here in Tallinn I asked out of curiosity what the approximate daily distance is that the guys drive and he did some maths from his logbook and said that he averages 200-300km with the freak day being 400km. With the 85kWh battery he could charge at home and do his daily faring without a single hiccup even during winter barring the freak day in -30C when he might have to stop for a charge mid-day when he takes his lunch break to offset the possible distance needs. So yes, for city cabs the Tesla would be a perfect car considering that you could save 5-10x on the fuel cost depending on region and fuel is one of the biggest components of cab fare cost. So I also see a bright future in cab companies implementing taxis. Heck, if I had the capital I might pick it up myself") �

�

1/1/2015

guest In places like NYC, taxi vehicles are used pretty much round-the-clock, so there's never a good time to charge an EV cab.�

1/1/2015

guest Could we not also say that there's never a good time to visit the gas station? I would imagine cab fleets would use supercharger-level charging if possible. Perhaps the cabbie's coffee/smoke break becomes more productive?�

1/1/2015

guest The article states that they got 2 superchargers for 50 000 dollars a pop, could this really be accurate? as I saw ur earlier statement from that uneducated tesla spokesperson who said 1,4 million?

And if this is true would this be the first confirmed private supercharger?

Edit:

I see now that google translated kroner to dollars so thats probably a standard HPWC they installed...�

1/1/2015

guest They try to avoid breaks. Tough to park in busy areas, for a start.

NYC also has expensive electricity, so they won't have the c/mi advantage they'd have in other cities. Average miles per 12 hour shift is 180 in NYC, so if they only save $1.80 per c/mi, the 45 minute loss of time could be costly. Costs still need to come way down, but it's definitely so ething Tesla should have its eye on. Right now, the Model S price and weight would mean it would likely be better to buy 2 Leafs instead.�

1/1/2015

guest A taxi fleet could have a dedicated swap station. Can't beat a 90 second "fill up".�

1/1/2015

guest In case it wasn't posted yet - Elon's meet & greet event in Germany

http://www.teslamotorsclub.com/showthread.php/22897-11-21-Munich-Tesla-Event-with-Elon-Musk

It looks like Panasonic will be able to supply 1.2k runrate worth of batteries by 2015. This extrapolates to about 63k cars for 2015. Also means there'll be 100k Tesla's roaming around the globe by the middle of 2015. Thoughts on how this changes/solidifies anyone's opinions?�

1/1/2015

guest At the munich event yesterday was a model S owner operating it as a taxi. She asked for a limiter to the max speed (to conserve energy). Elon said we might get it with the december update.�

1/1/2015

guest Exactly. It's difficult to make swap station economics work for the general public right now, but for fleet cars it works out great. Here's some quick math...

ICE

Tesla

cars 100 miles/day 300 mpg 30 gallons/yr 10.95 million fuel cost/yr ($3.50/gal.) $1.28 million