Nov 3, 2015

dhanson865

I'd argue that next year from 2015 is 2016. I'm not sure why you think "next year" from today isn't 2016?

See my partial transcript above.�

Nov 3, 2015

Yuri_G We are saying the same thing. Starting in the second half of 2016 is different than starting at the end of 2016. I would interpret that as starting in Q3 2016.�

Nov 3, 2015

tftf The Q3 2015 shareholder letter says "end of 2016" for stationary cells produced in the GF. See on page 2.

And on the CC the CTO mentions EV cells by 2017, as I had mentioned. See transcription provided by dhanson.

I don't see how that is massively ahead of schedule on the EV side.

We will likely have to wait for the 10-Q for more details.

PS: I also wonder if Tesla will finally correct/clarify their GF investment numbers for 2015 (numbers didn't match in previous 10-Q). In any case, Tesla and Panasonic didn't invest a lot in the GF so far compared to full $4-5bn needed/projected until 2020.�

Nov 3, 2015

Yuri_G "The Gigafactory project is on course to begin battery cell and pack production in 2017."

Q1 2014: [/FONT][/COLOR]http://ir.teslamotors.com/secfiling.cfm?filingID=1193125-14-187459&CIK=1318605�

Nov 3, 2015

JRP3 OK, I missed that.�

Nov 3, 2015

dmckinstry Even the most efficient PV cells have a lot of waste heat that can be used (as already mentioned) via heat pumps.�

Nov 4, 2015

tftf To expand on these numbers:

If one building corresponds to one block as the article/linked video below says then satellite and drone images will immediately show when Tesla starts building up additional battery capacity in Nevada:

Tesla Gigafactory Could Be Over Twice Initially Planned Size | CleanTechnica

Therefore the current GF building will probably only be able to pump out 5-7 GWh on the cell/pack level in 2017.

This very roughly corresponds to Tesla and Panasonic only investing about 20% (of the total planned funding of $4-5bn by 2020) until 2017 (that's even generously rounding up past and projected cap-ex for the GF).

The next 10-Q will show how much has been spent on just the first block (corresponding to about 14% of capacity in all 7 blocks) so far.

I know this info isn't new, the video in question has been discussed before: Tesla Gigafactory - Page 53

But this topic is interesting because of the total investment needed for the GF (to one day build 500k car batteries/year) versus money raised and invested up to now.

Tesla can probably only equip about 70-100k* cars/year (which limits future Model3 sales, this production ceiling can't be changed overnight until new blocks are constructed) using the current block 1 building.

_____

* I'm likely very generous with 100k cars/year (because Tesla was talking about 35GWh on cell level and 50GWh on pack level once full output is reached and pack sizes per car keep going up in the future; also, in case assembled cells arrive from third parties into the GF Tesla won't have the full claimed cost advantages over other suppliers...).�

Nov 4, 2015

Tim JB said there's not even going to be natgas piped into the gigafactory. All process heat is going to be via heat pump. Sounds pretty efficient to me.

Edit:

Just saw your later reply in thread. A modern heat pump can easily have a COP of 4. Even compared to solar heat directly. A heat pump powered by 22% efficient panels probably exceeds what you could do by concentrating sunlight directly.�

Nov 4, 2015

electracity It must be fascinating to have access to so much proprietary information.

- - - Updated - - -

Except that Tesla neither will make 55000 cars or make nearly the number of MX they forecast. I think Tesla is doing fine, but they are not making their numbers.

Gigafactory guidance, like all guidance, is a lowball estimate. Until they actually produce cells they haven't made a meaningful goal. Proclaiming them as the undisputed leader in low cost li-ion is a bit premature before they have made a single cell. Stuff happens.�

Nov 4, 2015

dc_h Tesla is on track to produce 70-80,000 cars in 2016 without any GF cells. Based on their ramp up, it seems likely that margin from Tesla Energy will be reinvested in ongoing development of the GF. As 2017 comes and the Model 3 starts, cell production seems to be on track to expand more rapidly. I don't think they have firmed up expected numbers for Model 3 in 2017, but 100,000 for year one seems aligned with the long term plan laid out in 2013.

I'm not sure if you are making a bear case or not with this post. Your historical record has Tesla bankrupt well before now, but you are laying out a cash flow neutral project that will result in a GF twice the original scale by 2020, allowing cash flow from Model X & S to be invested in the Model 3.

�

Nov 4, 2015

tftf Yes, they can produce the S and X fine in 2016 and beyond with Panasonic supplying the cells from factories in Japan. I never wrote about Tesla going bankrupt in 2015 or 2016 - Tesla can continue to spend for many years as long as there's people willing to raise more funds (either more debt or dilution).

But this isn't cash-flow neutral, except for maybe a single quarter until the next cap-ex wave kicks in, see chart here:

Tesla's Eternal Flame - Bloomberg View

And Tesla Energy isn't an automatic magic cash-flow machine with high margins. As we all know, Tesla competes with its own cell supplier Panasonic in this space (as well as many others):

Battery FrenemiesTesla and Panasonic Poised for a Fight in Europe - Bloomberg Business

I outlined above that Tesla is currently building up just 14% of the planned capacity for the GF - not even this first block is finished for cell produciton until late 2016 / 2017.

Now compare the state of GF1 (block1, 14% of the total and probably good for only about 70k cars/year, not 500k) to the money raised in early 2014, in mid-2015 (not even talking about the line of credit, just the dilution) and with the cash on hand at present.

Tesla will need additional billions to finish this first GF from 2017-2020.�

Nov 4, 2015

jesselivenomore This "dilution", has TSLA raising a secondary ever caused the stock to go down? No, because raising money to build a factory is not dilution, it is investment and value creation. They are not raising the money to keep the lights on. The market understands this, which is why the stock often rallies on secondaries instead of going down. So TSLA will dilute all the way up to 500, 1000. And investors will be more than happy to give them more money, because they are creating value.�

Nov 4, 2015

SteveG3 tftf, Tesla will be cash flow breakeven to positive when the Model X reaches steady state production. this is expected to happen in Q1, perhaps it does not happen until Q2 if new production challenges arise for the X. Yes, that's further out than what was said at the beginning of the year (getting out of cash flow negative by Q4). Tesla already raised ~$700 million in August of this year to compensate for this delay.

you are correct that Tesla will need billions to finish the GF. what you do not seem to have realized is that those billions will come from their ongoing business selling the Model X and Model S and eventually the Model 3. perhaps you've come to believe that Tesla loses money with incremental vehicle sales. that is completely false. be careful, there are many people who do not want Tesla to succeed and some write and say things about Tesla that are completely false. inform yourself and you will not fall prey to this nonsense.�

Nov 4, 2015

electracity It seems we should see the footings being built for block 2 now, based on car and Tesla Energy demand. If the plan is to be at full production by the end of 2020, and Tesla is on plan, where are the footings?

Why isn't Musk asked to lay out a capital plan that matches his production plan?�

Nov 4, 2015

tftf We will see. That's what people said a few years ago.

Maybe they will once again manage 1-2 quarters in the black (see chart above for late 2013 and early 2014), but then the Model3 and the GF will again consume billions that aren't realistically coming from operative results.

I doubt many people realize how much additional investment the "full" GF (7 blocks) will need going forward and how "little" - compared to the full $5bn - has been spent so far on just one GF block (14% of the total project). For those who missed this article back in May/June:

Tesla's first building phase nearly complete | Las Vegas Review-Journal�

Nov 4, 2015

Svetlin Tesla should be able to get at least $25B in revenue in 2016 and 2017 combined. Assume 20% gross margin = $5B in gross profit. R&D + SG&A for 2 years should be less than 4B. Here is another billion to burn for the next 2 years. Oh, and count at least another billion in customer deposits once Model 3 reservations open.

I predict that Tesla will only do a capital raise in 2016 if the stock price is above 400.�

Nov 4, 2015

tftf We will see. Here's how Tesla "sold" investors the $2bn raised in early 2014 for the GF:

Tesla Raises $2 Billion With Convertible Debt to Finance Factory - Bloomberg Business

Now, that money is gone and not even 14% of the "full" GF is built out - with an additional 12-15 months to go until local cell production can be started at this "14% of the total" battery unit.

This is only to show how rosy outlooks (in terms of positive cash-flows and ROI) can change.�

Nov 4, 2015

SteveG3 What are you talking about tftf?

"a few years ago" the discussion was,

Bears: Tesla? Ever heard of DeLorean, Tucker,... They'll never build a car as desirable as the 'big boys". Besides they will go bankrupt before they can reach volume production.

Bulls: There are inherent advantages to a well done long range EV over ICE vehicles that will make the car compelling independent of environmental concerns. The Model S and Model X are strategic moves to provide Tesla funds to deliver the Model 3.

That was when Tesla was trading in the $20s and $30s, and the company was hoping to reach GLOBAL volumes for the S and X COMBINED of 30K/year.

Since then the Model S has been a success far beyond anyone's expectations. Tesla has gone from looking for the S/X to fund the Model 3, to looking for them to fund the lion's share of a $5 billion battery factory (the increased investment for the future that makes it an obvious win to go from profitable quarters as a niche automaker to quarters with losses to tap enormous potential).

Many of us here on TMC have been bulls from "a few years ago" through today. The only call I've known you to make on Tesla these past years is your claim that the stock is overvalued... a claim you've been making it since it traded in the $70s. Looking back on whose comments from "a few years ago" turned out to be helpful (or not) does not seem like an exercise you would want anyone to engage in if your object is to make your bear assertions seem more persuasive.�

Nov 4, 2015

electracity You forgetting the rise in inventory needed to build a lot more units per years. 2017 volume will probably raise inventory by a billion. So even a billion in profit is not a billion available for capital expenditures. And of course there won't really be a billion in profit over the next two years.

I don't need Tesla to make a profit. I just want to know the capital budget, and where the money is coming from. This isn't the software business where the bet is on a product taking off. Tesla has to build stuff with very capital intensive inputs.�

Nov 4, 2015

tftf The "easy money" in Tesla was made from mid/late 2012 to early 2014. These days are long over.

From the day TSLA raised the $2bn "for the GF" (which didn't turn out be exactly true, most of this money was spent on other items, see my earlier comments in this thread for details) the stock has not gone up compared to today.

Back at the end of February 2014 TSLA was already trading near $250 - it's still lower at the moment, even after the gap today.

PS: Not even accounting for the risk and increased vol compared to investing in a broad index etc. since that date.�

Nov 4, 2015

Newb +1

I'm getting tired of the repetition of the same old arguments against Tesla which aim to spread fundamental doubt and uncertainty (overvalued, toys for the rich, overpromising). It's all blind to the reality. Blind to what's been happening in the past 3 years. Tesla went from 500 cars produced per year to 500 cars produced in 2 days as of today. If you'd look back what tftf and similar posters have been predicting about Tesla's future 1.5-3 years ago, you'd feel ashamed for them. And the worst thing is, that they don't seem to learn, nor would they admit being wrong or acknowledge Tesla's success story. And this is frustrating. Sometimes I wish mods could do something about this - obviously repeating nonsense is in the gray area somehow and therefore they continue to macerate our nerves. I don't care what their intentions/motives are, I just wish they would just stop it.�

Nov 4, 2015

SteveG3 so you are saying not only did you get it wrong when you called Tesla overpriced at $70 in the middle of that timeframe... you are also now saying it was easy to see TSLA was a great buy during that period.

look tftf, I don't want to get in a personal back and forth with you... the point is, we're not going to be passive when you post intellectually dishonest gibberish (garnished with a false air of "authority" despite your track record of getting TSLA predictions wrong). do you want me to link the two TMC threads in the past year where I provided evidence which thoroughly debunked your intellectually disingenuous claims for what they were?�

Nov 4, 2015

Familial Rhino I sympathize, but the last thing this forum needs is to silence the naysayers. It would be just as misguided as those governments who blame short sellers and speculators when their stock markets or their currencies collapse. Bearish views play an important role, just like wolves in the forest: they help the market weed out the loser stocks. I'm sure many GTAT investors regret not having been more exposed to skeptical viewpoints.

Different people look at things in different ways, and place their bets accordingly. Of course you will get a lot of disagreement. This is how information gets disseminated and processed to the benefit of all.�

Nov 4, 2015

SteveG3 I agree. I want objective analysis, not cheerleading. However, in the case of someone who has a longstanding and voluminous track record of intellectually dishonest posts, isn't it appropriate to call attention to this? Beyond what he's done here, tftf has literally posted about 3,000 (yes, 3,000) comments on Seeking Alpha about Tesla... all negative since the first ten or twenty. How probable does it seem that someone with nearly 3,000 consecutive negative comments on Tesla since May of 2013 could be intellectually honest given Tesla's successes between then and now.

Pointing out tftf to the unsuspecting is similar to pointing out John Petersen or Corey Johnson.

Tales From The Future's Comments on TSLA: Tesla Motors (Page 2) | Seeking Alpha�

Nov 4, 2015

Svetlin Inventory is on the balance sheet, not the income statement, or am I totally wrong... I am not a finance guy. But thanks for pointing out that omission, I guess it does decrease the available cash to throw in the cash incinerator.

But when you say "of course there won't really be a billion in profit", what are you saying: Revenue will be less than 25B for the two years, gross margin will be less than 20%, R&D & SG&A will be more than 4B? All of the above?�

Nov 4, 2015

Familial Rhino I dunno. Where do you draw the line? I may be wrong, but to me it seems that tftf believes what he says. I think this forum has done a good job so far in rejecting drive-by posters like those that are rampant on the Yahoo finance forums. Personally, I'd rather err on the side of open exchange of info.�

Nov 4, 2015

austinEV I invite TFTF to create a "bear cave" thread or a "TFTF bear case" thread where the best bear case is presented, edited and discussed. The bears can discuss and hammer out their best case. That way all the best arguments would be in one place, and it might incentivize Bulls to do the same. If we don't change the structure we are going to have an endless bickerfest because TFTF is presenting a case methodically and with repetition and we end up just bickering about it. Bulls respond piecemeal and the responses are lost in long threads and then we stop responding and the bear case gets restated. (If I see that cash burn chart one more time...)

This burden falls on Bears, being a minority. Make a thread, where your case is the focus and we can address it there instead of EVERY thread becoming a bickerfest.�

Nov 4, 2015

Familial Rhino I can't believe I'm coming to tftf's defense, but I think it's better for us to tolerate a certain amount of irritation than to create a "free speech zone" for the bears. (And I'm printing the Bloomberg TSLA cash burn chart right now and I'm sticking it to the wall. I'm crazy that way.)

Edit: to be clear, I hope tftf takes you up on your challenge and starts his own thread. I was just pushing back on the moderation calls.�

Nov 4, 2015

dakh Don't forget that some of the investments needed for Model 3 have already been made: paint shop, stamping, some of the R&D. Like was mentioned in a call, they're now looking at improving on the 2 year design to manufacture timelines for future models.

I get the point that stock already has a lot priced in. But success begets success and a lot of what we don't know haven't been priced in. To me the attraction is in the fact that this company can move quicker than anybody during disruptive times, and that's not something one can replicate by throwing more resources in.�

Nov 4, 2015

SteveG3 this seems like a reasonable compromise. you've cited good reasons to have the comments be in one place, and it would avoid completely blocking comments.

fwiw, my mistake going on memory and writing that tftf has 10,000 TSLA comments on Seeking Alpha... the correct number is roughly 3,000. they have been, however, since the first handful, all negative since tftf called Tesla overpriced in the spring of 2013. again, how probable is it that someone who was being intellectually honest would have commented 3,000 times on Tesla, and not have had one positive thing to say about Tesla's accomplishments between then and now.�

Nov 4, 2015

Newb couldn't agree more. @Familial Rhino: I'm not saying we should silence the naysayers, just silence the obvious manipulators who are not interested in any informative discussion at Tesla Motors Club. And the moderators and people running the TMC forums should ask themselves if they want this place to become a battle arena of cheerleaders vs. manipulating perma-bears. I'm just saying that balanced people could stay away from this place in the future if reading through increasingly more posts from posters like tftf or electracity are just a waste of time. Why would balanced people continue to come here for sharing valueable information if tftf and others conquer this place with their nonsense and just frustrate us?�

Nov 4, 2015

tftf I didn't mean "easy" to spot, I meant "easy money" as momentum drove TSLA from about $20-35 in 2012/early 2013 to $250 by the end of February 2014. I simply pointed out that the stock is still slightly down compared to that date (Feb 2014) - all the talk about retail trading "Teslanaires" buying their car with TSLA stock profits is gone. TSLA has been flat till today, with a few spikes to $180 and $280 in between.

Unfortunately, only a few of the past replies have been about the content/arguments I presented, such as various links (Bloomberg FCF chart etc.), internal battery competition with supplier Panasonic or the fact that only 14% of the "full GF" is currently being built and ready by 2017 for EV cell production - with all of the $2bn "GF money" raised in early 2014 already gone and mostly used for other business purposes.

So I'm going to retire from this thread and the forum for a while since this discussion isn't on-topic (GF investor thread) and therefore not very productive imho.

Everybody can return safely to the bull echo chamber�

Nov 4, 2015

Familial Rhino I see where you're coming from, but I think we stand to lose more, as participants on this board, if any one person's standard of objectivity or balance is enforced via moderation. I prefer the chaos of the bazaar; yes, bazaars are full of tricksters, but I'm more afraid of any top-down enforcement of "balance". Besides, as I said, the signal-to-noise ratio in this bazaar of ours seems quite healthy to me.

Anyway, I'm not a moderator. I'll let them make their call without any more input from me.�

Nov 4, 2015

BriansTesla I wonder how many of the bears on this forum today are still very pissed that they missed the easy money. I think it would leave a bad taste in my mouth. Fortunately, I was early on the wagon.�

Nov 4, 2015

chickensevil I think the reason you don't get responses on the actual subject is because people are tired of repeating the same things over and over again as this line of commenting hasn't changed nor has the responses... But you know what... I'm bored, so why not?

Huge negative cash burn -> Well, they did raise a heck of a lot of money, right? Shouldn't they be spending it? I would be more worried if they were hoarding it up until a rainy day. It has been pulled up before but what they claimed they would spend the 2B$ on was cleverly worded such as to allow them to basically spend it on whatever they wanted to. Thus far the comments about needing additional funding beyond that have been to support *other* growth, not directly related to the gigafactory (granted I don't think anything is restricting them from using the 750M$ on the gigafactory... but that wasn't the focus of the claim.)

That being said it has also been stated that the numbers on Construction don't tell the full story on the cost of the gigafactory. Someone has already recently pointed out that R&D so that the cells are fit to be used in that factory is a part of the cost of building that factory. Tesla doesn't (and shouldn't) itemize every little thing they spend their R&D/CapEx/OpEx on. Now that they have moved into the factory (at least on some level) there is likely to be costs associated with the bringing this factory online that fall under OpEx finance lines.

And why do you say it is "already gone" Last I saw they had 1.4BN in cash, if you add in 750M$ raised for "other purposes" that puts them back over 2BN$ of funding they had to allocate toward the factory. Because really, you can say that they got ambitious with the X, and had to lay the groundwork for it, plus the Model 3 growth, and the 750M$ raised was basically paying back on that cash burn they already spent. So now they are back to a healthy cash pool that can be funded toward the Factory.

To put it another way, total cash raised was roughly 3BN, they "spent" at least 750M$ of that toward expansions at Fremont, and I would argue they have probably dumped a decent amount toward the gigafactory.

They have spent (as of June 30) a little more than 200M$ on stated construction of the factory. If as you say that is "all they have spent" and we know they have already moved in some services into the building (meaning that it would have to be at least mostly finished being built for that section, in order to stick people and machinery in there...) then one could start to estimate that all 7 sections being completed should cost them around... what? 1.4BN... Let's throw an extra 100M$ on top of that for "other expenses" so it is 1.5, subtract off the 200M already spent, leaving about 1.3BN left to go. Huh, how much cash do they have left? Oh, right! 1.4BN...

So where is this cash problem of which you speak? They back funded the 750M$ from the spending they already did to grow the business in a way that if things go like they are looking will be returning dividends to the company (for future growth and investments) starting Q1 of next year. So if you had the choice, slowly invest 750M$ in cash over the next few years to have it paying back by 2020, or invest it all this year and have it paying back by Q1 of 2016? I would have to say you would be stupid to go with the slow route.

- - - Updated - - -

Oh and one more note, it had been pointed out that if you take off the CapEx and the R&D they would be easily in the green. If they wanted to sit back now and stop growth (maybe even tailor back on some of the OpEx since you are going to stop growing there is a lot of pointless OpEx if that was your goal... Fire like 2,000 some odd employees at least) such that you could keep a reasonable R&D budget going and be in the green. But noone wants that... That is why investors in general are not panicing over the numbers on your bloomberg chart. That is a good thing since that spending is contributed to 3 major things:

Growing your market footprint so you can service a global market (They are just trying to get to the level of where MB and BMW is at, nevermind trying to go any further in global coverage, we aren't even to BMW numbers yet as far as footprint goes)

R&D spending to continue to keep yourself ~10 years ahead of the competition (maybe further... don't know... noone has made a real Model S killer yet... which was released in 2012 and shown to the public in 2010... I think someone might have one to market by what? 2017 is the current timeframe... who knows? they keep saying "in three years" for the past 3 years...)

CapEx to grow the business to make not just 100k cars, not just 500k cars, but eventually millions of cars by 2025 (If they keep making products as they already have with the Roadster, the S, the X, and Stationary storage, then they will have no issue selling everything they can make so I fine with growing to millions of cars, because they have never yet made even remotely a crappy product or concept a crappy thing.

So spend the money. Spend it as fast as you can, but as smart as you can.�

Nov 4, 2015

austinEV Thanks Chicken for doing the work! You are my hero.

By the way, my earlier comment about making a "bear cave" thread was not meant to be disrespectful of TFTF nor was it intended to "rope off" critical commentary. I am not attempting to create a positive comment only zone. If we bulls are so thin skinned that we cannot hear disagreement without shedding tears then you know it is time to sell!

I was genuinely trying to create some better *organization* of this bull vs bear conversation that has started. The "short term" catchall thread famously addresses anything and everything and it is by definition a lousy place to contain an important thread. So, break out the Bear chatter in its own thread not to silence it but to focus it. And, if we bulls are so smart we should be able to refute stuff there and not have it swamped by 20 pages of "yay the stock moved" chatter.�

Nov 4, 2015

Familial Rhino Understood and agreed!�

Nov 4, 2015

jesselivenomore It was not "momentum" that drove TSLA from 20 to 200, it was the 30% in short interest who were forced to liquidate by their brokers as they saw their accounts evaporate. In the mean time, TSLA capitalized on this by raising capital at an elevated price level caused by the forced buying. TSLA was "overvalued" in this period, as Elon Musk admitted himself.

But, by taking advantage of the short squeeze and elevated valuation, TSLA was able to raise money and accelerate their initial plans. When before the gigafactory and model 3 were goals far off in the future, the shorts allowed TSLA to bring that to reality much much sooner.

With the acceleration of TSLA's progress, and the value created by the capital raised, including the gigafactory, TSLA is now fairly valued again. But in the meantime, shorts like tftf have once again piled into TSLA, up closed to 30% in short interest once again. While many longs in this thread like to argue and correct them, what we really should do is thank them. It is the shorts that have accelerated TSLA's progress, and it is the new shorts who have yet to be burned who will fuel the next phase of expansion.

It was not longs who bought TSLA through 200 the first time around. Think about it, what investor would buy a stock who just rallied 500% in the straight line? No, it was insolvent shorts who were forced to closed down their trading accounts who bought TSLA through 200. And tftf, I know guys like you will never concede that you are wrong, and I genuinely hope you stick to your guns. All the luck to you. Because it will be people like you who will buy TSLA through 400 and 500 as your accounts are liquidated.�

Nov 5, 2015

mkjayakumar There is a reason why bears like TFTF don't get any respect here. The fact that he has not acknowledged a single thing that Tesla has done right and always looking for FUD and glass half-empty outlook, gives the impression that they want Tesla to fail and fail badly.�

Nov 5, 2015

tftf

Let me just address that because I don't like open questions or wrong numbers floating around when I leave a discussion:

- Of course Tesla could spend the $2bn on any business-related purpose. I never accused them of doing something illegal. The issue is however communications to investors because they made it sound iike the $2bn were mainly supposed to cover Tesla's portion of the GF project (read the various press reports back in Feb 2014)

- And yes, that $2bn is gone/spent in my opinion (that's the main reason I came back to this thread to respond):

Let's keep things simple, disregard items like A/R and A/P and just look at rounded cash numbers from the quarterly reports:

In Dec 2013, Tesla had around $ 0.85 billion in cash

In June 2015, Tesla was again down to $ 1.15 billion in cash

In Sept 2015, Tesla had around $ 1.42 billion in cash (but of course raised another $700+ million earlier in that quarter, August 2015)

You can't add the $750 million again at the end of the quarter. As of Sept 30, 2015 the remaining portion of the money raised in the quarter is already included on the balance sheet. This means the small remaining rest of the $2bn in cash raised in early 2014 was burned (or "wisely invested for future ROI" if you prefer that term) during Q3 2015.

I estimated that only 10-20% of these funds were used for the GF by summer 2015. Yes, the $206 million is only about GF construction costs as of June 2015 (the next 10-Q will show how much they spent this quarter and hopefully correct the 2015 GF-related numbers) - but even if we add machinery/tooling already used in CA and then moved to Nevada, eg. for battery cell/module assembly, I have a hard time seeing how more than about 20% (that's why I used 20% as the upper limit) of the $2bn were used on the GF so far.

That leaves 80% spent on other business purposes - again, nothing wrong with that, but this means more fresh money will be needed to complete the full GF going forward..

Summary: Tesla spent most of money it raised in 2014 (the full $2bn, not chump change...) on other items while the GF in Nevada is still an unfinished hull at just 14% of the projected total size/output.

14% matches "one of seven buildings" very well, so the different reports add up (people claiming that the "full" GF will encompass seven buildings. At the moment the first building is being finished: http://bit.ly/1MeyT9S ).

Meaning there's no way Tesla can ever get close to 35GWh/50 GWh on cell/pack level output in the current building (maybe 5-7GWh for now?). For the full GF, Tesla needs the remaining six buildings going up in the desert until 2020. That progress will be easy to check thanks to drone videos etc.

Looking at the cash balance (even if cash burn is reduced in the coming quarters) Tesla will need a lot of additional funding* to complete the full GF between 2017-2020 (even if Panasonic chips in their part until 2020).

Now of course you say that this was money well spent and Tesla should spend more asap to reach its long-tem goals. We differ on the outlook/risks and the general strategy such as a need for a Model3 etc. (I don't need to repeat this portion in detail. I just wanted to clarify the numbers I used before leaving this thread for the time being).

_____

* The Model 3 R&D and tooling will also require additional billions between 2016-2020, the above was just for the GF. That's why I think a substantial amount of fresh funds will have to be raised in 2016 or 2017.�

Nov 5, 2015

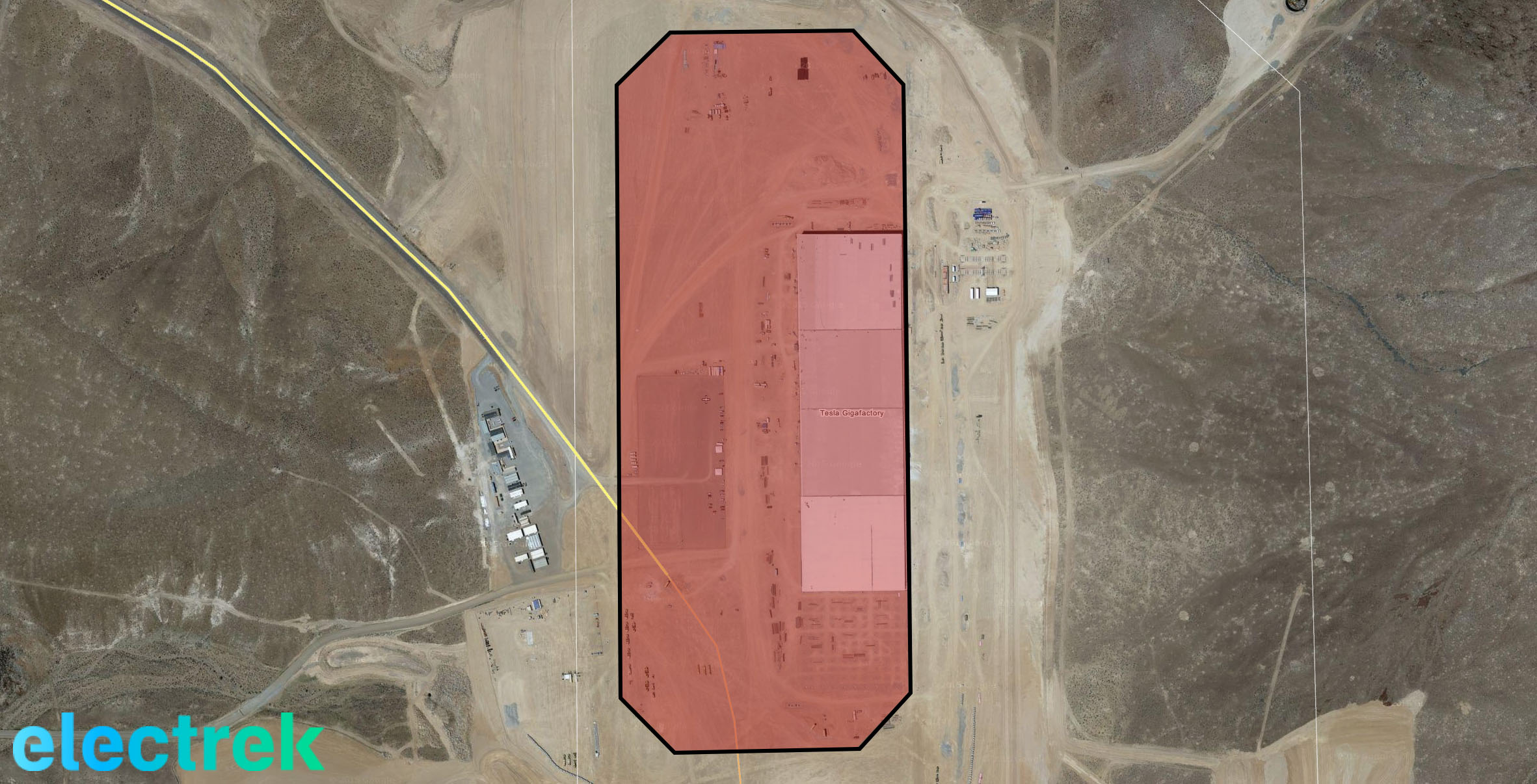

Model 3 I know you have a source for the clam of 7 buildings. Did that source give any information about the size of this 7 buildings? All of them will be the same size/form and cost the same? Or will it be some big buildings, and a some smaller? From what has been said from Tesla this first building should be 20-25% of the total GF. If it represent 20-25% of the cost? I don't know...�

Nov 5, 2015

chickensevil TFTF, I think we both just have different views on the implications of raising capital both in the past and in the future. I would actually agree that it would be prudent to raise capital in 2016 and have even posted as much to how I think this will go down with them hitting their stated cash flows so it will cause a pop in the stock... knowing this is the most likely outcome of showing green returns on cash (because this is really all financial people seem to care about) then planning to do a capital raise at that time would make sense. Which is likely why they only got 750M$ when they knew they could have got more. Why not wait for us to be over 300$ a share and do another raise?

That being said, I don't think that the raise will be stated for the purpose of tooling for the M3 or completing the gigafactory (whether they end up using the funds for that or not is a whole other issue). I am sure they will say it is for building a factory in Europe and China, which is what they have been hinting as for a while. With a nice share price they can get as much money as they would want with minimal dilution and be able to further accelerate their growth toward the goal of "millions of cars" by 2025.

So I agree with the notion of a capital raise, I just disagree with the reason they will do it.

But to the previous cash raises (outside of the 2BN one) was all to help them accelerate that growth of the business to handle more than anticipated volumes on the S and X, and to lay the groundwork for the entirely new business of stationary storage along with the R&D costs of other things. Which is why the funding sources keep putting them back up decently so they still have the money when needed for the gigafactory.

It is a perspective thing, I suppose, you look at it through bear tinted glasses and I through bull tinted glasses. Not sure I see where they are doing anything *wrong* with how they have spent the money since they:

1: have the funds still to keep doing what they are doing

2: holding high GMs on the core business and the GMs for the rest isn't too bad either (meaning you could easily make money if you stopped growing the business so rapidly)

3: have no apparently demand issues for anything they make so anything they spend seems to be money well spent

If you aren't implying/stating that how they are spending the money is wrong then I am not sure what your argument is? Just that they spent money differently than you expected them to? OK. That if they want to continue to grow rapidly them might need more money in the future than they have on hand? I'm fine with that.�

Nov 5, 2015

dc_h Has anyone done any estimates on sales from the first GF building and expected free cash flow? Based on tftf's 14% model, building one should produce 7 Gigawatts of batteries annualized by the end of 2016 or start of 2017. At that point, revenues would be ? 250 million per GW, or 1.75 billion, which at 15% margin would produce almost 200 million to reinvest in building 2. Based on more current estimates, the GF may be closer to 100GW than 50GW, so 14% could be more than 7GW. I think it would be instructive from an investment perspective to understand the investment needs and cash flow being generated by the energy business. If the Nevada plant is self sustaining, while doubling annually, that would leave new fund raising for European or Asian factories. One issue that will likely generate discussion going into 2017, is the level up process. Tesla, due to the current scale, tends to level up in bursts. Updates to the Freemont plant increase capacity from 800 to 1200 cars per week. The new line now allows 1600-1800 cars per week and perhaps more. The GF, being built in phases, may go from 7GW straight to 14GW, and then to 28GW, so investment will be a drain over a few quarters, and then production and revenue will quickly rise. This level up delay between investment and production has kept tftf busy since 2013 and I expect this will continue going forward. Better data will help create a more informed narrative and a better discussion.�

Nov 5, 2015

jhm My numbers are a little more ambitious. The equipment is about 80% of the cost of the GF, so about $80M per equipment for 1 GWh capacity. Tesla pays about half the equipment cost and collects 15% GM on Power products averaging $300/kWh. Thus, Tesla invests $40M and makes annually $300M in sales, $45M gross profit. Thus, an investment in equipment pays for itself plus 12.5% in 1 year.

If you want to allocate 2% of total property and plant to 1 GWh of capacity, that is another $20M Tesla invests. So at $45M gross profit per year, 1 GWh of capacity breaks even in 16 months.

Basically if Tesla begins with just $1B for property and plan and $0.5B for equipment, that is sufficient seed money to complete the GF in under four years. The beauty of the TE business is that it can scale just as fast as needed. Every dollar Tesla makes on a Power product can be immediately reinvested in buying more equipment. In fact, the 15 GWh of TE capacity pays for the whole GF in 3.7 years at full capacity. I suspect this is has something to do with why Tesla is so eager to get things rolling in Sparks.�

Nov 5, 2015

Perfectlogic I think a lot of people on here are way too optimistic about how gross margins turn into net profits, both when talking about Tesla's cars and the battery storage. At a 15% gross margin I don't think there will be any profit left after G&A and R&D is accounted for. It's important to keep in mind that there is always significant overhead that isn't included in COGS but still necessary. The reason Tesla would be willing to break even on the first sales is just to get the demand ball rolling so they know demand will be there when they get to scale and then they can start making money.�

Nov 5, 2015

30seconds Given the demand levels - sold out for 2016 - there should be plenty of room to actually make money on the energy side. I don't see any proof behind a claim of a 15% GM with basically 0 profit after G&A and R&D.�

Nov 6, 2015

jhm Seriously? The GF equipment should have an average useful life of 10 years. The idea that GM pays for this equipment in under 11 months means that there are about 9 more years of gross profit to pay for other overhead and net income. Put another way PPE on the GF is only about 2% of GF revenue. Scaling up GFs will lead to lower R&D per GF revenue, as R&D is pretty much independent of scale. A portion of G&A will scale with GF but much will not, so G&A as a fraction of revenue declines with scale. Of course, Sales cost do increase with revenue, but as a nearly commodity type product sales costs should be pretty lean. Moreover, considering that TE is sold out through 2016, sales costs pretty much come down to processing orders. So overall profitibility improves with scale and that leads right back to the question of how much capital must be raised in order to achieve scale. So here if the incremental cashflow from sell of Power products is good, it self-funds expansion.

Another thing to consider here is that Tesla controls the pricing at this point. They are pricing a Powerpack at $25,000, but just as well could price it at $27,500 and suffer no near term loss of sales due to price competition. So if they needed a 25% margin, they could price it that way. The advange of entering a the lower price is strategic. It accelerate a transition to batteries within the utility space, andit creates a barrier to entry for would-be competitors. These strategic advantages safeguard the investment in a rapid scale up. My view is that TE primarily exists to provide battery capacity for the automotive business where margins will be more durable longterm. A major automaker needs about 1TWh of GF capacity to support 10 million vehicle production. So the question is how to acquire this capital. Taping into the utility market for the next 15 years looks to do the trick.�

Nov 6, 2015

electracity  �

�

Nov 6, 2015

Perfectlogic @30second and jhm

I take it you don't follow many companies, but in general you don't make money with a 15% gross margin.�

Nov 6, 2015

Krugerrand And you don't build rockets for magnitudes less than ULA.

And you don't build a compelling long range EV.

And you don't start a car company.

And you don't simultaneously disrupt two trillion dollar industries.

And...�

Nov 6, 2015

electracity I agree.

The strategy seems to be about about rounds of raising additional capital backed by orders for both Tesla Energy products and cars. Musk is clear he wants a much bigger company. There is no possible way he thinks he can accomplish size through cash flow.�

Nov 6, 2015

Perfectlogic Yes I'm sure Elon can defy gravity too and turn water into wine. Discussing Elons businesses using logic and data from the market is futile, nothing applies to the company run by a god.�

Nov 6, 2015

Krugerrand Well that's an interesting response considering he's done several things that nobody else could or said could be done, all related to 'business logic and data from the market'. I'd say your response is because you've got nothing to counter the reality of what's going on and what's about to be done, including the success of Tesla Energy regardless of final gross margins.�

Nov 6, 2015

Rarity Musk will have to raise more money. A whole lot more money. The money that he raised for the gigafactory has gone to other productive places, so he will have to raise more money in order to do the gigafactory.

These facts are not profound. Just a day in the life of a rapidly-expanding startup company.�

Nov 6, 2015

Perfectlogic Business logic and data from the market was on Elon's side when he started Tesla. Many may have thought it was foolish, but the battery technology to make the Roadster was already there when he started, he didn't have to turn water into wine. It's kinda like 95% being sceptics on the prospect of solar in the next 5 years when the data clearly shows that the industry is on the cusp of a huge boom�

Nov 6, 2015

Model 3 From what I can see in your picture it looks like the current building is about 25% of the total complex if they have some space between the buildings, if not closer to 20%. Definitively more then 14% - if they have not expanded the area the building will occupy from the original plans. So no, all buildings (if it will be 7 - and they stick to the planed areal) can not be equal in size. And then probably not in cost either.�

Nov 6, 2015

chickensevil I'm not following you on this line of reasoning... They aren't doing anything "magical" with the gigafactory either... Make a large number of something and it tends to lower the costs. This has been the way of business since the invention of the loom and luddites getting upset over losing their textile industry jobs back in the 1800s. And taking something back to it's source components and building up from there is also not very "magical"... why haven't more people done these things? beats me.... Maybe people haven't been willing to take the huge risks and sink all that capital into it. The world needed someone with a ton of money to go... "You know, I don't need this money, I can live off a few dollars a month. How about I make the world a better place instead" before these things took place.

Apple didn't actually do anything special either. All the stuff they put together in their first iPhone not only wasn't "new tech" but Nokia had arguably a better "iPhone" before Apple did. So why did Nokia fail, why is Apple the one credited with disrupting the phone/portable media/internet access/and others industry and why were they the ones to succeed?

Point is, business logic and data is still on Elon's side.�

Nov 6, 2015

Perfectlogic I'm not saying they are. I am arguing that from the basis of looking over the income statements of a lot of companies it is unlikely that they will see any significant profit with a 15% gross margin. Take the HDD/SSD manufacturers as an example (SNDK, WDC, STX), a business that is kinda similiar I guess, they are at around 15% in SG&A+R&D. Where are all the companies making heaps of profit with 15% gross margins? Even if they managed to squeeze out a 5% margin on that 15% gross that is still only 3.3% after tax, there is just no way they make a significant amount of money on 15% gross.�

Nov 6, 2015

dc_h The logic was on his side? So you think he was right in 2003, but now that Tesla has made it through the first ten plus years, built a global sales model, acquired one of the largest plants in the US for almost nothing, created an energy company on the coat tails of the car company, building perhaps the largest manufacturing site in the world (Gigafactory), built a multinational charging infrastructure, that now the tide is against him? This is so out there as to almost avoid contradiction. The logic of Tesla is much more sound today than it was in 2013 let alone 2013. Tesla has changed more since 2013 than probably any other manufacturers has in the last decade. From proving they could mass produce a luxury, high performance sedan, to now proving they can repeat that with the Model X and advancing the core technical leadership of their cars at an accelerating rate.

They are moving to a growth rate that I think will likely be over 60% for the next 3 years, as Model X and Tesla Energy sales combine with the Model 3 introduction. Hyperbolic arguments against Tesla's entire business logic and continued existence encouraged me to buy in 2013 and still inspire me to acquire on dips. I look forward to see how our differing view of the future pans out over the next few years.

�

Nov 6, 2015

jhm Perfectlogic, thank you for insulting me personally. Kindly show me your math and justify the assumptions you hold to be true. Specifically, tell us how much incremental R&D will be spent on TE that was not spent on other Tesla products. Likewise incremental SG&A not otherwise spent on Tesla. Additionally break out fixed and variable components. Then you can back into the scale needed to turn a profit and the time it will take for the Gigafactory to break even. In short, cut your condescending crap and show us your analysis.�

Nov 6, 2015

Krugerrand ???? No other car company had succeeded in many decades. It's about a whole lot more than technology. The same goes for SpaceX. If everything was there already on Elon's side then it also existed for anyone else's side too, but nobody stepped up to the plate because business logic and data said you'd have to be crazy to try either company. How come Nissan didn't step up to the plate and produce a long range BEV? GM? Business logic and data per you suggests they should have along with every other OEM. With the technology out there, why didn't someone else strap together 7000+ laptop batteries? Why did they go with large format ones?

We know from history that both Tesla and SpaceX came *this close* to going under. Trying to now make it sound like it was a walk in the park is disingenuous at best. From the many interviews I've watched of Elon tell the history and other articles from current/former employees, it more accurately has been a journey of glass chewing and staring into the abyss. According to business logic and data, Tesla can't even sell their cars directly to the consumer in several states and certainly can't have continued on all this time without conventional advertisement.

If anything, Tesla and SpaceX prove that business logic and data isn't worth the paper it's written on, but hard work, determination, a balls to the walls attitude, and a sincere intent can accomplish the impossible.�

Nov 6, 2015

30seconds a. You are wrong about the first point

and

b. You also managed to not understand my point - which was I am sure that gross margins will be higher than 15%. They were able to easily sell out 2016, implying that they probably could do the same at at GM of 30%, 40% or possibly even 50%. This is not a stupid team. Profits will be used to fund further expansion so I doubt that this is breakeven product.�

Nov 6, 2015

AudubonB Mild-mannered Moderator here -

Play nice, everyone, or there are going to be some Time Outs. Better yet, take the weekend off and cool down. There are any number of ways the points several of you have been making could have been written in far less inflammatory ways than what's been posted over the past two or so pages.�

Nov 6, 2015

Perfectlogic The discussion was about the profitability of tesla energy sales next year at the guided 15% gross margin. Not a longer term view or tesla as a whole.

- - - Updated - - -

If you wan't to determine the profitability of a 15% gross margin I would say a good way to start is by looking at what kind of expenses other companies have, from there you can adjust your expectation based on how you think Tesla might differ from the lot. But given that every single company has SG&A+R&D spend above 10% and often 15%+ I think it's pretty reasonable to discount any net profit from the gigafactory next year assuming the 15% guided gross margin.

- - - Updated - - -

Clearly TSLA and SpaceX made sense, otherwise it wouldn't have worked, unless you believe magic made it work. If it didn't make sense to someone it is because they don't understand all the factors. There is no doubt we would have to switch out the dirty ICEs in time, it was just a matter of when and with what technology. The Prius gained traction in the early 2000s and the Roadster helped prove the concept, the major auto makers should have taken EVs much more seriously at this point. In any case now seems way too late as EVs were clearly gaining traction several years ago, there was more than half a million Prius sales in 2010.

"We know from history that both Tesla and SpaceX came *this close* to going under. Trying to now make it sound like it was a walk in the park is disingenuous at best."

I'm not making it sound like a walk in the park, I am just saying what he did makes sense. I'm not sure why it upsets you that I don't worship him like a god.

- - - Updated - - -

See my response to dc_h, you seem to have misunderstood the premise of the discussion.�

Nov 7, 2015

electracity I pointed out somewhere that both Tesla Energy and Tesla cars can't both benefit from gigafactory lower cell costs in this decade.

SpaceX is a mess, unless one prefers rockets made by twenty somethings new to the industry. I assume Tesla is better organized because they have better options in hiring experienced people. Outsiders have much higher interest in working for Musk than do the people actually working for Musk.�

Nov 7, 2015

Johan Please do elaborate on how SpaceX is a mess, since you seem to know more than most of us.

Also please do explain the first statement. Is it not going to be the same kind of cells in both cars and storage? If you mean that one cell can't go two places at once then no need to explain, but also kind of an unnecessary statement.�

Nov 7, 2015

Discoducky Would like to know that as well as some on this forum have worked with/for both�

Nov 7, 2015

electracity Gigafactory doesn't have the production volume to produce cells for Tesla Energy. Discussions about Tesla Energy margins seem to assume low cost cells.

I have a relative that is an engineer at spacex. With their turnover rate, eventually everyone will have a relative who works at spacex. Musk needs to demonstrate that he can build a large business where talented engineers want to work for more than a couple of years.�

Nov 7, 2015

Johan Great, thanks. Very convincing arguments.

BTW, do you GF doesn't have or won't have? And if so when?

That it doesn't have the production capacity currently, we can agree on seeing how it is currently producing exactly 0 cells. But you know how many it will produce in 2017, 2018 etc? Impressive foresight, please share.�

Nov 7, 2015

LargeHamCollider SpaceX is not only not a mess, it is by far the most efficient launch provider in history. SpaceX went from zero to orbit for a couple hundred million, this is a full order of magnitude less than any other country/company (and likely closer to two orders of magnitude for most). They've been scaling up at an incredible pace, it was on the basis of Musk's ridiculous work with spaceX that I first invested in Tesla. I don't think people outside the aerospace industry understand just how impressive the achievements of SpaceX are.

One failed launch does not mean that the whole company is a mess.�

Nov 7, 2015

electracity You obviously don't work at spacex. Got a link to their financials?�

Nov 7, 2015

pmadflyer I thought the tesla energy cells would continue coming from the Panasonic factories in Japan. The vehicle cells and the packs for both energy and vehicles would be produced at the GF. However, unexpected demand is driving cell production at the GF for Energy products at the end of next year.

I could be wrong though.�

Nov 7, 2015

electracity Yes, the Tesla Energy cells will come from panasonic or similar. My only comment was on Tesla Energy margins being lower using these cells.�

Nov 7, 2015

pmadflyer It might make sense to have a few lines operating at a loss (with cells at today's cost) so that when the $100 kWh cells come off the adjacent lines, they have the kinks worked out, and a line of repeat customers.�

Nov 7, 2015

Krugerrand Making sense is entirely different than 'having business logic and data from the market on Elon's side', which is what you originally said, and which has been obviously not true.

Yes, actually you are making it sound like a walk in the park, like anyone with half a brain could have done it, that it was obvious and only a matter of time, and yet we have proof that none of that is/was true. Because if it was so obvious that the technology existed then Nissan, Toyota and GM would have strapped together thousands of laptop batteries and produced a Model S instead of Tesla. Because it made so much business sense to start an EV company, then nobody would have called the Roadster a glorified golf cart, or the Model S vaporware, and GM wouldn't have crushed their EV1s and instead would have spun off another company and called it EVs of General Motors and so on.

It is because of Tesla that the world view has begun to change about what is possible. It is because of Tesla that GM is going to at least attempt to produce the Bolt. It is because of Tesla that all the other OEMs are announcing new and improved hybrid and ev models. It isn't because it made sense to them, or because of business logic and data. Indeed the latter is why the other OEMs are so stubbornly clinging to their old business models and practices because to have to change means they might very well end themselves in the process. And to suggest, hint at, or anything of the like that a transition would have happened without Tesla and would have happened easily because 'it makes sense' is to not understand what's happened to this point, nor to understand the establishment and human nature.

I'm not sure why you keep mentioning God, magic and the like when I've not said, suggested or hinted at anything along those lines. But to be clear, I'm not upset about what you think. I will, however, correct misinformation when I come across it.�

Nov 7, 2015

Perfectlogic I think our definitions of sense and logic might be different. If you don't think Elon starting Tesla and SpaceX made sense (even economically) then why was it a success? Was he lucky? I'm not sure what you are getting at here.

"Yes, actually you are making it sound like a walk in the park, like anyone with half a brain could have done it"

No I'm not, where have I said anything like that? Ofcourse if Elon hadn't put a lot of effort into Tesla then we would have transitioned to BEVs anyway, just at a later time (accelerating the transition is a great accomplishment, he is a great entrepreneur). Elon didn't make some great breakthrough, the most important part of being able to make a viable (for the market) BEV is relatively cheap and energy dense battery cells and that was supplied by Panasonic, 10 years earlier the Roadster wasn't possible and 10 years later it would have been easier. It's like the people praising Steve Jobs for bringing us the smartphone or Zuckerberg for making FB. Both of these inventions would have happenend without them that is absolutely certain as we are a capitalist society. The Iphone came soon after the hardware allowed it and FB happened soon after internet speed allowed it, just like the transition to BEVs happened just after the battery cell tech allowed it.�

Nov 7, 2015

dalalsid You have a link yourself? They are parking excess cash in scty so it can't be too bad.�

Nov 7, 2015

Johan Of course no one has a link, since it's privately held. No need to quibble. Perhaps they're doing great financially: investing heavily in future growth or perhaps they're "burning cash". Even if we had a balance sheet we would never agree, since it's all about outlook.

Point in case is Tesla: the financial info is there, some say it's a great success story, some say they're heading for the abyss.�

Nov 7, 2015

Krugerrand Logic: a proper or reasonable way of thinking about something

Economical: giving good value or service in relation to the amount of money, time, or effort spent

It most certainly did not make logical sense to start a car company where none had succeeded for many decades. It did not make logical sense to start a private space company where world interest was at an all time low, and only a few entire countries had succeeded, and it's...well...rocket science!

Economical sense would be of a very personal opinion depending on who you are. Certainly for future generations, transitioning to BEVs has great economical sense, but for the people in the trenches battling the establishment, the naysayers, etc... they might have a very different take. They obviously feel it's important, but when all is said done they might also feel they sacrificed too much for others. We can all see that Elon has suffered.

Why they've been successful to date is because of a combination of a lot of factors, and yes, luck played a part. The luck part for Tesla was Daimler financing at the eleventh hour on the last day in 2008.

One of the biggest factors in success is because Elon does not do *it* for the money. He does it because he believes it needs to be done for our continued existence, plain and simple. There's an understanding that he's got to make money to do it, but the outcome is not to line his pockets with cash. Altruism really does count and makes a big difference.

Willpower is Elon Musk's middle name. It's been talked about by several current/former employees. The guy just will simply not give up and won't let anyone else around him give up. He's broadly intelligent, charismatic, determined and has a real knack for surrounding himself with very capable people of like mind. He doesn't think like most people. Wait But Why has the last installment of the Elon Musk articles up now and it's about this thinking process. The Cook and the Chef: Musks Secret Sauce - Wait But Why

I'm not convinced that mankind's transition to BEVs happens anyway without Tesla. I'm just not. And not until the Model 3 comes out do I think we can breathe a sigh of relief. I think without Tesla's push we choke ourselves to death. I'm also not convinced we get to reuseable rockets and to being a multi-planetary species without SpaceX.�

Nov 7, 2015

Perfectlogic You claim that it did not make economical sense to start Tesla yet Elon has made a lot of money doing it, so obviously you are missing something as it is not up for discussion that it did infact make economical sense.

"I'm not convinced that mankind's transition to BEVs happens anyway without Tesla. I'm just not. And not until the Model 3 comes out do I think we can breathe a sigh of relief. I think without Tesla's push we choke ourselves to death. I'm also not convinced we get to reuseable rockets and to being a multi-planetary species without SpaceX."

Sure, the beginning of the transition to BEVs just happened to coincide with the underlying tech maturing enough to let it happen, just like we wouldn't have the iphone or FB, or even google today if it hadn't been for the founders of those companies, nothing to do with the underlying tech really. There is a difference between technological breakthroughs and incremental innovation.�

Nov 7, 2015

dc_h Are you implying there is a public link to SpaceX financials, or that you have access to SpaceX financials? Typically only large 100MM plus investors would have such access to privately held SpaceX financials. Seems odd that Fidelity would pony up $1bn for an unsound, unsustainable enterprise, but perhaps you have more resources and privileged access than Fidelity?

You might want to stick to unsubstantiated claims about Tesla and the GF.

�

Nov 7, 2015

BriansTesla +1

10 or 15 years ago, how many of us would have imagined the success of Tesla and SpaceX today. Not me! I would have said it couldn't happen but I am really enjoying the ride.�

Nov 7, 2015

Discoducky

SpaceX and Tesla are pure innovation and yes, that may cause turnover but I see your definition of mess and mine differ�

Nov 7, 2015

Krugerrand I defined economical for you so that we could be on the same page. That definition had nothing to do with making a lot of money. But for argument's sake I'll go with your definition and repeat, Elon is not motivated by money/making money and that isn't the reason or a reason for why he invested in Tesla or started SpaceX. For Elon money is a means to an end, that end being sustainable transport and multi-planetary existence, not to line his pockets. He already was rich prior to starting SpaceX and investing in Tesla. He had it made. There was no logical reason for him to risk every last penny (which he did), except that he felt it was that important for the welfare of man. And again, investing in the two biggest capital intensive businesses to ever exist isn't economically logical. It's suicide and as we know, both companies were in fact about to die a horrible death if not for heroic efforts by a small group of people (and a bit of good fortune - thank you, Universe).

- - - Updated - - -

Isn't part of the turnover rate also related to having a bunch of interns?�

Nov 7, 2015

Rarity At Glassdoor (past/present employees review their workplaces), SpaceX has employee ratings as high as Apple's. Well above its peers in the rocket business.�

Nov 7, 2015

Discoducky Not saying the turnover rate is higher than it should be, but yes, would include interns that have been offered a full time position but declined.�

Nov 7, 2015

LargeHamCollider Not a serious answer, capability and the value of existing contracts are a good indicator of SpaceX' value.�

Nov 8, 2015

Perfectlogic Elon's motivation has nothing to do with my original claim. I feel like I'm treading water so I'm just gonna leave it at that, it doesn't have much relevance to the thread subject anyway.�

Nov 8, 2015

Oil4AsphaultOnly If you look at Tesla and Spacex's history, you'll find that they succeeded despite their businesses being unprofitable. Read "The engineer" by Erik Nordeus, or the biography by Ashlee Vance. You'll see the story of 2 companies and a man on the brink of destruction. It was due to the collective efforts of the entire company, Elon, AND their investors that they survived long enough to be the successes that they are now.

Also keep in mind that the Leaf and the Volt were both put on the drawing board as a result of the Tesla Roadster. Had that vehicle not existed, Lutz would never have gotten the greenlight to build the volt, let alone the bolt! http://www.newsweek.com/bob-lutz-man-who-revived-electric-car-94987

"When Lutz first proposed creating an electric car in 2003, the idea "bombed" inside GM, he says. "I got beaten down a number of times." ... "That tore it for me," says Lutz. "If some Silicon Valley start-up can solve this equation, no one is going to tell me anymore that it's unfeasible." "

With the business-as-usual attitudes of many major corporations, the EV transition would never have happened (or would've happened much later) without the tesla "thorn in their sides".

And without SpaceX, the ULA would've continued to charge the US Air Force cost-plus pricing for their rocket development and launches, as that's how all the incumbent "competitors" price their offerings!�

Nov 8, 2015

MitchJi Tesla's GM is clearly higher than 15%.�

Nov 9, 2015

jvonbokel Just because you won the lottery doesn't mean playing the lottery made economical sense. The financial reward was large *because* the risk of failure was so high.�

Nov 9, 2015

ScepticMatt For Tesla Energy products the target gross margin is 15% IIRC.�

Nov 9, 2015

MitchJi Agreed that Tesla's claimed GM is 15% , but I think it's clear that Tesla's GM is higher than 15%.�

Nov 10, 2015

jhm How cheap can energy storage get? Pretty darn cheap : Renew Economy

Anyone who hopes to understand the economics of the Gigafactory needs to understand how experience curves work and the strategies for staying ahead of pack in terms of experience. This article does an OK job setting this out, and so is a good starting point.

The essential ideas of an experience curve is that manufacturing, innovation supply chain efficiencies scale with cumulative production. Spcifically, the cost of batteries are coming down 15% to 21% everytime cumulative production doubles. The implication of this scaling principle is that advantage goes to those manufacturers who scale production most quickly. Thus, adding Power products to EV battery production enables Tesla and its supply partners to gain experience faster than producing EV batteries alone. In fact, demand for stationary storage can scale so much faster presently than EV demand that to ignore this market could imperil the experience gain needed for EVs. That is, there is a risk a that another battery maker could gain so much experience with grid batteries that they cut costs for EV batteries faster than Tesla would, if they were to ignore the stationary market. In any case, Musk and Straubel understand the importance of leading on the experience curve. So staying ahead means being able to drive down the cost faster. At first this is really sweet for GM. However, as GM widens this also motivates more competion to enter and try to get ahead on experience. Thus a common strategy for preserving experience curve dominance is to keep driving down the price, and this of course limits GM expansion. However, it greatly accelerates the expansion of addressable markets and technology adoption. So one can have a discipline approach to GM. On is to target a specific GM and keep lowering prices as costs fall. The lower the target GM is set the more aggressive the path down the experience curve. Now one can question whether 15% GM on Power products is enough to support the profit of an entire business. An alternative view is that this agressive GM is intended to accelerate the path down the experience curve, that is Tesla and partners will get below $100/kWh well ahead of any automaker and this will yeild a very handsome GM in the auto segment for Tesla. It is the 30% GM in Tesla's auto business that covers the massive overhead of running Tesla Motors.

I have shown that 15%GM is sufficient for paying for the Gigafactory. Now I am arguing that experience gain of doing so will also pay dividends in giving Tesla a cost advantage in auto, such that 30% GM in autos is sufficient to assure 10% profit across the whole enterprise. 80% to 90% of Tesla's gross profit will come from EV sales, not Power product sales. If one allocates SG&A on the basis of gross profit, then clearly the auto segment will cover the bulk of overhead.�

Nov 10, 2015

electracity If Musk had known gas was going to be $2/gallon in 2015 he probably would not have invested in Tesla. Ten years ago he probably would have said, like everyone, that gas at $2/gallon was probably fundamentally impossible.�

Nov 10, 2015

Gerasimental Utterly beside the point.�

Nov 10, 2015

Johan I don't think Musk put any thought at all in to the price of oil before investing in Tesla.�

Nov 10, 2015

electracity So you think a cost/benefit analysis of EV vs. ICE ownership was never part of the investment decision? You would have never heard of Musk if he was an idiot.�

Nov 10, 2015

Krugerrand Um...no. Watch his interviews, he's always been consistent and clear about why he invested in Tesla - the need for sustainable transport to save the planet and thusly mankind.

Now that I know you think this, it makes all your other posts make sense. You don't understand the point of Tesla, nor the man.

- - - Updated - - -

Definitely not a 'part of the investment decision'. Certainly a 'part of the marketing strategy' to convince others to get on board via investing, buying, supporting in whatever way they can.�

Nov 10, 2015

Johan I don't think it was an investment decision as in "what can I do that will make my fortune grow the most" but rather "how can I use the money I've accumulated best for the betterment of mankind". I know you perhaps don't believe anyone may think like this, but if you knew/read anything about Elon I think you would see that in his case this is actually the truth.�

Nov 10, 2015

electracity Are you responding to my post? It doesn't seem like you are. I only said that your Lord and Savior would have rigorously evaluated the cost/benefit of owning an EV to determine the viability of Tesla. Musk is able to do Tesla and SpaceX exactly because of critical analysis of financial viability. That financial viability comes from having sufficient demand.�

Nov 10, 2015

Johan Yes I'm replying to you. My point is that even if Elon somehow predicted or know Oil would be $1/gallon in 2015 he still would have invested early and devoted time to Tesla. I think he believes demand for EVs is only to a small extent influenced by the price of oil. (which seems pretty true, especially considering the simple fact that the huge drop in oil prices lately have done relatively little to influense the cost of gasoline for consumers, coupled with the societal trend of pricing CO2 emissions higher regardless of oil price).�

Nov 10, 2015

Krugerrand Yes, Johan was responding to your post.

Out of line and weakens your argument. It also tends to turn people off, both those who believe he is their Lord and Savior and those who don't.

That's not exactly what you said. You started off by claiming he would have never invested in Tesla if he'd thought the price of gas would be as low as it is today - which is untrue given what Elon has publically stated time and time again about how important he believes sustainable transport is to the future of mankind. Then you went on to say he did a cost/benefit analysis, which I'm sure he did but not for the reason or the outcome you think he did. He'd have simply done it as a part of 'How can I convince other people this is the way to go? - For starters, I can appeal to the economic sensibilities of BEV vs ICE'.�

Nov 10, 2015

Familial Rhino I usually read your posts because sometimes you raise some good points, but I find this tone very off-putting. Use this information as you see fit.�

Nov 10, 2015

AlMc I have been fairly disappointed/frustrated with many things TM/EM over the last couple months but I agree with Johan and Krugerrand on this one ( I don't think EM gives a darn about gas prices/oil prices) and feel you are losing your argument/credibility if you have to resort to this ^^ type patronizing ^^. Argue your point. Leave the patronizing off the thread. Thanks�

Nov 10, 2015

dhanson865 If you believe that, then you don't know Musks plan

The Secret Tesla Motors Master Plan (just between you and me) | Tesla Motors

Seriously read that and you'll see it isn't about cost of gas, it is about possible negative effects of burning more fuel.�

Nov 10, 2015

RobStark

When Elon first invested in Tesla the price of gasoline was below $2/gallon.

Adjusted for inflation the average price of gasoline for the last 80 years is $2.62/gallon.�

Nov 10, 2015

ecarfan As the last decade of car sales clearly demonstrates, EV sales have little to do with the price of gas, while hybrid sales have a great deal to do with the price of gas.

And as others in this thread have clearly demonstrated, and the evidence clearly shows, Musk is motivated to build and promote EVs because they offer a clear choice towards a sustainable energy-based transportation future, not because he wants to add billions more to his bank account.�

Nov 10, 2015

electracity I can read the risk factors in the TSLA prospectus.�

Nov 10, 2015

chickensevil It was stated in thread already that he invested when gas/oil was cheaper. What I want to add is that he has also always stated that growing up there were three things about this world he wanted to change.

Sustainable Transportation

Sustainable Energy Production

Making the human race have a "backup plan"

It has been stated many times by himself and those around him that he thought about electric cars for a very long time... As in during high school / college long time. Back when gas prices were under 1$ in the 90s.

Wise investment wasn't the plan. He has even stated that he went through the trouble of finding out he could live on something like 5$ a month and because of that didn't care if he lost all his money.

That being said, the Roadster would not have been possible if not for the auto industry becoming like it did. They outsourced everything... Everything except the motor. So they were able to invest all their efforts into the motor and get suppliers to do everything else for them. (Little over simplification but not much...)

Anyway, you should actually put a little effort into researching the people running a company before you start making crazy claims.�

Nov 10, 2015

jhm Gigafactory Renewable Energy Plans Slip Out | CleanTechnica

Getting back to the Gigafactory, this article has some good info including an extended quote from JB's UNR talk. Also note that one commentor came up with a nice 537MWh/day average solar production from the roof of the GF.

Does anyone have an idea of how much energy the GF will consume per year at full capacity?�

Nov 10, 2015

AudubonB A lot?�

Nov 10, 2015

RobStark Wal Mart stores consume 29 GWh of electricity per year.�

Nov 10, 2015

Cattledog Just spit-ballin' here, using the source of all truth, the internet, for my research. But if the initial assumption is close, this gets us an order of magnitude view.

Average mfr. facility uses 250kWh/sf/year. So at 10,000,000 sf, the Gigafactory 2.5 Billion KWh/yr., or 2.5 Million mWh/yr.

The rooftop will produce 537mWh/day x 365 days = 196 Thousand mWh/yr.

So the PV on the roof makes about 8% of the energy necessary to run the factory.

That's why they need hillsides for solar and wind.�

Nov 10, 2015

AlMc Geothermal should also be included in where they will get energy.�

Nov 10, 2015

MitchJi Hopefully they'll use geothermal or solar thermal for the heat for drying the cells.�

Nov 11, 2015

electracity I doubt they will use more than air source heat pumps for heat needs. But perhaps they will have significant simultaneous heating and cooling needs, in which case some sort of closed loop hydro heat pump may work.

Actually going after a significant geothermal energy source would be experimental. I expect their experimental plate is full.�

Nov 11, 2015

gigglehertz I've always assumed they would purchase power from a nearby geothermal plant, not drill directly underneath the factory. Kind of like how I could purchase "green power" from my utility which gives some amount of money per kWh to local or regional alt energy producers.�

Nov 13, 2015

electracity Is Tesla Energy constrained by cell availability?�

Nov 13, 2015

ecarfan At this moment that seems very likely. As someone who placed a Powerwall reservation the day after the Tesla Energy launch, and does not yet have a Powerwall, I assume part of the explanation is that demand is greater than supply.�

Không có nhận xét nào:

Đăng nhận xét