Oct 30, 2014

Theshadows I use TOS, mostly on my phone now though. I'll use it on my computer to see if I can find the function.

Does anyone have a good TOS training course? There is so much stuff in there that it is way confusing for me. Not to mention I don't know how to make sense of what the benefit is.�

Oct 30, 2014

hershey101 Waiting until the afternoon before the earnings will allow you to lose time decay, but the IV rise will more than compensate for it. So, no, its not better to wait. Assuming the stock is at the same price today till Wedesday, options on a highly volatile stock like TSLA are almost always going to be higher wednesday than today. Remember, IV peaks in the hour or two close, and drops within two hours of the open the next day.

Also, believe me, if you think you have found a way to make money with minimal risk (or the risk reward ratios are in your favor), trust me they are not. I have been in HFT for several years, and done some automated trading related research. The algos are much smarter, faster, and have much better access to data then you or me can ever imagine. So always remember that "the odds are forever against you" (to modify the quote of Hunger games) when dealing with any form of derivative product.�

Oct 30, 2014

AlMc If you call TD they will set up a time to talk with one of their experts and give you a personal tutorial of TOS (I am assuming TOS is Think or Swim??)�

Nov 17, 2014

Theshadows How do verticals work?

When I go into the my trade feed on think or swim I see a lot of these types of trades. Both buying and selling them.

How do they work and what is their advantages/disadvantages? What is the logic for picking the strikes?�

Nov 17, 2014

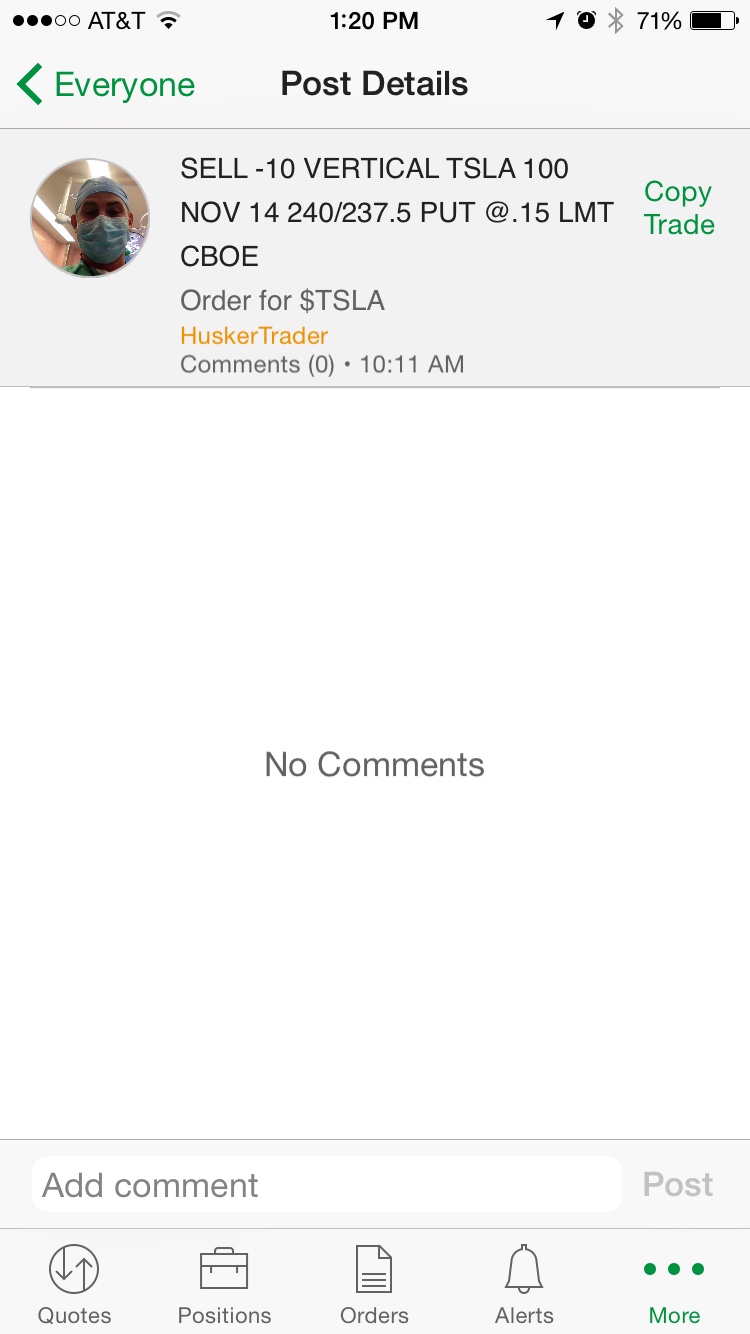

mershaw2001 That's just selling a normal put spread. They sold the 240 put and bought the 237.5 put as downside protection. Looks like they net 0.15 dollars per, and they did 100 of them so 1500 dollars net. Doesn't seem like a great trade. The downside is 2.50 loss *100, or 25000 dollars (less the 1500 gained, so 23500) if tesla falls to 237.5. My opinion is that the bid ask spread is stealing too much of your profit when you pair puts that are that close together. You lose prob 0.10 or 0.20 bid/ask spread on both options and only make 0.15. Based on that, the option play should be netting you 0.5 or so if you remove the amount that market makers are stealing from you. If you got 0.5 for that sort of trade, it would be appropriately priced. I'm not sure what the -10 means, perhaps I'm wrong that this person did 100 contracts and maybe they did 10. If that's the case, i don't know what the 100 is in there for. CBOE is the routing to the chicago board of options.

by the way, this is my interpretation of what was posted. please correct anything that needs correcting.�

Nov 17, 2014

Causalien -10 means selling 10 contracts. i.e. 1000 equivalent shares if exercised. Using verticles is a newbie mistake, or done when in a pinch to execute fast. It also combine the comission of both legs together, which makes it great for >100 contracts. The safer method is to do it one leg at a time. The commission is not worth saving at small volume when compared to the loss to bid ask spread. Another problem of the verticle is that TOS will wait for all condition of the order to be met before executing the option. So when you click on sell verticle in TOS, the program actually send out the two legs as limit order. If the stock is moving too fast, one side of the limit order might never be met and the order will get stuck. If you do a market vertical, then may the devil have your soul. Never market order an option.�

Nov 17, 2014

Theshadows I think it means they sold to close 10 contracts. My TD account always puts the 100 in there, that's the 100 shares that is in the standard option contract.

This was the only trade like this that I saw today, on some other high volitility days I have seen many of them both buying and selling and on both calls and puts. These are about the only types of trades I see in the my trade feed area so I was wondering what made them so popular.�

Nov 17, 2014

Johan They're probably not that popular. But the owner of the trading service probably wants to push and highlight them since it promotes trading in general and two comissions?�

Nov 17, 2014

Theshadows It looks like it's a Twitter type feed for trades. When I buy or sell it asks me if I would like to share it with my trade. I always say no. I see them from many different users when I look at the feed on high volume days.�

Jul 13, 2015

MitchJi Hi Dave,

Forgive me if you have already moved on.

I agree with buying on dips for long-term, but not for short-term!

For short-term I think this makes more sense:

Robert's response to that:

Of course combining buying on dips with the strategy I suggested above is even better if the timing is correct. And now might be a good time to try that if you share my opinion that the next 3-6 month's are an unusually good opportunity to profit (long) on Tesla.�

Feb 27, 2016

Blip Awfully quiet around here...�

Jun 8, 2016

Jonathan Hewitt I was looking at IV for the At the Money options around the end of quarter delivery numbers. Here is what I found for the $235 calls:

Jun 24th: 27.73 %

Jul 1st: 29.98 %

Jul 8th: 29.58 %

Jul 15th: 29.77 %

You see a small spike for the 1st, even though I doubt we will get the numbers that day. You then see a slight decline after that, but still ~2% higher than the June 24th IV.

I don't think the market is pricing in the delivery number reveal if there is only a 2% higher IV post delivery numbers. Looking at the last quarter isn't that helpful because of the Model III event. Using the OptionsHouse volatility chart it appears that the delivery reports 3 quarters before the last (January, October, July 2015) saw an IV run up of about 5% during the 2 weeks before the numbers were released and then volatility went up even more after the numbers release. This reaction post news is opposite of earnings, which usually sees IV go down after release.

Considering we are 3 weeks before delivery numbers I think there is a good chance IV will go up like it has the last 3 quarters, especially because IV is on the lower side when looking at it's 52 week range.

This knowledge might give one a trading edge when doing options trades. For example, it might work out well to do a call calendar spread with the July 1st options and July monthlies. The July 1st calls are over inflated by 2% if the delivery number doesn't come out on the 1st. This means the July 1st call should lose value a lot faster than the July monthlies thanks to a stronger theta decay and volatility increase keeping up the value of the monthlies.

This strategy would also work for puts. In fact, I think it would be a better trade for puts as I doubt TSLA will tank leading up to the delivery numbers barring some bad news coming out and in that case the July 1st put will expire worthless and you end up with what is basically a reduced cost put for July 15th. This reduced cost put can hedge your long position into delivery numbers or you can sell for a profit it if you are up on the position thanks to IV expansion.

Whether you choose puts or calls, in either case if there is a strong move then you would actually have theta decay move against you and you will have a large loss if held to expiration (however it is a defined risk trade). Using September calls instead of July calls would give you a wider range for potential profit and you could continue to sell new calls against your September calls all the way up to September to try and better your cost basis.

WARNING: I have not tried this trade before and am not recommending it. I've been doing some more advanced options learning as what I've been doing lately hasn't been working out real well for me and thought I would share some of that knowledge with everyone (and maybe get corrected by those with more experience!) I thought I would start some discussion in this thread because it seems that most people are just buying and then closing out straight calls and/or buying puts to hedge. I think we can be smarter than that?�

Jun 8, 2016

Jonathan Hewitt The bid ask sucks on this example according to the Bid/Ask I'm seeing after hours but here are some P&L graphs of a $235 put calendar to get my point across. One shows as of now, the other is with an assumed 10% absolute increase in the IV in the July monthly option. You would have theta decay working in your favor as well as long as you stayed in the green range.�

Jun 16, 2016

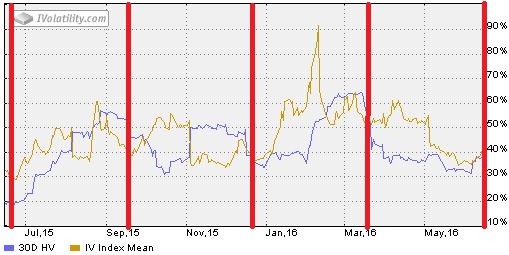

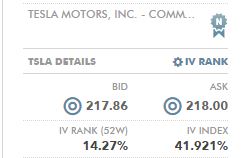

Jonathan Hewitt IV is still on the lower end compared to the IV over the last year. TSLA's volatility is 14% of it's highest volatility over the last 52 weeks. This is a misleading number because of the crazy volatility we had in February due to the crash in the share price, as you can see in the first chart. IV percentile is a better value to look at in this case. If you looks at the IV percentile, IV has been lower 41.9% of the time over the last 52 weeks. I expect the delivery numbers to raise IV and the ER to raise IV. Now that we are 2 weeks until the delivery numbers it may be a good time to start thinking about putting in a volatility based trade. I also uploaded the volatility chart where I put in a red line approximately 2 weeks before prior delivery numbers we have had over the last year.

�

�

Jun 16, 2016

Jonathan Hewitt What I mean by volatility based trade in this case is one in which you are long volatility (long Vega). In its simplest form, you are long Vega anytime you buy an option. You could just go out and buy a load of calls and puts and hope you make money when Vega inflates but while you wait for this to happen your options will lose value to time (Theta) decay and they will be subjected to the whims of stock price movement (Delta), which could either be very good or bad for your position.

To minimize the effects of Theta and Delta you can short options against your long options as anytime you are short an option you will have the opposite effects of buying an options. For this situation, you ideally want to construct a trade in which you are long Vega, but you have Theta working FOR you, not AGAINST you. To do this you want to short options that have higher Theta decay than the options you are long. As far as delta, ideally you want it to be near zero if you are trying to do a pure volatility play but you can either make them positive deltas if you think the stock is going to go up or negative deltas if you think the stock may go down or want to balance out and hedge a bullish portfolio.

Overall, you will make money as time goes on and volatility goes up. You will lose money if volatility goes down. You may also lose or make money due to stock price movement depending on what Deltas you chose and the stock price movement. If you choose a neutral Delta then the stock price will have to more a lot more for you to lose money due to stock movement than if you bought naked options.

You will not make nearly as much money on a play like this than buying naked options but you are probably more likely to profit. It also is a good strategy to use for hedging if the stock price doesn't move or moves opposite the direction the rest of your portfolio needs to go to profit.�

Jul 4, 2016

Jonathan Hewitt I thought I would give an update on the volatility trades I'm attempting. I continue to see people only use options for leverage and hedging so hopefully my posts get the group to come up with some new ideas. I am not the most knowledgeable person in this area but would like to continue to learn as much as possible (you can see I started the newbie options thread as a options newbie 3 years ago).

One trade I tried was a July/August $230 call calendar that will most likely be a loss. I put that trade on June 13th when TSLA was trading ~$220. It has a $20 range in which is will be profitable and based on the delivery numbers it looks like we will likely end up below that range. Once the July call I shorted becomes worthless I can continue to write calls against the August calls and maybe the ER will save the long side of the trade but I think I will be lucky at this point if that happens. The good news is that I will end up losing less money than if I had bought straight August $230 calls.

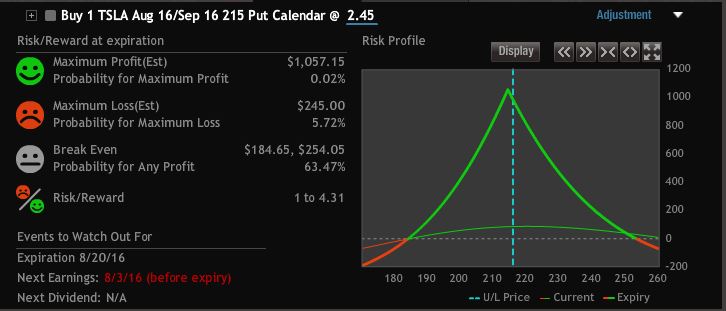

A more interesting trade I've attempted is an August/September $215 put calendar. I placed this trade on June 16th when TSLA was ~ $215. This trade is even more purely based on volatility. As I posted in my previous posts I've noticed 2 weeks before delivery numbers being reported that I've noticed volatility going up and then continuing up after the release of the numbers. I've attached a picture of how the trade looks as of Friday. What was interesting was that after suspension gate, Brexit, and the SCTY offer that even with the drops the trade did not lose much money, thanks to the corresponding increase in Volatility (Vega).

When I put the August/September $215 put calendar on TSLA IV was ~38%. It is now ~48%. My put calendar is up 35.7% even though the stock is at pretty much the same price as when I put the trade on two weeks ago. The pattern of a rise in IV before delivery number release came true once again. Hopefully IV continues to go up this week as is has in the past after delivery number release but it may not because Suspensiongate/Brexit/SCTY offer may have already raised IV as high as it is going to go for right now. On the other hand, based on bad delivery numbers and the ER in a month I think IV will continue to rise at least a few more percent.

My conclusions so far are that the shorter term calendars don't have enough wiggle room to withstand violent swings in stock price. I was hoping a $20 profit range would work out but it's looking like that won't be the case. The longer term calendars look better for capturing rises in Vega. By having a longer term calendar you have a much larger range to be right. In the August/ September calendar, for example, I have a breakeven range from $184.65-$254.05. It's possible to fall outside this range but I think there is a really good chance to be in this range over the next ~2 months. I don't plan to hold it that long but will if I need to. Some negatives I can think of for the longer term calendar is Theta (time) decay doesn't work as fast as a shorter term calendar, liquidity isn't as good, and there's more time for you to end up being wrong due to a black/white swan event.

.

�

�

Jul 9, 2016

ggr I moved this discussion out of the short term thread.

I've never actually done complicated options trades like this. Actually this is relatively simple spread compared to people who do iron condors etc, but my point is that my options trades are usually one-sided. But your example piqued my interest, and I have a spare afternoon.

First, I tried to reproduce your actual numbers. Now, my broker is ETrade, and maybe the quotes are broker specific. And, I'm completely ignoring the TSLA part of your logic above, just talking about the raw SCTY trade.

The first thing is that your $8.15 was the last trade of the $240 puts. However, the Bid/Ask is $6.80/$7.80. That is, the stock moved without the options trading again. Realistically you might get $7.30 for this put (the average of the bid/ask spread).

The $21 puts did trade. The b/a spread is $5/$6, last trade $5.50 as you show.

Above, you calculate maximum risk as $3 (which is the difference between the two strike prices) less $1.80 (the money you already got), so the maximum loss is $1.20. The maximum return is when you get to keep all of that $1.80. So your maximum loss is actually 67% of your maximum gain. Failing to take into account the lack of trading of the write-side option is where your calculation went wrong. You would be right if you could actually execute the trades as you wrote them, but without further movement in the underlying stock you'll never be able to do that. Actually, movement in SCTY will tend to move both ends of the trade, so you'll probably never be able to do it. In fact, even my trade might be impossible.

This is one of my big problems with "paper trading", which a lot of people recommend to beginners. It is easy to convince yourself that you'd have made a fortune if only you had real money, but in reality either the trades wouldn't ever have happened or you'd get the timing wrong or something. All you can count on is that you'll never make as much as you thought you would. And the fortune you make may be negative.

The good thing about this is that, like you, I followed the link to optionsprofitcalculator.com (thanks @MitchJi) and learned a lot about how the time value affects early exit from a trade like this. Suppose the deal goes through and on July 30 SCTY goes instantly to $26. You could probably exit both puts and get 12.5%, in only 3 weeks. Of course you'd make a lot more by ignoring the lower strike, and just selling the at-the-money puts, but then your downside insurance is all gone. If the deal tanks and SCTY goes down to $21, I can probably exit for only 15%. Note the disparity... time value works against us here.

The next good thing is that I knew ETrade allowed me to do these kinds of trades, but I'd never tried one. The way it works is I enter both ends of the spread, but instead of pricing the individual trades I just say "I want to get $2" (a little up from $1.80). This makes my downside $1 and upside $2, for a slightly better outcome. Of course the trade might never execute. I put it in for 10 contracts of each. We'll see, and I'll report back.�

Jul 9, 2016

MitchJi One more thing about that trade (I have not bothered to analyze if this has a positive or a negative effect on the trade, my guess is positive) is that the high put price is due to the IV, not the SP. Which means that it could easily go away (and probably will) without a corresponding change in the SP.�

Jul 9, 2016

Jonathan Hewitt TSLA's volatility has spiked to one of the highest points it's been in the last year at an IV of 58.6%. I was hoping it would go up at least a few more percent after delivery numbers and was shooting for 5% but it looks like the delivery report rose IV by 10.6%! The current IV was matched a few times over the last 52 weeks but only greatly surpassed during the February SP crash as you can see on the chart below.

My Short August/Long September $215 Put Calendar spread is now trading at $4.325. I originally purchased it for $2.45. That means it is now up 76.5%. Last week it was up 35.7% and TSLA was at about the same share price as it close this week and surprisingly close to when I bought it back in June. The amount Volatility can affect a calendar has really surprised me! From here I don't know if Volatility will maintain it's high value until earnings or not. It would probably be smart to book some profits at this point but I think the upcoming ER and the pending SCTY offer will keep IV high. Luckily time decay is in my favor as I am short the nearer term option. While I may lose some of my gains if Vega goes back down I will make up for it a little bit from Theta decay.

]o

�

Jul 11, 2016

ggr Indeed, it expired unfilled.�

Jul 17, 2016

Jonathan Hewitt Latest update on my August/September $215 put calendar: It is now worth even more at $4.80 per contract, or a 95.6% return. If you remember, I was concerned IV would drop and it did. It actually went up to ~63%, then ended lower than last week (was 58.6%, now 53.85%). If I am looking at it correctly, the reason it went up despite IV going down is that Theta Decay provided more value to the calendar than it lost from IV going down. Now that we are getting closer to the short option expiring it will be decaying a lot faster. My platform shows a Theta of $6.39/day for the spread.

If I was risk adverse I should have sold a long time ago. My prediction is IV will stay more or less in the same range until earnings and that I will continue to make money due to time decay. IV may go up and down due to the master plan coming out tonight and SCTY acquisition based news but I don't expect any huge changes. There will probably be a large IV drop after earnings so I currently plan to sell this calendar the day of earnings release.

While I haven't closed the trade yet I think I can say at this point that this is definitely worth trying again. For those who have been interested in this trade I will definitely try to set it up again just like I did this time, ~2 weeks before delivery numbers release. Hopefully IV falls enough after earnings to give us a good setup as it has in the past. If IV remains high after earnings due to the SCTY acquisition then it may not make sense to repeat the trade. I will be sure to monitor the situation and post here my findings.�

Jul 24, 2016

VanE Thank you for your reply! It is indeed just a simple put spread. I've looked at my analyses again and, like you said, I used the wrong numbers, I took the numbers of the last trades, instead of the bid/ask numbers, those numbers are a lot closer together and make it thus not quite as profitable.

The problem for me with only selling the put is that the margin required for the trade by my broker is immense! It is more profitable for me to buy a lower put and let expire worthless.

Wow, that is a great option of ETrade. My broker unfortunately doesn't allow two-legged option strategies, so I have to buy the put option first and then sell the higher put option.�

Jul 25, 2016

neroden So, I've sold some SCTY puts (backed by loads of cash so I don't need to worry about the margin requirements). I'm more conservative than Mr. Hewitt so I've been happy with much lower returns, such as 25% (40-60% or more annualized).

The interesting thing, and the thing which causes me to consider this *advanced* options trading, is that SCTY options are all very thinly traded. I've had to feed them onto the market rather carefully; it can only take so much each day, I've had to spread it around to different strikes, and I'm sure the market makers are getting a pretty good deal out of me. I was doing this before with TSLA puts and they were very liquid by comparison, with much greater improvements being possible over the bid. It seems to me at this point that it's unwise to open an options position unless Open Interest in that particular option is at least 10 times the position you're taking, and 100 times is a lot better. It also seems much better to trade positions which have already traded the same day.

SCTY put premiums are still huge but they seem to be shrinking fast. The SCTY/TSLA arbitrage gap in the stock prices is also shrinking. I think this has to do with news reports making the merger seem more and more likely.�

Jul 25, 2016

Jonathan Hewitt After making a ton of money buying options in 2013 and then losing a lot of money buying options in 2014 and 2015, writing options makes up the bulk of my portfolio right now. Some of them plain, others part of more advanced trades like ratio spreads. After I've done a few more of those trades and am more comfortable with using them with TSLA maybe I will write about them here.

For now, one thing I have slowly realized over the last couple years of just writing plain puts is that sometimes they will increase in value (a loss to me) or not lose much value even with only small changes in stock price. This effect is because of Vega/Volatility. If the share price drops and volatility goes up then you get a double whammy. All of a sudden your put is super red. I never really paid much attention to why this effect was so pronounced before because I would just try to make sure I sold the puts on large drops and hope for the best. This works great when I time bottoms right, which isn't that often. I am hoping that by paying attention to Volatility that I can be more successful. The calendars that I am experimenting with will gain value (positive effect to me) if the puts gain value (negative effect to me) due to a Volatility/Vega increase. So even if the calendars I own are up 50-100% over a time period due to a Vega increase it's likely that the puts I wrote are losing me money over that time period. The best case scenerio is nothing happens to Volatility or share price because then BOTH positions makes money due to time decay. The calendars are meant to only be a small percent of one's portfolio because they are more risky than the puts but I think they will help smooth out your returns, especially when used when we know volatility will probably go up, like before the delivery numbers.

With all that said, I think selling longer dated cash secured puts is a great strategy and a lot easier to implement. Anything more than 10% total account annualized return with minimal effort is awesome. I may go back to just going that route depending on how things go...�

Jul 29, 2016

neroden Soooo, in hopes of getting TSLA stock at a discount, I sold some September and January cash-secured equity puts on SCTY which were in the money. (The premiums were so ridiculously high that if they were executed, I was effectively buying SCTY below $22, which if the merger goes through, is equivalent to buying TSLA below $180.)

With the potential stock runups related to the merger, I'm beginning to think they have decent odds of expiring out of the money. Even the $35s. I'm kind of disappointed. I guess that's the risk one takes with writing put options.... the risk of losing the upside of outright stock ownership. On the other hand, I've already been paid the premium, so I really can't complain too much.�

Jul 29, 2016

Mario Kadastik Well now imagine me in 2013+ when I first decided to buy a Tesla I also decided to buy TSLA. It was trading at ~$28. So I sold a bunch of puts at the money every month expecting to get hundreds of shares of TSLA, but instead getting the premium and the puts expiring OTM. I was too, oh well at least I get free premiums and I've already made 60% of what the purchase price of the shares would be so I'm super well off...

Then the squeeze happened and instead of benefiting on the 10x share rise I got 0.7x out of it... I can't afford to buy multiple hundred shares of TSLA now, but had I just gone through and bought those 300 shares when I had planned instead of selling the puts I would be far far better off today�

Jul 31, 2016

neroden I bought shares first, after realizing that they were less than a quarter of what I thought was a reasonable valuation. But I didn't buy enough and I'm still kicking myself. I bought more after that, including some which are still out of the money. It was only after the stock price exceeded my (pessimistic) valuation model that I started looking seriously at options as an improvement over good-until-cancelled limit orders, and discovered the monumentally high premiums on put options. Right now, about 10% of the entire portfolio I manage is in TSLA or SCTY stock outright, so I'm being a bit conservative before buying more, and the puts are one way to do that.

When the price dipped to $150 in February I was out of town and couldn't follow the news or trade (as I had anticipated). I figured my short puts would be executed, since they were heavily in the money. However, the guys on the other side didn't exercise them. :sigh: Apparently almost all long put holders don't even look at the stock price until the day before it expires; a lesson for me.�

Aug 4, 2016

Jonathan Hewitt To tie up loose ends I closed the $215 put calendar yesterday for $5.12 per spread before a volatility crush happened. I had paid $2.45 a spread so 109% profit. I should have held onto it because today it is trading for $5.75! I think this is explained by the IV on the August going down a lot more than the September. Apparently I have a lot to learn! In the future if I do this trade again maybe I will sell half and hold half through earnings.

I put on a trade yesterday before the end of the day using weekly puts. I constructed a very complicated "Spiked Lizard" which consists of 6 total options across 4 different strikes. It has no risk to the upside but you will potentially be assigned 200 shares on a large drop. In this case a drop below $209.32 would have gotten very painful very quick. I got very lucky we didn't get such a drop. Here is how it turned out:

�

�

Aug 5, 2016

neroden Wow, you're willing to try much more complicated things than I am. I just keep loading up on puts. I may end up getting assigned a million dollars in stock, but based on my long-term analysis, I'm OK with that.

The IV must have dropped massively in recent days, and I can't really figure out why. The put premiums have been shrinking weekly, by a *lot*. Can't figure out what's causing it to happen. They'll probably get too low for my taste soon.�

1/1/2015

guest As promised, here I am ~2 weeks before delivery numbers. I am debating on when to put on my Volatility based trade at this point. I think it will be successful again based on today's conditions but waiting until tomorrow or next week might be better. Let me describe my purposes and intent for this trade again as a refresher.

-I will short the sooner month option and be long the longer month option.

-Like last time, I've decided to make the time to expiration of the sooner month option larger than the gap in between the two options. This allows me to pay little money for the spread in comparison to the price of each individual option. This is because ~90 day options and ~60 options do not have a large difference in value. In this case I will be using November and December.

-It's a Volatility based trade. This means that if Volatility goes up the trade should make me more money, if Volatility goes down I should lose money. To be more specific it actually depends on the Volatility of each option but they should mostly track together. This confused me last time for a bit as last time the short option had it's volatility climb faster than the long option right before earnings, which made sense once I noticed it but I didn't consider it up front.

-Pretty much every time since Tesla started reporting delivery numbers at the end of the quarter volatility increased starting ~2 weeks prior to delivery numbers being released. Just because this has always happened before doesn't mean it will continue to happen.

-Both the option I am short and the option I am long will lose money over time, but the closer dated option will lose money faster. In other words, I am guaranteed to make money on this trade as time passes IF nothing else changes. Things WILL change but at least this aspect of the trade makes it similar to paddling downstream instead of paddling upstream. Buying straight calls is like paddling upstream.

-I have a brokerage platform that lets me trade spreads and saves commission over individual trades. Putting an order in for each option individually is at best a pain in the butt, and at worst will cause you to lose money.

-This trade will be a small part of my portfolio. It should be less risky than short term calls but I am treating it like short term calls as far as how much money I'm willing to risk.

-Strike selection doesn't matter a ton (except in hindsight). I don't know if TSLA is going up or down so I plan to choose an ATM strike.

-If Tesla goes to the moon this trade will lose me money but my short puts and LEAPS will make more money than I lose on this trade so I am ok with that.

-If Tesla has a big but not huge drop in price this trade should make me money. This is because big drops cause Volatility to go crazy. This should counteract some of the money I will lose on my short puts.

-If Tesla has the floor fall out underneath it then I will lose money on this trade despite volatility going up but at least I will not lose more than I spent on the trade.

-As a summary, this trade does best if share price doesn't more than +/- $20 (possible), Volatility goes up (very probable), and time passes (Guaranteed!)

-I am probably missing some important points but this post is already crazy long.

-If I decide to go ahead and put on this trade I will let everyone know shortly after doing so.

-This is not a trade recommendation. I am not sharing this for people to blindly copy my trade. I'm hoping people can add to this discussion and either decide this trade looks good for themselves or come up with their own trades. Helping me do better trades in the future would also be nice. I can NOT predict the future and I've only done this trade once so do not think I am confident in everything I have shared. If you do blindly copy this trade then it's all on you when it crash and burns.

As far as when to put on the trade, if you look at Volatility it is the lowest today that it's been in the past week but it was lower at the end of August. It's still at a good point but 5-10% lower would be ideal.

�

�

1/1/2015

guest Please remind me exactly what you're doing, because you left out a key piece of information. Is this correct:

Short November Call

Long December Call

?

Or are you doing:

Short November Put

Long December Put

?

Both are typically debit trades, but they have somewhat different behavior.

I am confused by your claim that both options will lose value over time; the short position gains value for you (by losing value for the guy on the other side of the trade).

Obviously if you're doing one of these you're doing something really complicated:

Short November Call

Long December Put

(I can't imagine why anyone would do this)

Short November Put

Long December Call

(This is slightly more plausible)

----

I'm still sticking with selling puts and waiting for expiration (and accepting assignment if it happens). If volatility is low at the moment, perhaps this implies that I should wait until earnings when volatility goes up and sell more puts *then*. Gotta remember to look at volatility.�

1/1/2015

guest You want to do Short November Call/Long December Call or Short November Put/Long December Put. If you look at the Profit/Loss curves it's essentially the same for both. This may be kind of confusing but if you play around with some P/L curves you will see that they basically do the same thing. The only main difference I can think of right now is that one scenario will end up with both options ITM while the other one will end up with both options OTM. This matters only if you hold until expiration because options that are out of the money can just expire whereas ITM options must be closed or exercised.

Hopefully the following explanation on the time decay portion makes more sense. We all know that all options experience theta/time decay thanks to having an expiration date. Time decay on an option you are short is beneficial to you. This is just like having a covered call on your stock, you want time to go by and for it to expire worthless because you get to keep the premium. On the other hand, time decay of your long option hurts you. This is like holding a naked call and TSLA not moving. Your options will lose value over time and eventually expire worthless if they are OTM. For the calendar spread, you have both of these dynamics working at once. The way we set it up though is so the overall position's time decay is in your favor as the short option will time decay faster than the long option. As time goes on both options will lose value due to time decay but you are ok with losing money on the long option due to time decay because you will make money faster on the short option assuming all other variables stay the same.

It's weird to think about but the prices of each option in the spread could go wildly up or down thanks to a large share price movement but your P/L could remain unchanged. This is by design of the spread, we only want to capture profit from Volatility change and Time Decay.

Shorting naked puts in low volatility is fine (I do it) but it's something to be aware of. When volatility is higher you will get more premium shorting a put and if volatility drops back down afterwards you will make money faster. Because of this you might want to short more puts at periods of high volatility. If volatility is low when you put it on and then spikes while you're short a put then it will probably look like a loser position until volatility comes back down or enough time passes to counteract volatility's effects. The biggest problem is usually volatility spikes during a large down move, which means you are double hurt if you are short puts. Just remember that share price direction makes a bigger effect on naked put value than volatility and at expiration the share price in relation to the strike is all that matters.�

1/1/2015

guest I prefer to short puts out-of-the-money, and I'm always willing to take assignment. (I'm only working in the situation where I have a reason to believe the stock will go up above my target price long term.) In the assignment scenario, higher premium means effectively lower buy-in price... and doing it later in a large down move means I'm getting a lower price, too. So shorting puts at high vol rather than low vol ends up being 100% good for the scenario I'm working with. I *have* to remember this.�

1/1/2015

guest Regarding your calendar spread, I note that TSLA routinely has higher premiums for puts than for calls, because it's hard-to-borrow. I suspect this will show up in different prices for the put calendar and for the call calendar, which should give you different rates of return.

It's clear that either calendar spread is a trade which has to be closed, correct? If you wait until after the first expiration date, all kinds of things happen and it stops doing what you wanted it to do. I personally avoid trades which *have* to be closed because you never know when I'll be called away on urgent business and unable to trade.�

1/1/2015

guest Yes, the puts will cost more, but this will raise the premiums on both the option you buy and the one you short so I don't think you are at either an advantage or a disadvantage in this case. There will be a difference in your starting point depending on choosing puts or calls but I would think you would see similar results percent wise from that point onward. I would have to run some scenarios to explore this further as I don't have any proof of this and it's quite possible I am thinking of this wrong. Thanks for questioning me on this!

It all depends on your trading style as far as when you want to close it. You are trying to pick the point in time in which the difference in value between the short option and long option is largest. Because picking this exact point in time is only possible with a time machine traders will generally set target a certain % return for calendar spreads. 30% profit is a popular target from the traders I follow as this is a decent return that makes it worth your time but not too high of a target where you end up waiting too long and lose your profits due to the trade going against you. This spread is different as I aim to capitalize on the volatility increase from delivery numbers and then a volatility increase before earnings so last time I closed it the day before earnings. If you hold all the way until the first option expires (I don't plan to for this trade) then yes, things can get interesting. If you have a profit generally you should close your trade before expiration of the short option. If you don't have a profit you can short the next weeks option. This gives you another short option to time decay against the long option and keeps the calendar alive. It's kind of like selling a covered call against stock over and over. The difference here is unlike stock your long option will expire so eventually you will run out of weeks to short against the long call but hopefully you end up with a profit somewhere along the way.�

Không có nhận xét nào:

Đăng nhận xét