Jan 20, 2014

Bgarret Thanks Dave,

I had remembered the quotes from the conference call, but thanks for getting the actual transcript. I republished some of the transcript, but changed the parts that were highlighted - and this is the difficulty of trying to parse the language on what Elon is saying...and what he is saying. I agree with your justifiable caution base on Q3 and Elon's comments, but he seems a little cagey on this, almost like his language on the secondary offering in May's conference call. Tesla did saturate demand in Q3 - to 100% of the demand for ZEV credits for the fiscal year from October 1, 2012 to September 30, 2013. But it is a new year and there is now 110% of the previous year's requirement to fill (based on 10% more cars sold) and everyone is at 0. Additionally, at the end of this year there is a 330% jump in demand with very little material changing in the way of new credits coming on the market.

In the conference call response Elon is specifically addressing 25% Gross Margins and not counting ZEV in it and saying they shouldn't use ZEV for modeling...I think this is correct, but it is also potentially a lot of sandbagging.

It is also interesting to determine how you pre-guide to a greater than 20% growth in revenue with a less than 15% beat on cars delivered (less than 6900 vs. less than 6000 guidance.) There is another 5%+ of revenue growth unaccounted for, or at least $30+ million in revenue from what source....a 5% greater uptake on options, maybe?

I think Tesla did exceed revenue by 20%....and I bet by even more than 20% as companies usually reserve some additional good news for the conference call. If you have a good idea where the additional $30+ million of revenue came from, please let me know.

TESLA REVENUE EXPECTED TO EXCEED GUIDANCE BY 20% IN FOURTH QUARTER SALES DRIVEN BY SUPERLATIVE SAFETY RECORD AND EXCELLENT COLD WEATHER PERFORMANCE TUESDAY, JANUARY 14, 2014 PALO ALTO, Calif. � Tesla sales in the fourth quarter of 2013 were the highest in company history by a significant margin. With almost 6,900 vehicles sold and delivered, Tesla exceeded prior guidance by approximately 20%. A higher than expected number of cars was manufactured as a result of an excellent effort by the Tesla production team and key suppliers, particularly Panasonic. The two key drivers of demand were the superlative safety record of the Model S and great performance under extremely cold conditions.

Here is another good link that breaks down some of the ZEV and Carb historical information by StopCrazyApp. It doesn't answer your question about Q3 2012, but those are hard number to get.

ZEV credits

Caution is definately in order, but I think that the ZEV is less than dead based on some of the points in this and the preceding posts.

Cheers...�

Jan 21, 2014

uselesslogin I saw this note which looks like a general Tesla is doing good analyst update:

Tesla Motors Inc (TSLA) Growth Is Just Getting Started: Stifel

But I was puzzled by this line:

"We are lowering our FY13 non-GAAP EPS estimate to $0.62 from $0.73 (Street: $0.59) to reflect in the increase in units vs. our prior estimates and our expectation for lower gross margin."

They are still modeling a 25.2% gross margin ex-ZEV and I guess they were modeling higher than that in the past. Still, I don't see how more units will lead to less gross margin especially when I am under the impression they used existing production capacity and it was the fact Panasonic was able to get more batteries delivered that caused the boost. Can anyone tell me if I am missing something?�

Jan 21, 2014

c041v I too was puzzled. The only contributing factors I could see would be increased labour cost (more O/T) or some large marginal component cost once a certain threshold was realized. Either way, neither of those make much sense to me, and I wouldn't think they would be enough for such a hit to the EPS. I think it's a misleading line, and the "expectation for lower gross margin" is the relevant part of that statement.

Curious to hear the thoughts of our resident experts...�

Jan 21, 2014

kenliles My guess is they are just correcting a over exuberant GM position by couching it in this language. The only other I can think of is that the increased volume is coming from Asia-Europe so for their model the new market costs factor into a trim of the GM. Otherwise I can't get there from here, either�

Jan 29, 2014

PeterJA Motley Fool calculation:

Tesla Motors Inc.'s Earnings May Be Easier to Guess Than You Think (TSLA)

�

Jan 29, 2014

chickensevil Just saw that, and was coming here to post it. I think this is the best breakdown on the pricings which I think is STILL assuming zero ZEV credits. So if we get anything off of that we will see even higher than .33 per share. If the market doesn't go ape-**** over a 100% beat on EPS... I am going to throw in the towel, lol. But seriously, I am totally buying more shares, because I feel like we are going to have another REALLY sweet ride

I am hoping to make as much as I possibly can over the next month or so to fund the purchase of my car, haha!

So on the for real, what would make the stock drop at this point? And I mean drop hard...

1. Something fishy in the financials when they announce.

2. Something horrid from NHTSA (although they have already strongly hinted that they don't see any real issue with Tesla's car, given they said that EV's are not worse than ICE, they just have different risks.)

3. More fires???

4. Some horrid court case rulling making Tesla unable to sell any more cars in the US? (stupid auto dealers)

5. Something that scares people away from them when they guide for 2014 and the giga-factory. (I have seen future expectations cause problems in other stocks...)

6. Tesla goes Union

Those are pretty much all I can reasonably think of over the next month or so to the earnings release... and most of those seem pretty out there as far as actually ever happening.�

Jan 29, 2014

30seconds this looks like it is mixing and matching GAAP and non-GAAP. In third quarter there it was GAAP $603m revenue, 24% margins, $56m R&D expense, $77m SG&A, net loss of 0.32/share. Per non-GAAP is was $431m revenue, 22% margins, $48m R&D expense, $67m SG&A, net profit of 0.12/share.

Replacing the $603m with the $431m but carrying out the same calculations you would get $541m revenue x 25% margins = $135m - $140.4m - $2.2 = ($7.4m) non GAAP loss.

Using the GAAP numbers and the $756m revenues with 25% margins = $189m - $70m R&D expense - $92.4m SG&A - $2.2m = 24.2m profit

needless to say neither of these is a particularly good way to do this, however given the big top line revenue beat (driven by 6900 sales) and that R&D expense doesn't scale with revenues, however SG&A may to some extent, it is pretty likely that the bottom line will be much better than expected.�

Jan 30, 2014

RationalOptimist I think you may have mixed up your GAAP and non-GAAP labels here? GAAP has lower revenues because of lease accounting...�

Jan 30, 2014

30seconds that's what I get for not proofing my work. very sloppy of me!�

Jan 30, 2014

Robert.Boston If you are bullish on short-run TSLA performance, consider buying calls instead of stock. For each dollar of TSLA price increase, you will realize a much higher % increase in call value than in stock value.

Call options have much more risk, of course: if you get the timing wrong, you lose. Long-dated calls ("LEAPS") largely step around that issue, but they're trading at a substantial premium these days.�

Jan 30, 2014

AlMc I would add that if you have not done options before and are considering them you should study them first to understand them better. In addition, commit only money that you are not afraid to lose. While I know this comment could apply to all stock/investments it is particularly true of short term options. I have seen both sides of 'weeklies' (short term options). VERY high risk/reward. Correctly timed (and watched closely) you can double, triple or even '10 bagger' your investment. I made 135% on 180s today in 3 hours. I have also lost an entire position in the same amount of time.�

Jan 30, 2014

Theshadows I agree completely with AlMc. I too have seen both sides. I always ask myself "how would I feel if I loose all of this that I am about to spend. More often than not it has happened, especially when buying otm options.�

Jan 30, 2014

chickensevil I appreciate the suggestions toward options. I consider myself a rather smart person, and although I get the gist of how options work, applying that thought into a logical order for them never seems to make sense to me. I I don't know what part of them I am not quite understanding... It seems simple in theory, but then the application of it kills me. I would basically need to have complete throw away money on a cheap stock to "play around" with them so I can understand it better, I am just not willing to risk the capital on the learning curve, lol.

When I first got into stocks, I took a huge risk, dumping a ton of money left and right on different stocks... but I felt like I at least understood the market basics to do that and not be completely throwing money away. It took me about 1 to 2 years from that initial purchase before I really felt like I understood the ins and outs of timing and analyzing and such, and surprisingly held rather flat (not losing but not gaining money). Options... I just... I dunno. I can't seem to get my head around it well enough to do.

Sorry for the slight derail of the topic here, haha! But I think for now I will stick with stock, maybe someday when I really feel like I have cash to throw away again, I will risk it and figure it out. Right now though, I need to be *somewhat* safe with the money, since I am planning to use a lot of it on my down payment (wouldn't want all my money just disappearing on me).�

Jan 31, 2014

Lessmog I think you just proved that bolded part. �

�

Jan 31, 2014

AlMc Interesting article: http://us.rd.yahoo.com/finance/external/tsmfe/SIG=13aup7ekv/*http://www.thestreet.com/story/12287550/1/teslas-second-wind-californias-green-stickers-running-out.html?puc=yahoo&cm_ven=YAHOO Concerns 'green/white' stickers in Cali and TMs advantage because of them.�

Feb 6, 2014

PeterJA Autodata strikes again

This morning, my broker sent me a Reuters story about Kia's new EV, stating the following:

This evening, my broker sent a "corrected" version of the story:

For a firm that claims its business is providing auto data, Autodata seems really bad at counting auto data. Last summer, their bogus sales data for Tesla provoked several FUD articles on Seeking Alpha.

Reuters fans may want to tell their journalist (James B. Kelleher) that Tesla's 2013 deliveries were:

Q1 4900

Q2 5150

Q3 5500

Q4 6900

total 22,450, so Autodata is incompetent or corrupt or both.

http://www.reuters.com/article/2014/02/06/usa-kia-electric-vehicle-idUSL2N0LA1BS20140206�

Feb 6, 2014

techmaven It would be relatively accurate if they were talking about U.S. only sales. However, that article has been amended to eliminate the Autodata reference.�

Feb 6, 2014

PeterJA Ah, amended again. Maybe the error was not Autodata's, this time.�

Feb 6, 2014

Norse It's easy to forget that there are other countries besides the US isnt it?�

Feb 6, 2014

Jonathan Hewitt There are? :O :O :O�

Feb 6, 2014

chickensevil Next you will tell me that the earth isn't the center of the Universe!�

Feb 6, 2014

Jonathan Hewitt Or that there are EVs out there that aren't Teslas!�

Feb 6, 2014

Clprenz Just Spit balling, any possibility that Tesla delivered 7,000 cars? Seems like something they would do, technically 7000 cars is almost 6900. I expect GM's were substantially good, due to huge increase in production output (27-28% GM). Reason: New Panasonic agreement started, ie. new cheaper price (more quantity, less $$), hence the pick up in production.

Now I'm not trying to start rumors, I just think that these are real possibilities. 7,000 cars, $109,000 ASP, 27% GM, 142 mil CapEx = $64,010,000 Profit EPS: $.45

What I expect? EPS of $.25+

What is priced in? Around $.20

What I want? $.35

What would rock my socks off? $.45�

Feb 8, 2014

EarlyAdopter Zero probability. It was already well into Q1 when they announced so they had a good handle on how many they delivered all the way to the end of Q4. If it was 7000, they would have said 7000.

More likely the number will be 6850-6890.�

Feb 10, 2014

Benz TSLA reached a new all time high of $199.30 today and it closed at $196.56 !!!

I must say that I had not expected that to happen before the release of the Q4 2013 ER and Conference Call on February 19th, 2014.�

Feb 11, 2014

emupilot Is it possible the 4th quarter results won't matter? Imagine this scenario: 6,900 sold in Q4 (which we know), 27% gross margin, Q4 earnings per share exceeding expectations, projection of 40,000+ Model S produced in 2014, lots of China reservations, with demand exceeding supply for the foreseeable future. It all sounds great so far, but we also know that a gigafactory will be announced. That is great for long-term growth, but what if Tesla says they are going to plow most of their earnings into that factory so there won't be much earnings per share for the next 3 years. Could that tank the stock?�

Feb 11, 2014

Benz Good question. But I think that they will find another solution to finance the gigafactory. Don't worry about it.�

Feb 11, 2014

austinEV Why would that be an issue? It isn't like any of us are expecting dividend checks (for the next 15 years anyway. when they are making bank selling 500k model E's per year the natives will get restless). They are supposed to reinvest their cash earnings back into revenue-generating capacity, thus growing the company without new debt or dilution. That is the *ideal* case, not a problem.�

Feb 11, 2014

emupilot Projected earnings per share as an important metric by which institutional investors (and their trading robots) evaluate stocks. We see it as a positive if Tesla invests its profits in future growth, but if big stockholders devalue Tesla because it won't have very much net earnings per share the next 3 years, they will sell and the stock will drop.�

Feb 11, 2014

brianstorms Also, we already know that Tesla won't be going it alone with the gigafactory -- per Elon's recent disclosures, other co's (read: other money) will be involved no doubt at some significant level.�

Feb 11, 2014

sleepyhead Projected EPS is not important at all, just look at AMZN.

The only thing that makes a stock valuable is potential future dividend payments. A stock price is the present value of expected future dividend payments and not expected EPS over the next 3 years or so.

What I am trying to say is that your scenario would not be an issue at all.�

Feb 11, 2014

DaveT This is exactly my view on EPS on a high growth company like TSLA.

For AMZN it doesn't matter what EPS they report since they're re-investing money into growth. Rather, AMZN needs to report fast-growing revenue and decent margins for investors to keep believing that the company will someday in the future be able to give exceedingly large amounts of dividends back to shareholders that will make their investment well worth it. Once AMZN growth slows (and it might actually have started), then they need to start showing more EPS since investors don't have the fast-growing revenue to convince them of huge earnings in the future which will lead to large dividends and repayment of the initial investment and more.�

Feb 16, 2014

Thumper Do we really know that the earnings call is Wed the 19th? The Tesla corporate site still does not list it as an event. It is usually up by now.�

Feb 16, 2014

AlMc Yes. I will look for references but that date has been mentioned by a couple sources. After close 2/19/14�

Feb 16, 2014

DaveT Tesla Motors Announces Date for Fourth Quarter Full Year 2013 Financial Results | Press Releases | Tesla Motors�

Feb 17, 2014

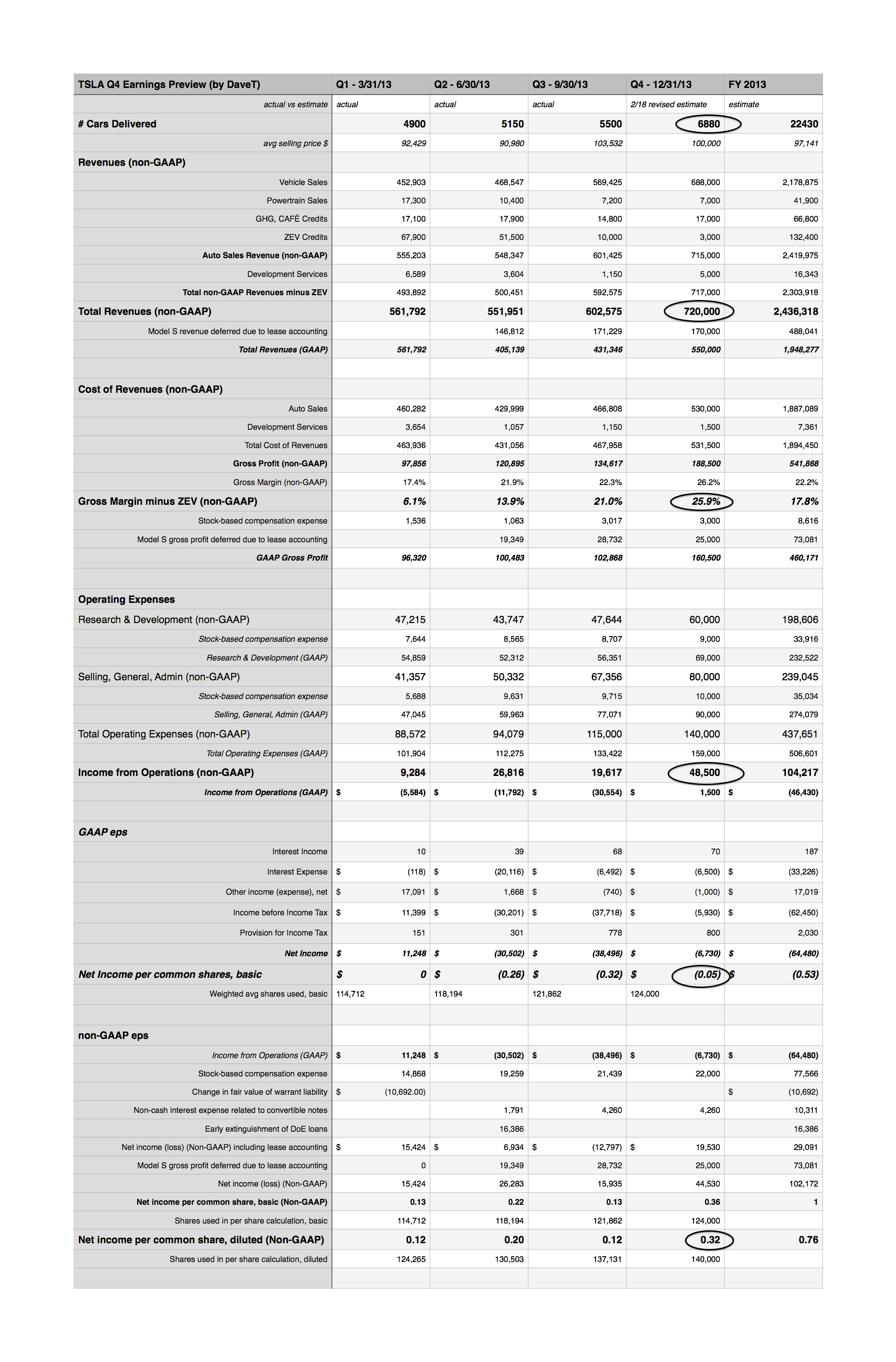

DaveT Q4 2013 earnings is just a few days away (Feb 19) so I�ll share my Q4 estimates. The TMC community has been generous so it�s an honor to contribute.

Quick Summary: (revised 2/18/14)

$720m revenue (non-GAAP)

25.9% gross margin excluding ZEV income

$48.5m income (non-GAAP)

$0.43 eps (non-GAAP)

$6.7m loss (GAAP)

-$0.05 eps (GAAP)

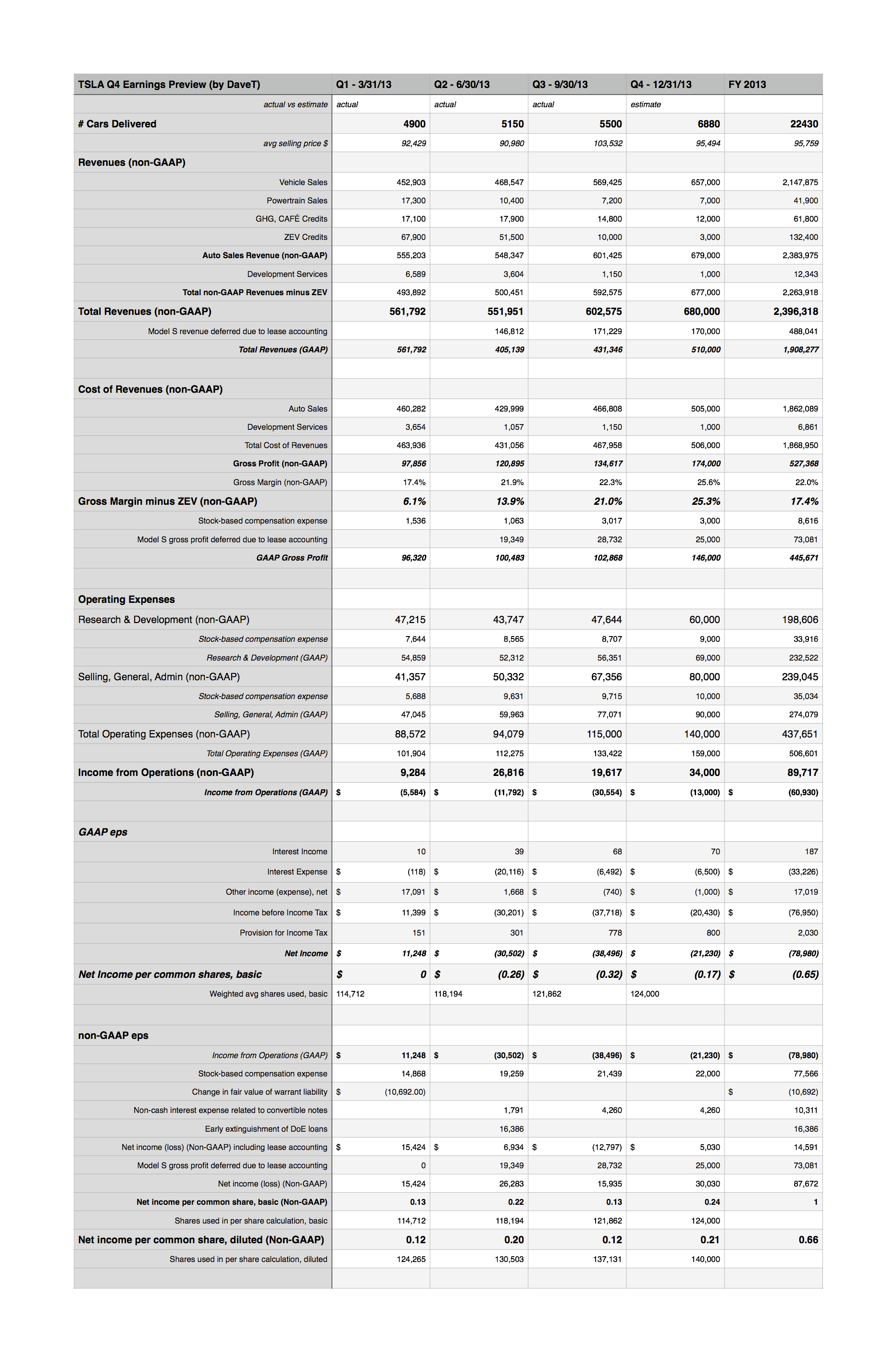

Previous 2/17/14 estimates:

$680m revenue (non-GAAP)

25.3% gross margin excluding ZEV income

$34m income (non-GAAP)

$0.21 eps (non-GAAP)

$21m loss (GAAP)

-$0.17 eps (GAAP)

Here are the key numbers to look out for.

1. Total Revenues (non-GAAP)

I�ve forecasted 6880 deliveries with an avg sales price of around $100k. The reason I�ve done this is because in Q3 I think Tesla benefited from early European signatures but in Q4 I think the number of signatures and fully loaded cars to Europe might have decreased. $103k asp for Q3 was an abnormally high number IMO. I think $100k is more realistic for this quarter and I�d imagine it to fall a bit in coming quarters as well. So, at $100k asp, I�m projecting total non-GAAP revenue at $720m.

Previous 2/17/13 estimate: $95k asp, $680m revenue

2. Gross margins w/o ZEV income

It will be important for Tesla to deliver strong gross margin numbers, around 25% excluding ZEV income. 24-26% would meet shareholder expectations, anything more would exceed.

3. non-GAAP income and eps

At $720m non-GAAP revenue and a 25.9% gross margin w/o ZEV income, I�m forecasting a non-GAAP income of $48.5m. I�m estimating a non-GAAP eps (diluted) of $0.32 eps. Tesla needs to report over $740m to exceed shareholder expectations.

Previous 2/17/13 estimate: non-gaap revenue estimate 680m, 25.3% gross margin w/o zev, non-gaap income $34m, non-gaap eps (diluted) $0.21 eps.

4. GAAP eps

I�m estimating a GAAP eps of -$0.05 eps, basic. The only way for TSLA to be GAAP positive this quarter is if they can have strong ZEV credit income along with strong revenue. If they can achieve $28m in ZEV income (with 6880 deliveries at $95k asp), then I�m showing a GAAP profit of $0.03 eps. However, Tesla management has said multiple times to expect near zero ZEV credit in Q4 2013. So, I think it�s wise to heed their advice, and thus I�ve forecasted $3m in ZEV credit. But it�s interesting to note that Tesla can be pushed into GAAP positive territory with strong ZEV income if that occurs in Q1 2014 or later.

Previous 2/17/13 estimate: gasp -$0.17 eps

Overall, I think Tesla will report a strong quarter, but the bigger question is will it meet shareholder expectations. With a high-growth momentum stock like TSLA, the analyst estimates sometimes are on the low-end. The reason being is because the analysts aren�t the ones usually holding TSLA stock. The people holding TSLA stock are Tesla believers (both institution and retail), traders and momentum investors. The typical shareholder is very bullish on TSLA and after the recent $60 rise in the past month, shareholders will have high expectations going into Q4 earnings.

Since Tesla pre-announced deliveries for Q4, the key part of the earnings report/call will likely be in other areas. Here are they key areas to watch out for besides what I mentioned above (ie., revenue, GM, eps, etc):

1. FY 2014 delivery guidance

Tesla will likely share how many vehicles they�re planning to deliver in 2014. While I think they could guide as high as 37,500, I think they�ll play it conservatively and guide at 35,000 units for 2014. I�m expecting this to meet shareholder expectations.

2. Battery Gigafactory

Elon is expected to share more details on the battery gigafactory. Some people have dilution fears (ie., the gigafactory will need a large stock offering to fund it). I�m optimistic that Elon will have a creative plan to tackle the gigafactory and financing it. Further, I don�t think the full financing amount needs to be done up front. If Tesla needs to raise $1 billion this year for the gigafactory (since it could take 1-2 years to build), then that�s only diluting the stock 1/25 (out of the current $25b valuation). I don�t think shareholders need to fear dilution as Tesla�s valuation is high enough to make dilution less severe. Further, Elon can involve partners and creative funding mechanisms to prevent stock dilution. Regardless, the battery gigafactory is going to be something to focus on in the shareholder letter and earnings conference call. Personally, I think if presented well the gigafactory presents upside to TSLA�s valuation.

3. Production ramp

If TSLA gives FY 2014 guidance then that will answer most of the questions regarding how fast they can ramp in 2014. However, if they don�t offer 2014 guidance for units delivered, then it�s going to be important for TSLA to show that it�s ramping and scaling production (or has immediate plans) in a meaningful way.

4. 2014 Gross Margin guidance

If Tesla offers guidance for 2014 gross margin, this has potential upside to TSLA�s valuation. More specifically, if TSLA guides to reach 30% gross margin by end of 2014 then this will be significant as it shows that Tesla is doing what most people thought they couldn�t do (ie., make high-margins on the Model S).

5. Model X and S demand

I don�t think this will happen in Q4 ER, but at some point this year people will wake up to the fact that demand for Model X is very strong. On TMC we know Model X reservations are already at around 12,000. And I think Model X demand could be at least as high as the Model S. At some point (maybe this year), people will realize that Model S global demand is at 50k+ units/year and Model X global demand is at 50k+ unit/year. If you do the simple math (100k units x $100k asp = $10b x 30% gross margin = $3b GM x .5 (expenses) = $1.5b income. Give it a 25x forward multiple and you�re looking at a $37.5b valuation or close to a $300 stock price). In other words, if Model S remains robust (ie., U.S., Europe, China) and Tesla is able to ramp production significantly, and if Model X reservation pace picks up (test drives are supposedly starting in Autumn this year), then it could become clear to the market that Tesla is headed to 100k Model S/X per year in a couple years, and that could take the stock higher. I wouldn�t be surprised to see TSLA print $300 at some point this year. That being said, if TSLA runs into challenges (ie., production challenges, safety issues, fires, etc), then the stock could get hit as the valuation is based on future earnings potential and a generous multiple.

Overall, I think Tesla is in control. They can release as much good news as they deem fit in Q4 ER. However, my hunch is that they�ll be somewhat conservative and space out the good news/expectations throughout the year.

Sleepyhead and I will be co-hosting a google hangout on the evening of earnings (Feb 19) where we�ll evaluate the earnings report/call and share our thoughts.

ps., I'm open-sourcing the spreadsheet I've created. Feel free to add your own numbers and share your creations.

download excel spreadsheet: View attachment Q4-2013r.xlsx

*note: I originally created the spreadsheet on Numbers (Mac) so I'm not sure if it exported the excel file correctly or not, so some functions/formulas might not work.

previous 2/17/14 estimate:

�

�

Feb 17, 2014

callnaveen Wonderful , great work Dave.�

Feb 17, 2014

callmesam @DaveT

Great work! Thanks for providing us the fruits of your hard work.

Offer of Assistance:

I've done a live blog of the previous few earnings reports on TM Forum (which I'm slowly wearying of) and wonder if there is any interest here. Most will listen live, but I'm a fast typer . . . help where people aren't set up for audio or flash (in the car, perhaps). Also not sure exactly where to post. I'm interested in the google hang out.

Tesla Motors, Inc. Third Quarter 2013 Financial Results QA Webcast - LIVEBLOG | Forums | Tesla Motors

Live Blog 2012 Shareholders Meeting June 4, 2013 | Forums | Tesla Motors

Live Blog Tesla Announcement April 26 - Elon Musk | Forums | Tesla Motors�

Feb 17, 2014

kenliles +100. Thanks so much�

Feb 18, 2014

Matthias Buhl Thanks Dave. I'm impressed by the willingness to share such valuable information to the TMC-Communiy. Great place on the internet ;-). If TSLA goes to 300 $ before this summers I consider spending some of my profits and coming to California to the shareholder meeting. Maybe I'll meet some of you guys there ;-)

- - - Updated - - -

Since Elon is likely to talk about the Giga Factory, what do you think could be the implications for gros margins? I heard somewhere that Elons goal is to achieve gros margins of 30%. Do you think this is possible without their own battery factory or did these margins also include own battery production?�

Feb 18, 2014

Robert.Boston I for one would appreciate this; I'm not going to be able to listen in. Moreover, I like to see things in writing.

Perhaps you could use the Blog feature here? Tesla Motors Club - Enthusiasts & Owners Forum - Recent Blogs Posts - Blogs�

Feb 18, 2014

kenliles was thinking the same thing. I plan to listen live, but had that same plan foiled last time and wished there was a good place to grab the text. would be a valuable service I think�

Feb 18, 2014

surfside i would definitely be interested in this -- i'm unfortunately going to be tied up in a meeting tomorrow during the conference call, so i'd love to see the text when i get out of my meeting. the last several conference calls they have been really slow in getting the replay posted online, so this would really be helpful.

thanks in advance,

surfside�

Feb 18, 2014

callnaveen Hi Dave,

By any chance if you have few minutes can you Please add analysts expectation also along with your results so that it will be easier to compare the difference.�

Feb 18, 2014

vgrinshpun Potential massive EPS beat by TSLA

From Tesla Motors Press Release: (Tesla Revenue Expected To Exceed Guidance By 20% In Fourth Quarter | Press Releases | Tesla Motors)

" Tesla Revenue Expected To Exceed Guidance By 20% In Fourth Quarter. With almost 6,900 vehicles sold and delivered, Tesla exceeded prior guidance by approximately 20%".

I recognize that above excerpt is cryptic, and I believe it is by design. I have seen more then one clueless gentlemen whining that these numbers do not add up. Do they really??

For all of those inclined to take this post with skepticism, just remember, that TM pulled similar trick during the Q1 (which I, along with many others did not recognized prior to the the ER release)

Per the shareholder�s letter, TM revenue guidance for Q4: "We are continuing to expand production and plan to deliver slightly under 6,000 Model S vehicles in Q4� ASPs are expected to be relatively flat sequentially as we continue to see a rich mix of options on incoming orders."

Based on data from 10-Q

Q3 ASP � all inclusive: $109.35K

Q3 ASP � w/o ZEV credits: $107.45K

Q3 ASP � w/o ZEV, GHG, CAF�: 104.768K

TM are using margin and ASP accounting exclusive of ZEV credits, but inclusive of GHG, CAF� credits. To be conservative, however, I will use ASP exclusive of all credits: 6,000 x 104.77K = $628.6M.

Revenue exceeding guidance by 20%: 1.2 x $628.6M = $754.32M

Revenue based on 6,900 deliveries: 6.9K x 104.77 = $722.91M

The difference between two above numbers - $31.41M - is revenue that is not coming from selling cars, with three distinct possibilities: ZEV credits, development services or combination of the above. To bracket these possibilities, let�s carry $31.41M to the bottom line at minimum of 27% (conservatively and unrealistically assuming development services only, recognizing that historically this margin was north of 30%), or at a maximum of 100% (assuming that this number represent ZEV credits only).

The following quote from Q3 Shareholder�s Letter is a reference to the conjecture on the development services: "Development services margin was negative this quarter due to the timing of revenue milestones and development costs incurred during Q3." In other words, the costs were booked in Q3, but the revenue was carried forward to Q4 due to the revenue milestones.

Assuming 124M outstanding shares, based on the above, the $31.41M carry to the bottom line either as: $31.41M x 0.27 /124M = $0.07 per share, or

$31.41M / 124M =$0.25 per share

Finally, the EPS from car sales, based on $104.45K ASP, $59.6M R&D, $80.8M SG&A, 6.9K deliveries and 27% gross margin estimated by Deutsche Bank in Jan 15 note on TSLA (DB TSLA Note)

($104.77K x 6.9K x 0.27 � $59.6M � $80.8M) / 124M = $0.44 per share.

Based on the above the EPS range is from $0.44+$0.07 = $0.51 to $0.44 + $0.25 = $0.69.�

Feb 18, 2014

DaveT Thanks, vgrinshpun for posting your thoughts.

You mention their press release is cryptic and I agree. One issue is that I can't find anywhere where Tesla actually guided for Q4 revenue. Yet, they said that they're going to exceed revenue guidance by 20%. They did guide for # units (almost 6000) and for ASP (relatively flat). But that does not necessarily mean total revenue since there are ZEV income, GHG/Cafe, development services, etc. But they did previously guide for zero ZEV income in Q4.

I'm starting to think that maybe the 20% revenue beat is based on Q3 revenue of $602m. Thus, Tesla shows Q4 revenue of about $720m. I had previously forecasted $680m in my models and I'll update my spreadsheet.

It's hard for me to see $750m+ in revenue coming in for Q4. But if they do when I enter the numbers (at 27% GM like you mention), then yes I get a $0.50+ eps (non-gaap) and GAAP positive eps of $0.08+ eps.�

Feb 18, 2014

vgrinshpun Dave, the Q4 guidance is in Q3 shareholder's letter, under the Q4 outlook heading, as per my OP. They give guidance for cars delivered and the ASP. The product of the two numbers is the revenue.�

Feb 18, 2014

DaveT Total revenue should be # Cars delivered x ASP + Powertrain Sales + ZEV income + GHG/Cafe + Development services.

Or if GHG/Cafe is included in ASP like you say, then # Cars delivered x ASP + Powertrain Sales + ZEV income + Development services.�

Feb 18, 2014

vgrinshpun Agreed, but like I said, I was trying to capture big picture. If we want to be precise and use your detailed formula, the beat will be even higher, as the 20% will be applied to a larger base.

What I did not realize is that if my interpretation is correct, TM will be GAAP profitable, as you indicated in your post. This could be really big.�

Feb 18, 2014

DaveT Yes, but the problem is that Tesla never guided for the total revenue including ZEV, powertrain, development services, etc. So we don't know what 20% over guidance for that number is.

When I input the numbers, if Tesla shows $740 revenue, 26.3% GM, then we'll see a $0.01 eps (gaap). Anything GAAP profitable would be big.

- - - Updated - - -

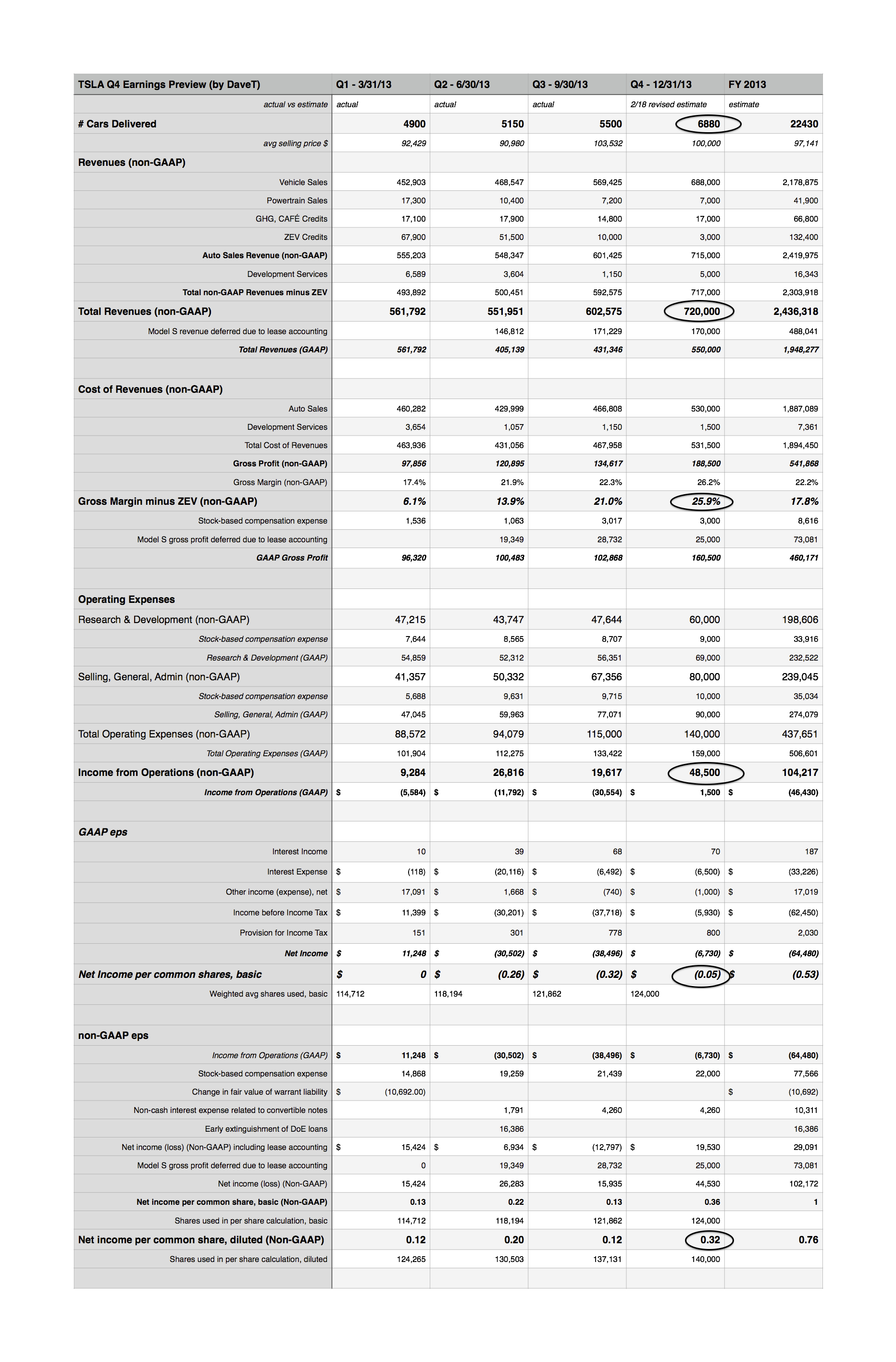

Here's my newly revised estimates based off of $720m instead of $680m in revenue. I've circled what I think will be important numbers to watch for.

�

�

Feb 18, 2014

vgrinshpun Well, unless you accept that their Press Release about the 20% beat is s half-cooked sloppy document, and I, for one, can't - the 20% increase in revenue taken together with 15% increase of deliveries can be true only if one assumes increased ASP or substantial non-sales revenue. Since IMO increase in ASP above approx $105K is simply impossible, the only possibility is that they had additional revenue that is not directly linked with sale of cars. And that is what my interpretation is based on.�

Feb 18, 2014

MikeC Yes, please. I can't listen to it at work.�

Feb 18, 2014

blakegallagher Thanks for posting your thoughts here Vgrinshpun. As always much appreciated. I think your right on about the additional non car sales revenue. The Mercedes B-class electric is due out in early summer 2014 in select markets and nationwide 2015. I got the impression last quarter they had done a lot of work on this and not got paid so it only makes since they would book some profit here. Sure hope we see a GAAP positive result. That would be pretty awesome.

2014 B-Class Electric Drive Car - Zero Emissions | Mercedes-Benz

There is a link to info about the upcoming B class electric. Looks pretty nice as far as 100 mile range cars go.�

Feb 18, 2014

DaveT I think might be putting too much weight into the ASP Q4 guidance and reflecting that as overall revenue guidance. All they said was that ASP would be relatively flat. That's fairly vague in my opinion. It could mean it drops $4-5k per car and that could still be considered relatively flat.

I looked over Q3 conference call transcript to see if they gave Q4 revenue guidance, but couldn't find anything.

I'm starting to wonder if they gave Q4 guidance to analysts in a separate note to analysts. Is that even possible?�

Feb 18, 2014

vgrinshpun Well, the car sales is by far the major portion of the revenue, and they explicitly listed ASP and deliveries first thing under the Q4 Outlook heading in the Shareholder Letter. I think that the bigger picture is what important here. The discrepancy between the revenue increase vs. increase in deliveries as compared to the previous guidance (both btw, should apply to the same base, i.e. if 6900 deliveries are 15% higher than 6000, it would not be correct to apply 20% revenue beat to the Q3 revenue, rather to the Q4 guidance) invariably means revenue additional to the car sales. If one accepts that the Press Release is a valid document, it implies that there is revenue that is not captured by multiplying the ASP by the deliveries. Everything, of course would be sorted out tomorrow. I believe that TM will report $0.50 to $0.70 EPS on Non-GAAP basis, without accounting for deferred lease revenue. I believe there will be major source of the revenues that is not priced in, to the tune of $30M+.�

Feb 18, 2014

DaveT If ASPs are down in Q4 by $3k (which could still be considered "relatively flat" IMO), than that would be $21m (about 7000 cars x $3k each). And we'd only need to find $10m more in revenue from other sources.�

Feb 18, 2014

vgrinshpun Looks like MB has a bit of an issue with mentioning that the power train is supplied by Tesla. Did I miss it, or they just feel a bit insecure?�

Feb 18, 2014

austinEV AustinEV Q4 ER Megapost

1. Long term TM outlook

?2. General market background

3. Specific Q4 earnings content guesses and ramifications

4. Differences from Q3.

5. Bear case, such as it is

6. Investment setup

?

1) Long term outlook:

I have never been more bullish on the long term outlook.

If you haven't watched it, check out this lengthy video of a talk given by Marc Tarpenning posted by TD1 here. Skip to 52:00 to see him comment on why the big automakers will not be threatening Tesla any time soon. Yes, TSLA has 1/2 of the market cap as GM, but this makes me think that GM is hugely overvalued.

He says in that video, that most of the functions of GM (or other large auto makers) has been subcontracted out, including the electronics. They essentially kept the engine part in house because that is "where the value is", in making good engines that run for 100k miles for not a lot of money, and the electronics and even some of the design and manufacturing is done by subcontractors. Maybe you all knew this already, but wow, they are in a terrible position to pivot and change in a major way.

He basically insinuates that 20 years ago you couldn't have started a new car company at all, because all of that subcontractor space didn't exist and now it does so they can leverage it. So basically, a brash silicon valley team could have probably succeeded in just making a good car of any sort (ICE) with a small in-house team, lots of vertical integration, top in-house design capability and a direct sales model. Whereas GM would be incapable of much more than making last year's car an inch longer.

That Tesla-as-a-new-ICE-car-maker thought experiment is valuable. That company alone would be quite exciting. Strong team, strong CEO, vertical integration, cheap factories, local tax incentives, market ripe for a new entry for a US made car. I would probably be investing like crazy in that company. Now add on the fact that they make better cars than anyone in the world, and have a multi-year plan to expand like crazy and a plausible explanation for being demand constrained for many years.

Now add in the new innovative drive train. Simple, with a low cost and a path to become very low cost. Ultimately the EV drive train should be much less than ICE which is fully cost-reduced after 100 years.

2) General market background:

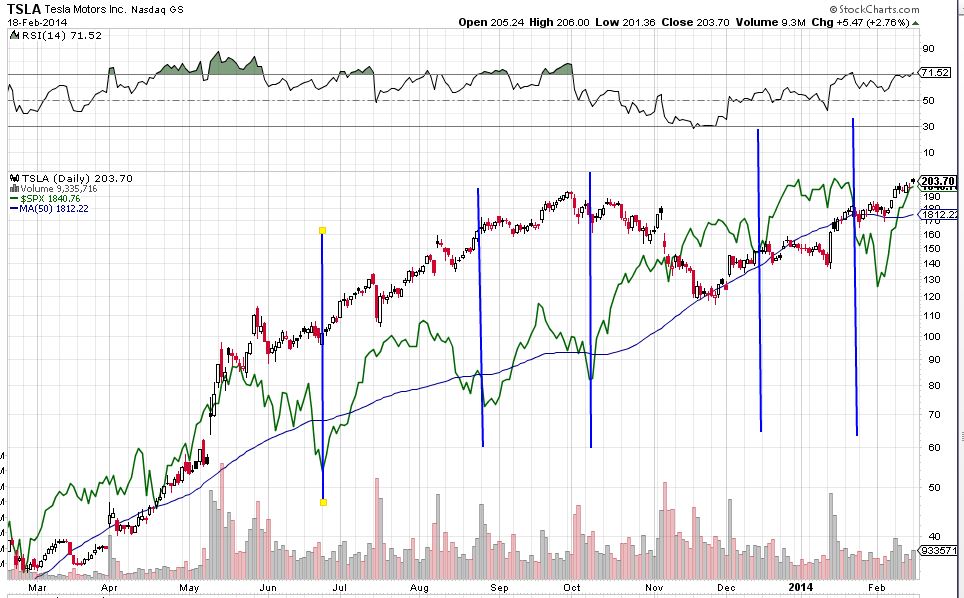

It is a fortunate time in the general market, with Congress coming to their senses and the general market indexes on a roll. The last year has shown some periodicity of the SPY hitting or threatening the 50 day MA, but we just came out of our latest freak-out, strongly rebounded and we are not due for another for a few weeks, giving us a tailwind:

(SPX in green, blue lines are my market downturns)

3) Specific Q4 earnings guesses:

I am not a leading prognosticator on numbers, and I don't have an entrant into the guessing game. In this case I don't think the numbers will matter that much, other than the 6900 cars which has already mattered. Generally companies who pre-announce good news have other good news in their pocket. That seems reasonable, given that there are many such potential sources of good news and I would suggest relatively few things that could be lurking as bad news.

Potential Good News Menu:

- China reservations or uptake at a high rate. High reservation reserves of cash.

- China government incentives/anything.

- Improving Gross margin, at least over 25%. Guidance to 30% in 2014 possible, if they choose to say it.

- NHTSA clearance, probably not going to come out this week and probably 2/3 priced in.

- 2014 full year guidance. They should guide, and they should guide to 35k. I think 40k would be a headline and very positive.

- The Elon factor: For Q3 he practically warned us when he made bearish comments about the stock. For Q4 he is more upbeat and we have no such warning.

- Factory capacity plans: I and the market will be disappointed if they are silent on this again. I like Bonnie's theory that they ALMOST talked about it last time so they have had a whole quarter to get the details right. The uncertainty itself is the negative. If they do announce, I will be watching to see if it is not dilutive or if it is dilutive in a smart way. A clear path with partners will be a very bullish factor because it will clear a lot of fog on the path to mass production of the Model E. Without it, the fog remains and that is bad.

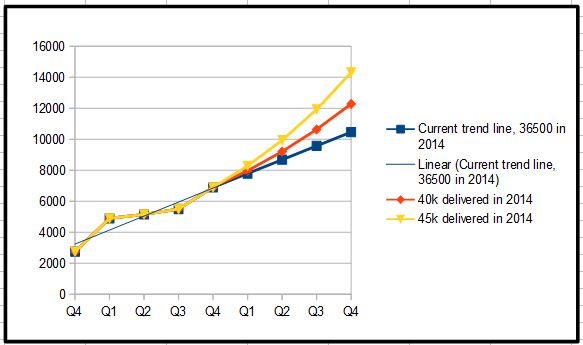

- Supply chain improvement: This one will be my favorite. I will be looking for comments about supply chain constraints easing up, which in the really fun best case scenario could mean they are increasing production in a meaningful way and have a path to more than 35k and they will provide more guidance in the next earnings release or something like that. I like to think they have supply worked out well except for batteries, so output can go up in non linear ways, getting off this trend. Here you see how just a modest acceleration this is:

- ZEV credits: We all forget this one, since TM has guided to ignore it for Q4. So this is all upside. This is an easy way to get surprise into the profits/eps.

- Supercharger update: High install rate and 135kW. Battery swap station (maybe the market will think that is cool)

- Autopilot features plan? That was a heck of a hint. Another headline possibility.

4) Differences from Q3.

Many of us got burned just trusting last time would be ok. In hindsight that was more of a faith move on my part than was warranted. Elon practically told us to take that one off. But, I think there are significant differences between the poorly received 2013 Q3 ER and now. For one, we had just had 2 positive reactions in a row. Honestly I was always a bit puzzled by the positive reaction to the Q2 announcement. It felt like TSLA just had positive momentum so a good report was enough to make it go higher the next day.

For Q3, the momentum was going sharply the other way. We were mid f*re freakout and technically the market was looking for an excuse to push it down. When a good report came out, the fact that it wasn't bristling with extra goodies was enough for the market to push it down, continuing a technical correction. Q3 needed to be so good it broke the back of a strong downward trend.

For Q4 (now) the situation is reversed. The technicals are on an uptrend and the market is looking for a reason to push it up. We just (apparently) survived our first f*re FUD alarm with a shrug, a very bullish sign. Plus, there are good reasons to suspect the Q4 ER will be bristling with goodies, where the Q3 was not. Some of that is priced in, yes, but not all in my humble opinion. I think the market is looking for a reason to push it up to a new ATH, I have a target of 220 for this week and I think it will have support at that level. Sleepy's 280 would be ok too...

I don't think this is irrational exactly, the company is now humming along better than the last ER.

5) Bear case, such as it is:

- "Valuation is just too high. Half of GM!� If you are stuck in valuing it compared to a slow growing old guard company you will just never understand. If you understand/believe in the long term growth story the PE ratio is justified.

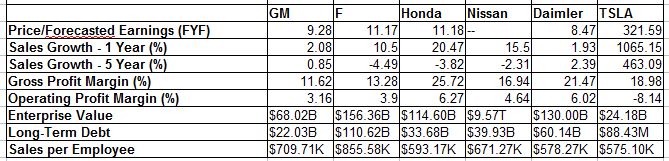

Here are some numbers I pulled from Schwab's research tools. Yes, the forward PE is 321. Yes the market cap is 24B. But note the high (and rapidly increasing) gross margins, sky high growth rate, competitive sales per employee and virtually no debt. GM has 22B of debt and Ford 110B.

?

I am not sure why it is showing Nissan with a 9Trillion dollar market cap... ignore that.

- Execution risk: "A lot of perfection is priced in. Therefore one hiccup and the stock will plummet." That is fairly true and we saw it play out after the f*re debacle. But this switches to a positive now because we all know how that looks now having seen it and seen it recover. This was a lot scarier back in early Oct2013 when the stock had essentially never gone down before. Also, new f*re headlines seem to have little risk now as we saw with the Toronto incident. That hasn't played out yet totally, but the fact that the release itself was harmless is a bullish sign.

- Competition risk: "The other automakers can get in the game and make Tesla killers and halve the potential market for Tesla or undercut them completely with a better product. Everyone would prefer to buy a BMW EV if they could, so Tesla is on thin ice." They won't want to invest to obsolete their core competency so they might be culturally incapable. Also these investments will just cause confusion in their own lineup since they can either make a poor EV that no one will buy and therefore be a waste of money, or they will really pull together and make a car almost as good as a Model S (ignoring the barriers of patents, battery supply, software, charging network, etc) and would be in the position of having a car that was better than their other cars so there is no good way to sell it without admitting that the 99% of their other cars is inferior or trying not to sell the good EV. They see this end so there is little reason to invest. If one accepts that EV platforms are superior, and one sees that most or all of the car makers are in this position, then you now see how the valuation is not worrisome. For Tesla to justify even their current valuation, they essentially have to be on a path to become one of the largest automakers in the world, and indeed largest companies in the world. That seems insane to the casual critic on TV, but in this context you see that in 10 years the other automakers will be going bankrupt one by one and making desperate plans to reinvent themselves as EV companies, far too late to be a serious threat. THEY will be the small upstarts trying to gain market share, not Tesla. Furthermore, EM has said multiple times he is not afraid of competition, since a vibrant market place would be a rising tide lifting all boats. Other serious entrants would rapidly accelerate acceptance in the marketplace and Tesla would benefit for being the first mover. Telsa could also benefit from becoming the licensor of Supercharging capacity for competitors or even drive train patents. There are more paths for TM to become the largest automaker in the world, than there are paths to settling in Porsche territory, as critics like to place them. Also there are no good pure EV's yet. The BMW i3 is being advertised on the Olympics and is lackluster by all accounts

6) Investment setup:

I have a fair amount of shares, 15 Jan '16 leaps that I have as a "core" position. I got these in Dec when it was testing lows and I wasn't sure of the timeframe of the inevitable recovery. Since then I have gotten many Feb 22 DITM calls and a few 190's. I have some more cash on the sideline that I will look to deploy on a dip.

With all of this going on, I haven't been more sure of an upside after earnings since the Q1 '13 report that we all love so much. I am seriously questioning why I am not putting the couch cushion change into Feb 22 200's. I am calling for a target of 220 post earnings which is only 8% from Tuesdays close.

The big risk of course is that all or much of this is priced in already, and the report will just trigger a sell-the-news drop commonly seen with other momentum stocks. This is my biggest fear for this week, but I do not think it will happen for these reasons:

[*=1]While it is true that the stock is up sharply in the last few weeks, I see that as a recovery from the f*re overreaction, not growth.

[*=1]Technically the market is in an upswing and wants to push it higher. The 195 previous ATH is now support and have confirmed upward momentum to ATH's. One could argue that even without an earnings release this week the stock is poised for a breakout on technical terms alone. Contrast this with Q3 when the stock was in a confirmed downtrend, and the report would have to be so good it reversed that trend. Q3 was merely "good". Workmanlike. Solid. Good job. But, nothing fancy and the market sold it off due to continuing softness and risk in the unfolding f*re story.

[*=1]We on TMC have proven again and again that just because we TMC nerds know stuff that doesn't mean the market does. With the long list of things I expect to be positive bullet points in the announcement, along with loads of potential great news bullets, I think the announcement will be immediately perceived as positive and that will be the narrative.

[*=1]Lots of shorts have been attracted to the ATH. It went down from 195, why not 203? If you think that the half-of-GM market share is silly then it is a very attractive short, but they will be weak shorts indeed.

[*=1]If Tesla pops, a lot of sideline people may capitulate, buy in at $220 and hate it, figuring that it simply won't be cheaper in the future and it is time to bandwagon a bit. There is a big risk of weak longs who will head for the exit at $220+, but they will be matched by shorts heading for the exit and other technical traders looking to take advantage of a technical rise. If that plays out prices above $220 are not crazy talk.

Headlines from the future, internet writers feel free to use:

TSLA up 8% on China reservation strength

TSLA surges to new ATH on higher guidance

TSLA higher after announcing battery factory deal�

Feb 18, 2014

vgrinshpun Then we can assign equal probability to ASPs being 3K more (majority of North European customers buying additional set of winter wheel/tires from Tesla for instance), and then $31M will become $51M... As a matter of interpretation I believe we should analyze the middle number, not the extremes. Ultimately, though, I tend to agree that there is no 100% clarity here, and that is what makes it so similar with the situation before the Q1, when nobody guessed how they can be both GAAP and non-GAAP profitable based on the information revealed at that time. As you no doubt remember, the additional revenue was in what at that time TM called "regulatory credits".�

Feb 18, 2014

Bgarret I'm with Vgrinshpun on this one...I believe ZEV is alive and well based on the changeover in the program year in October, Tesla's front loaded ZEV revenue in Q4 2012 & Q1 & Q2 2013, the increase in requirements for 2013/14 & exponential increase set for 2014/15, the 276 credits carried over from last year amounting to approx. $42 million in potential revenue and Tesla's guidance to 20+% increase in revenues. Here are my numbers for Q4 2013....good luck and cheers.

Cars Rev/Car Gross Margin ZEV Credits Revenue Gross Profit Expenses EPS 6,800.00 98,000.00 0.26 65,000,000.00 731,400,000.00 238,264,000.00 138,000,000.00 0.72 Non-GAAP 6,800.00 72,000.00 0.26 65,000,000.00 554,600,000.00 192,296,000.00 162,260,000.00 0.25 GAAP �

Feb 18, 2014

callnaveen Wawww... good detailed explanation Austin. Keep up the good work.

I hope things will be good tomorrow as everyone expecting. I lost lot of money in the last quarter, hopefully I should get that back with this ER.�

Feb 18, 2014

kenliles @austinEV - fantastic post. Thanks for all the detail; extremely helpful�

Feb 19, 2014

Chickenlittle Are we forgetting battery backups for solar city. Have seen a picture of one. Are they selling those already or prototype?�

Feb 19, 2014

blakegallagher Yea I noticed that too. In fact they almost denied it lol.

"It's a fresh, fully connected approach to driving that's equal parts responsibility and exhilaration � and every part Mercedes-Benz." (except what makes the car move :wink�

Feb 19, 2014

JRP3 Maybe Merc considers themselves part owners of Tesla so it's all "in house" :wink:�

Feb 19, 2014

vgrinshpun They might need to buy few more shares to lend some token credibility for such a claim. I can sell them some for $500 or so...:biggrin:�

Feb 19, 2014

ItsNotAboutTheMoney Low volume, I'd say. Robert(.Boston) has pointed out that there's not that much value in grid management and arbitrage, and relatively speaking lithium batteries are an expensive back-up, so I'd look at it as a grant-sucker for now. The long-term value comes with the gigafactory (=high volume, low cost), as a future product and as part of the gigafactory plan (back-up storage using degraded batteries as part of maximizing value in the manufacturing loop.)�

Feb 19, 2014

chickensevil If I am not mistaken Nissan is being rated in their local currency their (yen)... according to yahoo, NSANY which is their US stock symbol, is rated at 76.74B�

Feb 19, 2014

callmesam I tried to create a blog post, but it wasn't an ideal fit since it won't let me comment and I'd have to revise the blog post, delaying access.

I did create a forum post:

Fourth Quarter 2013 Financial Results QA Conference Call - LIVE BLOG�

Feb 19, 2014

DaveT My initial Q4 shareholder letter thoughts:

- strong FY2014 guidance at 35k and 28% gross margin in Q4 2014

- super strong revenue numbers at $761m

- reached 25% gross margin target for Q4

- production target/guidance given for 1000 cars/week by end of year

- Gigafactory to deliver "massive volume" of stationary storage for solar industry

Neutral:

- expenses higher than expected but doesn't matter since revenue was so strong

- Q1 guidance for cars delivered is 6400

Negative:

- it appears Model X is delayed somewhat as design prototypes on road by end of year and no mention of customer deliveries by end of year

Overall, it looks very good.�

Feb 19, 2014

Johan Produced. But of those 1000 will be in transit so 6400 delivered.�

Feb 19, 2014

sleepyhead 7400 produced, but 6400 delivered. 1000 additional units in transit.�

Feb 19, 2014

pz1975 Model X will be available in Canada Q2 2015 as per the email I received from Tesla (I Have a reservation). I assume it would a similar time (or maybe sooner) in the US.�

Feb 19, 2014

Noble Ninja Man, we're up to 220 in AH and the ER conference hasn't even started yet !! I regret missing the chance to buy more at $165 recently!�

Feb 19, 2014

Matthias Buhl From the Report:

"Very shortly, we will be ready to share more information about the Tesla Gigafactory."

Do you think "very shortly" could be during the conference call, or is this too shortly?�

Feb 19, 2014

FredTMC nice summary Dave

congrats to all the long term investors!�

Feb 19, 2014

carrerascott $117 wasn't long ago either!�

Feb 19, 2014

tslas For that, It needs to go to 295�

Feb 19, 2014

Mario Kadastik And I think as this is I think the first time TSLA reports produced it's precisely to show incremental increase. And there are other nice nuggets hidden in the report like showing that the Beijing store is highest traffic store ever (likely translates to record reservations) and for example customer deposits went from $138.8M a year ago to $163.1M even though Tesla delivered 22.5k cars. That shows the amount of demand that is HUGE.�

Feb 19, 2014

DJ Frustration Looks like the email was accurate from the shareholder letter details.�

Feb 19, 2014

brianstorms I don't treat the Model X "delay" as news. It was hinted at, if not more explicitly stated, in recent public statements Elon or somebody made.

I also think the delay is strategic, to maximize Model S sales and profits.

Then again, could be wrong, maybe they've discovered the falcon-wing doors aren't as bright an idea as they hoped.�

Feb 19, 2014

RationalOptimist what time is the call?�

Feb 19, 2014

carrerascott 5:30et�

Feb 19, 2014

rdalcanto Did i miss it in the report? I didn't see anything on expected EV credits for 2014. Those will help earnings in the first half of the year, correct?�

Feb 19, 2014

DaveT From Q2 2013 Shareholder letter:

"If demonstrated demand in North America and Europe is matched by similar demand in Asia, annualized sales for Model S could exceed 40,000 units per year by late 2014."

From Q4 2013 Shareholder letter:

"The potential in Europe and Asia is even more significant. Towards the end of the year, we expect sales in those regions combined to be almost twice that of North America."

Q2 mentioned "if". Q4 mentions "we expect".

Tesla appears to be growing more confident on demand from Europe and Asia.

I hope an analyst asks about this so Elon can expand during the conference call.�

Feb 19, 2014

pGo Anybody has the conference number handy? Congrats to all long holders.�

Feb 19, 2014

FredTMC Someone said earlier that the webcast works okay even for iOS. I'm on it right now and listening to the nice elevator music. I think it'll be fine.�

Feb 19, 2014

pz1975 "Q4 non-GAAP net income was $46 million, or $0.33 pershare, while Q4 GAAP net loss was $16 million or $(0.13)per share. Both results include a $4.6 million net gain, or$0.03 per share from a favorable foreign currency impact. "

Note the last sentence - I remember discussion on here previously about the USD exchange rate with other currencies and how that would affect revenue/EPS. We can use the numbers given here as a reference for future earnings reports to adjust the numbers for the USD going up or down.�

Feb 19, 2014

mulder1231 Yes, because didn't they also reduce the deposit amount?�

Feb 19, 2014

Mario Kadastik It's �2000 for Model S and �4000 for Model X. Signature is �40k. That should translate approximately to 2.5k, 5k and 50k$. So assuming max Sig X amount is 2000 (all for EU, US) that's 100M, the rest 60k I'd give a mix of 1:1 for S:X so 30M for 2.5k Model S i.e. 12k cars reserved and 30M for X which is 6k reserved. Hmm... I guess the Sig count is lower and the S and X numbers are respectively higher so more likely 60M for sigs and 100M for rest giving a nice full 2014 already pre-reserved?�

Feb 19, 2014

sub thanks to everyone here for all the work you do. I was considering hedging but after reading everyone's projections I went in naked and i'm happy I did so. Looking forward to the conference call, I think Elon is going to mention at least a little info on the Giga Factory.�

Feb 19, 2014

Causalien Dave, what caused the discrepancy in net income (gaap and non gaap) between yours and the actual result?

*Edit: NM. DaveT was actually pretty spot on.�

Feb 19, 2014

CapitalistOppressor Capital raise incoming. Surprising no one.�

Feb 19, 2014

AlMc Nice to see you again. don't be a stranger!�

Feb 19, 2014

CapitalistOppressor I've been too busy with other projects to run the numbers, but if I recall, my old models showed that 2014 should be slightly less ZEV revenue than in 2013, followed by a probable increase in 2015. But forward looking projections into that market are pretty hard. It really depends on how the other automakers do in meeting the requirements.�

Feb 19, 2014

sleepyhead Selling the Model X is like "going fishing and the fish are jumping in the boat"

Nice!�

Feb 19, 2014

CapitalistOppressor Also, Tesla will consistently downplay the possibility and effects of ZEV revenue. They've been trying to fake out the press into thinking ZEV goes away by focusing on how it goes away in Q4.�

Feb 19, 2014

pz1975 Agree - brilliant quote!�

Feb 19, 2014

Clprenz Another Line is being built

!�

Feb 19, 2014

CapitalistOppressor Thanks

It's hard to keep super plugged in all the time. The company is doing very well, and not doing anything unexpected if anyone was following these forums in 2012 and 2013 (and presumably earlier).

So the marginal value of my contribution is quite low, and the marginal value of long delayed vacations to exotic locales is concurrently higher at this point.�

Feb 19, 2014

sleepyhead Congrats!�

Feb 19, 2014

callmesam THIS! +100. By focusing on diminishing ZEV credits going into Q4 . Implying they're gone. Saying "we don't count on the revenue" etc, they are building a beat-down into Q1.

Classic.�

Feb 19, 2014

DaveT Here�s the major differences between my estimate and actual (the shareholder letter had a few minor numbers that I couldn�t reconcile but generally it�s fine for illustration purposes).

Basically I underestimated ASP significantly and total revenue but that was balanced by Tesla having higher expenses that I anticipated, namely higher cost of development services, higher SGA, and higher stock compensation. This led to non-GAAP income to be similar to what I was forecasting ($0.32 vs $0.33) but GAAP income to be slightly different (-$0.05 vs -$0.13). I was correct that GAAP profitability would be difficult to achieve without significant ZEV income.

Overall, the results are better than I expected because revenue was super strong as well as ASP.

�

�

Feb 19, 2014

austinEV It is hard to buy a Model S for 100k, strange as it is to say that. Once you have decided to go to 100k, the last 5-7k in options seem real minor and you sell yourself on the pano, or the fancy paint, or the leather, or the...�

Feb 19, 2014

Zythryn Dave, I am curious, is that average sale price stated by Tesla, or calculated in some way?

That seems very high to me. I see more 60s in our state than P+s.�

Feb 19, 2014

FANGO In Southern California I see nothing but p85s.�

Feb 19, 2014

DaveT I calculated the average sale price by taking the vehicle sales number and dividing by number cars delivered. I probably should have added GHG/Cafe income to the vehicle sale number so the ASP should be higher (which is mind-boggling because it's already so high).

The shareholder letter had development services at 4.368m and mentioned 15m in regulatory credit income (not ZEV), zero ZEV, and mentioned they received 13m from Daimler and Toyota (which I added to power train sales, which do not go into ASP).

I'm kind of scratching my head on how ASP can be so high but it could be Europe shipped mostly loaded cars and P/P+ demand was really high as well in US and Europe. If anyone has any insight on this, please let us know.�

Feb 19, 2014

brianstorms I'm in SoCal and I have a standard 85. So there's at least one�

Feb 19, 2014

Cobos I've got one of the few S60s in Norway. And I still haven't seen one other S60 so I'm guessing I could use my fingers to count S60 sales (at least if I'm allowed to use toes as well). Every car is at least a S85 with decent amount of equipment and I'd say about half are P85 and P85+, that's out of almost 1500 sales in Norway in Q4. That might be some of the reasons the ASP has been pulled up.

Cobos�

Feb 20, 2014

Discoducky nice, missed that, no issues with demand!�

Feb 20, 2014

sleepyhead Even though customer deposits went up from $138.8m to $163.1m Yoy, that is only peanuts. I expect that number to be a lot bigger in the Q1 balance sheet. $20m is equivalent to 500 reservations in China. Since we know that demand started soaring there after the fair pricing announcement (which only happened in January 2014), it should show up in the Q1 balance sheet.

1000 Chinese reservations = $40m�

Feb 20, 2014

chickensevil I mean, when I bought my car, I didn't want to really spend more than I had to... I am not "rich" or "loaded" by ANY stretch of the word, yet even I couldn't resist getting options to the point where I spent 96k... and I ONLY got a regular 85. I think JUST adding the performance package is another 13k, so if I had done that I would be hitting well over that ASP without even trying.�

Feb 20, 2014

VolkerP I have one of just 5 S-60 in Germany, total for 2013 was 191 vehicles. So most were 85kWh which started at 81.650� including VAT and import duty.

I guess that initial pricing for oversea deliveries was calculated with a cautionary buffer for exchange rate changes, since prices were announced months before finalize & deliveries. Tesla seems to have erred on the safe side. Recently they reduced prices due to "exchange rates / weaker US dollar". Reservation holders report that prices of their cars (if reordered) would be like �5.500 less or even CHF 11.000 less.

So I think Tesla achieved excellent US$ revenue on all cars delivered to Europe in Q4.�

Feb 20, 2014

chickensevil Which explains the comment about how they had favorable exchange rates that contributed to their profits. While I don't think they should price gouge foreign countries I don't take major issue with them placing a "safety" buffer there if the exchange rates go sour, and then updating the price every 6 months or so. Because otherwise it has the potential to eat into their actual profits on the car itself.�

Feb 20, 2014

AudubonB

I just went through TMInc's Order--->Reservation page, trying to corroborate your $40K reservation statement. The interesting thing is that you can get from its pop-down menu "Price based on delivery to..." effectively every country on earth...exceptfor China! As here: Buy or Reserve a Tesla | Tesla Motors And $5K is the downpayment everywhere. So why did they up the ante so much for China?�

Feb 20, 2014

772 $40k is no longer necessary in China for Model S... only 15k CNY: MODEL S 设计室 | Tesla(特斯拉)Motors

And for Model X it's 30k CNY�

Feb 20, 2014

Benz There is something from the shareholder letter that I want to discuss here with you guys:

"For the year, Model S was the top selling vehicle in North America among comparably priced cars. Nonetheless,we believe there is room to improve in 2014 as we complete the Supercharger network and enable vehicle

service almost anywhere in North America. The potential in Europe and Asia is even more significant. Towards

the end of the year, we expect sales in those regions combined to be almost twice that of North America."

OK, let's break it down:

- "Model S was the top selling vehicle in North America"

- "we believe there is room to improve in 2014"

What does that mean?

I think that it means that they will sell more Model S vehicles in 2014 (at least about 20,000?) than that they did in 2013 (about 18,000?).

- "The potential in Europe and Asia is even more significant. Towards the end of the year, we expect sales in those regions combined to be almost twice that of North America."

I think that this says more about the situation in 2015. Europe and Asia combined will be almost twice that of North America. Suppose that North America is 25,000 in 2015, then Europe and Asia combined will be almost 50,000. Meaning that the total will be almost 75,000. Right?�

Feb 20, 2014

AlMc Benz, That is how read it.�

Feb 20, 2014

Benz "We expect to deliver over 35,000 Model S vehicles in 2014"

That will be purely because they expect not to be able to produce more, meaning that they will be production contstrained?

Because I think that the number of new reservations for the Tesla Model S in 2014 will be somewhere close to 50,000 (at least).

But they know that too, don't they?

This means that the waiting time for a Tesla Model S will rise significantly in 2015, right?�

Feb 20, 2014

Krugerrand No, because by 2015 they'll have their factory upgrades online.�

Không có nhận xét nào:

Đăng nhận xét