Nov 4, 2013

sleepyhead Please click on the link below to find my Q3 earnings preview and to download my Excel model. I appreciate everyone's hard work here on TMC; without it I would not be able to put together such a comprehensive preview:

tcinvestor

Highlights:

Q3:

5,700 cars delivered,

$633 million in revenue

$0.34 EPS

22% gross margin excl. ZEV

I will stop by later to discuss my article; we will keep the discussion here on TMC. I am on vacation now and I am going to the beach to relax and enjoy the solar rally that is going on today and over the past year.

Cheers,

sleepyhead

- - - Updated - - -

Please do your own due diligence before investing. I have done mine and taken some TSLA positions today accordingly.�

Nov 4, 2013

Thread Summary Index of sleepyhead's articlts

This wiki-post is to track sleepyhead's articles via hyperlinks to other so-called "megaposts":

Q3 Earnings Preview - 11/4/2013�

Nov 4, 2013

farzyness Thanks Sleepy.

FYI that Solar pun was a thing of beauty.�

Nov 4, 2013

Objective1 @sleepyhead:

You have "23.4% gross margin including all credit sales" for FY13. That's impossible.

Q1 and Q2 margins were far below the 23% level. For Q3 and Q4 to bring the annual average margin up to 23%, they would have to feature margin of over 30% (ballpark figures).

In any case, it was clear in the Q2 earning call that the goal was to achieve 25% margin in Q4, not to realize FY13 25% margin overall by Q4 end.�

Nov 4, 2013

sleepyhead 23.4% gross margin for FY13 includes ZEV credits. There is no error in my estimates in this case.�

Nov 4, 2013

MikeC Thank you once again, sleepy.�

Nov 4, 2013

hershey101 Hey Sleepy, the formatting of the page is screwed up (at least on Chrome).

I know the site was having issues with certain browsers before, I just wanted to let you know so you can fix it if you have access to the web server.�

Nov 4, 2013

Mario Kadastik At least on Safari it looked fine") �

�

Nov 4, 2013

sleepyhead Thanks for the heads up. I never had issues on my Nexus 10 before. We will look into it.

In the mean time what do you all think about my estimates?

I think that eps of 0.30 is a good starting point and it can go +/- 0.10 in either direction.�

Nov 4, 2013

marvinat0rz Thanks for your comprehensive model and contributions�

Nov 4, 2013

MikeC Looks fine to me on Chrome.�

Nov 4, 2013

aznt1217 I think it's a very fair estimate. Not too far off from Wall St. Whisper numbers. The big question is the ZEV credits (because nobody knows the distribution of the Euro cars) and how much the price increases helped on the % margin. Thanks for pulling together the in depth analysis. I've been wanting to do this but other obligations have been keeping me. The range also seems very fair as well-- depending on the amount of deliveries.�

Nov 4, 2013

Sunnyday Thanks, Sleepy. Great stuff. Three questions.

1. Your models are forecasting significantly higher EPS than the highest consensus estimates, per your notes at tcinvestor . Based on past quarterly beats by TSLA, if the Q3 numbers come in near your numbers, what would that mean for analyst consensus estimates for 2014 and 2015?

2. In the Stanford video, I think Elon was quoted as being inclined to keep lid on short term earnings growth in favor of increased investment. If EPS comes in where you forecast, might Tesla be inclined to ramp up investments to bring that down in coming quarters?

3. What impact from the fires, if any, are you forecasting for Q4?

thanks again.�

Nov 4, 2013

c041v Thanks for the post Sleepyhead.

I'm wondering how much of the increase in R&D will come from Gen III? There's got to be a few teams of engineers working on it now, and I would think with the big cash stockpile raised from the secondary that their may be less resistance to be extremely conservative in getting Gen III going as long as they don't make it look like they are vaporizing cash. Just my thoughts.�

Nov 4, 2013

hershey101 I came up with ~0.21 with slightly lower production rate and lower ASP... I think I was being a bit too conservative though.

The absolute bottom I see is $0.17. I don't see any way they could have a lower number than that... That being said, in order for us to see ATH or anything that can be considered a good move on the upside, I think we need an EPS of $0.25 with increasing this years guidance and next year's guidance.

I think that they are definitely going to increase this year's guidance to about 21,500 cars and then actually end up delivering around 22,200... The bigger boost would be from increased GM ex zev. credits. But I think they will maintain this at 25% and end up doing 27%+ for next quarter.

I'm looking for a 41K guidance for FY14. I think this is reasonable to expect, and that leaves them plenty of room to increase guidance as the year goes on. In reality I expect them to deliver 50K+ next year. This is going to be the big one. Anything that shows less than 100% YoY growth will not be looked upon well by the street and this will be the make or break for the quarter.

Lets hope some of the smarter analysts read this forums and figure out the correct questions to ask during the Q&A.�

Nov 4, 2013

brianstorms Formatting's messed up on Firefox as well. One paragraph plotting on top of another.

Quick screen grab snippet:

�

�

Nov 4, 2013

hershey101 Okay then it might just be me... Chrome tends to act weird on Linux with SSDs... It looks fine for me on Firefox but on Chrome the GM and Supply constraint paragraphs are on top of each other...

Looks like brainstorms beat me to it

I'm seeing the same thing on Chrome, but its fine on Firefox...

Are you on a Linux distro. brainstroms?�

Nov 4, 2013

sleepyhead 1. Please find my Q2 ER preview hear on TMC. In it you will find ridiculously low FY13 EPS estimates compared to now.

2. Elon said that 2015 will be the year for high EPS. I take this as give or take $10 EPS in 2015 and a few bucks in 2014.

3. I can't see fires having big financial impact on Tesla. Maybe only on TSLA.�

Nov 4, 2013

Borris thank you, this should be fixed now�

Nov 4, 2013

hershey101 Yep... Awesome thanks�

Nov 4, 2013

Citizen-T I saw this on my Nexus 7 as well.�

Nov 4, 2013

sleepyhead The R&D increase will come from Model X and Model S improvements; Gen3 will not have any material impact for a while.�

Nov 4, 2013

ModelS8794 Sleepy, is your $101k ASP pure car, or does it include either of GHG and/or ZEV credit revenue?

I think low ASP is what's got the street most off base this qtr, but I have a hard time getting to $101k ex-all credits.

Street is at $3.1 billion sales in 2014 - i dunno if that's GAAP or lease adjusted, but if it is the latter then I think it's off by about 50%. I dunno if this quarter will be the time or not, but getting 45k+ units and 99k+ ASPs into consensus is IMO what will have the most impact on TSLA over the next year.�

Nov 4, 2013

FredTMC Thanks for the post sleepy. I've had trouble sleeping last few days. ER anticipation. It certainly won't be boring. Nice to see TSLA pop back to $170 today.�

Nov 4, 2013

ibcs Thanks Sleepyhead,

Always look forward to your thoughts going into earnings report. Seems like others are agreeing that Tesla will surpass estimates.

Go Tesla!�

Nov 4, 2013

sleepyhead $101.5k is pure auto. I think the risk might be to the upside though, since Elon said they factored in a 3% price increase for international sales for forex movements. Since the USD weakened in Q3, this will provide an even bigger boost.

Remember no more 40 kWh sales in Q3, lower mix of 60s. Full quarter of P+ sales. Signature deliveries in EU, and a couple of weeks of higher options pricing for Model S orders.

So I think that the risk is definitely to the upside.�

Nov 4, 2013

Mario Kadastik With regard to the fire Elon mentioned in the german interview (it was really a huge source of intel) that initially when the fire happened they saw a slowdown of orders, but when they posted the explanation to what had happened they actually regained those very fast and continued at a higher order pace. People loved the fact that it's such a safe car. So this is to answer about the Q4 impact from fires.�

Nov 4, 2013

sleepyhead In regards to 2nd fire:

There is suspicion that the driver was drunk and speeding. Crashed into a wall and catapulted into a tree, but the driver managed to walk out of the car without any hints of the slightest injury.

Sounds like a pretty safe car to me.

After these two fire incidents, I am considering buying a Model X for my wife and kids for the sole reason to protect them in case of an accident.�

Nov 4, 2013

tslafan123 And the guy was begging for faster delivery of his next Model S. Sounds like he just can't tolerate driving any other car anymore..

Musk said in an interview in Germany that sales went down after the first fire, but they went up after the blog post - higher than previous high. Looks like people are pretty convinced that it is a very safe car.�

Nov 4, 2013

sleepyhead One thing that has gone completely unnoticed is that Tesla said in Q2 shareholder letter that EPS will be positive excl. ZEV.

Since It looks like they will beat delivery guidance by 10%, there is a floor of $0.10 EPS. Each $10 million of ZEV should raise EPS by another $0.07.

I think it is safe to say that TSLA will beat non-GAAP EPS consensus by a good amount.�

Nov 4, 2013

ModelS8794 There were on the order of 500 or 750 40kwh produced right? So maybe that adds $5-8 million over 5150 cars = 1-1.5k to the $93 ASP for an adj. Q2 base of $94k. off the 94k base, shall we assume 25% of production headed to Europe this quarter? 500 European Sigs at, what, $120k? and 900 more at $103k sound good?

That would leave 3600 US sales. To get a $101.5k ASP you'd need those cars selling at $99k, a 5-5.5% increase from the Q2 adj. ASP. I guess that's doable if the P85+ is a huge hit; I don't really recall the timing of the introduction nor have a good sense for how much uptake it got.

Best get your reservation in now. Better yet, you'll want to have the fam driving safe ASAP, so a Sig reservation seems most appropriate. This recommendation has nothing to do with my desire to see Tesla's balance sheet look as good as possible. :tongue:�

Nov 4, 2013

ElectricFarmBoy Absolutely agree. I think we're now into a 4th category of Tesla buyers (after treehuggers and performance freaks and early adopter techies) -- that being those that years ago would have bought a Volvo for its safety. Just looking at all the crash pics in this forum and how well the car survives puts me into the same mindset as Sleepyhead as well...and I think long term this is an extremely important selling feature.�

Nov 4, 2013

kenliles I think that second-fire driver, redefined himself as a tree-hugger category�

Nov 4, 2013

Lessmog Perhaps in a roundabout way ... ;-)�

Nov 4, 2013

austinEV These puns strike me as quite wooden.�

Nov 4, 2013

Lessmog Funny, I thought it was concrete. :-D

(Sorry)�

Nov 4, 2013

Convert2013 Elon too had trouble sleeping working hard to make us TSLA investors happy.�

Nov 4, 2013

DaveT First, excellent article. Thanks for writing it up, referring back to Q2 shareholder letter and for posting the excel docs.

Just curious do you remember when/where you heard Elon saying 2015 will be the year for high EPS?�

Nov 4, 2013

StapleGun ~735 40kWh cars were delivered, basically all in Q2. The average 40kWh car probably had an ASP of around $65-70k ($57.4k base and most likely much less equipped than the average car). These 735 cars from Q2 are being replaced by US deliveries with an average ASP of around $95-100k, so we're looking at about $30k*735 difference or about $22 million net difference.

Your EU numbers (1400) look about right, but there's no difference in signature/non-signature pricing. The key is standard v. performance v. performance plus. My EU data about configurations comes from this spreadsheet. Compiling that data gives me these approximations...

* These are pretty much guesses, so change the numbers to suit your liking if you disagree. Also note most early EU reservations were under the original pricing scheme.

Config Percentage Est. ASP*

P85+ 25.5% $118,000

P85 38% $107,000

85 34% $96,000

60 3.5% $84,000

This gives a total EU ASP of $106,330.

The number of US deliveries doesn't have a huge effect on ASP in these calculations so lets guess 4300. So to get to sleepy's ASP we would need a $99.9k ASP for US deliveries.

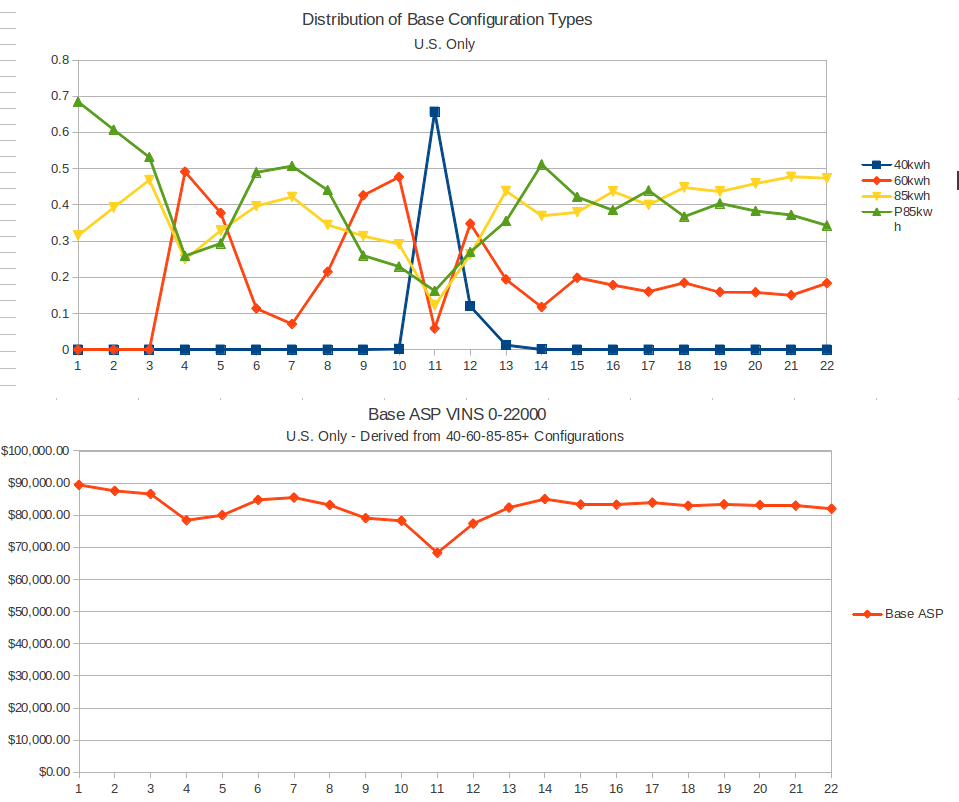

I posted this image in the Q3 predictions thread, but it's relevant here as well. The numbers show the configuration types and base ASP (sans options) per 1000 VINs for US deliveries only. Q2 is roughly 7500-14k and Q3 is roughly VIN 14k-22k. Q3 looks like the base ASP will be about $3k higher, but this graph does not include the $2500 price increase that was not a major part of Q2 but will be in effect for most of Q3. Also, Performance plus will give a bit of a boost. So I'll say US delivery ASP will go up about $5.5k from Q2 or around $98-99k.

There's a lot of assumptions here, but I'm pretty confident in a 100k-102k ASP for Q3.

�

�

Nov 5, 2013

RationalOptimist Thanks for all your hard work, Sleepy, and others. It seems to me that a lot of the recent volatility in stock price has been driven by growing investor awareness of -- and puzzlement in -- the VIN data. At one point it appeared to be surging like crazy, and I truly believe that helped fuel the rise to $190+, boosted by numerous Internet claims that 6-7k+ cars would be delivered in Q3. Then, as VIN trends tailed off, and Q3 estimates came back down to the 5500-ish level, confidence of the biggest bulls ebbed a little and the stock became vulnerable. Today a Seeking Alpha article uses the recent fall to claim both that Q3 will be beat and that US sales are plummeting. I hope Elon and team will take the opportunity tonight to clarify how the VIN system works (eg, what is the range of timings between issuance of VIN and a car entering production, and are there sometimes gaps in the numerical sequence?) and/or introduce some other sales tracker. The current situation seems to me to create risks of people getting hurt.

One other note: Elon opened the last shareholders letter by reminding people that maximizing profit is NOT the company's goal any time soon. I personally am not that concerned whether EPS hit, smashed or missed. Much more relevant to me is whether they communicate that demand is rising fast and that all the pieces are in place for a 2x production ramp-up for 2014. If they say that clearly, Wednesday will be bright green.�

Nov 5, 2013

sleepyhead I can't remember, but that was not his exact quote but rather my interpretation of it; I thought it was a well known quote here on TMC so I just quickly paraphrased it while typing on my phone. His words were something like this:

We will not show high profits in 2014. 2015 will be the year for that.

I haven't had a chance to read your megapost yet, but I am glad that you came up with a lower EPS and pointed out that EPS will not be the driving force for the stock price post earnings. Most of our EPS estimate difference comes from ZEV credits - about $0.10 EPS worth. I have no idea what ZEV will come in at, so I basically slashed it in half; and then you cut it in half again. It may turn out that I was not conservative enough with my guess.

- - - Updated - - -

Thanks for your great post. I was going to write something similar to what you wrote in the first paragraph, but the rest of the information, especially the graph, is amazing.

My ASP number might be aggressive, but I also factored in the 3% price increase for international sales to allow for currency fluctuation. On top of that the USD has weakened in Q3 quite a bit and international prices are fixed at the local currency, so this will boost ASP even more.

I also factored in an increased number of P+ sales that were not available in Q1. I think that the $100k - $103k range is most reasonable so I took the middle of the road.

I also thought that my delivery number might be conservative, so I thought that a higher ASP to offset that wouldn't overstate my top line. After seeing DaveT estimate 5650, I am not sure about the conservativeness of my delivery number, but it looks to be in the right ball park.

- - - Updated - - -

Great point on the VIN assignments and I completely agree with you that the stock price was going up when Craig's work on this topic got widely publicized. After the market figured out that Tesla isn't building 700 cars/week, the stock corrected 20%. I know that the fires played a big part, but the fires should have only had a temporary effect on share price and TSLA would have been above $200 today if TSLA was in fact producing 700/week.

I really hope Elon addresses this as well, since misinterpreting such information like this is dangerous. It is a reason why I thought that TSLA would be around $220 today on ER day. Since actual production is 20% below 700, it makes sense that the stock is 20% below 220. I think that we are in a good spot valuation-wise going into ER.

If TSLA says that it can hit 35k - 40k production in 2014, then the stock might take off post ER again.�

Nov 5, 2013

justdoit Just a note on that VIN chart slowing down, Elon did say that sales took a hit after the first fire but picked up after the blog post. If that's the case and the VIN data starts to also show that (that graph starts to trend up again) then that's pretty powerful b/c at least VIN data gives us an idea about the rate of sales.�

Nov 5, 2013

sleepyhead I am sure that the VIN chart is useful data, but I have not been able to discover how to use it yet.

I am not sure what triggers a VIN assignment, but I wouldn't be surprised if VIN's get assigned when all of the parts for a car are procured; in which case Craig's chart is not very useful in determining demand or production (since they order parts in batches). I think that it is dangerous data and was part of the cause for TSLA's volatility over the past two months; both on the way up and down.

Hopefully Elon addresses this issue on the CC today. Media really picked up on this topic and there are already two SA articles based on Craig's VIN assignment graph, and both articles are erroneous and flat out bad.

Craig has done a great job of putting the data together, but unfortunately everyone is misinterpreting the data either accidentally or on purpose to create more FUD.

edit: there are already two SA articles today that are using Craig's graph as the basis for their arguments.�

Nov 5, 2013

DonPedro We must (for now) kill the VIN analyses. They are adding unwanted volatility to the stock and creating FUD (and, in some cases, completely unrealistic expectations).

Craig has himself been very diligent in pointing out that we do not know what the data means yet. Emails to Norwegian customers have plainly stated that the assignment is random/arbitrary. This is supported by the fact that people ordering almost simultaneously and taking delivery almost concurrently ... but still getting their VINs assigned months apart (and with very different numbers).

Let's face it: The reason VIN assignment changed was that the old system enabled people to track production by tracking VINs. Do we really think that Tesla are so stupid they are not able to assign VINs in such a way that they stop giving away production figures?

- - - Updated - - -

By the way: Great job, Sleepy. The main difference from your projection to mine is ASP, where I think you are right. 22% GM is also on the aggressive side, but I like the assumption. They are getting a few % for free in Q4 (because of price increases), so if it is 22% in Q3 I think it will be way above 25% in Q4. So 22% now would be a very strong forward signal.

The wild cards are of course ZEV, R&D, SG&A. If they all move in one direction they could distort the picture, but I have a sense that Tesla would be managing that actively.�

Nov 5, 2013

sleepyhead I used 22% GM because in Q3 they are getting the added benefit of high margin signature vehicles and positive currency movements.

If they can't get significantly more than half way to 25% (19.1% would be half way) then I fear they will not reach 25% in Q4, especially with the dollar strengthening.

At one point I thought they might achieve 25% in Q3 (not out of the question completely) but my gut tells me it will be between 21% and 24%.

I could be very wrong on this.

I wildcards are ZEV, SG&A, and R&D (as DonPedro properly pointed out), but Tesla said in Q2 shareholder letter that they will be profitable without taking into account any ZEV revenue. That assumption was based on 5000 deliveries, but with 5700 deliveries they should easily exceed $0.10 EPS without ZEV. ZEV revenue is just a bonus.�

Nov 5, 2013

vgrinshpun In the interview linked below Elon states that currently the main focus of his work is increasing production. This presumably indicates that they already hit 25% margin (some time in October?) as he repeatedly indicated before that improving the margin was the main focus until the 25% threshold was exceeded.

Verpasste Zukunft�

Nov 5, 2013

techmaven This. Once European deliveries commenced and the time between sourcing parts for production to actual deliveries could range from 3 weeks to 5 months, VIN assignment became meaningless. Add to it that Tesla may be obfuscating the assignments or least changing the method of assignment, any short term analysis has become impossible.

I'm pretty certain that the price increases had little effect on GM in Q3. If you placed an order for a P85 in the second week of August, the car wasn't delivered until end of Sept. So only those in the U.S. that ordered P85's in the first 2-3 weeks of the price increase and chose to use the new pricing scheme would count towards Q3. Mine, for instance, went under the old pricing scheme during that time period. There were a lot of cars being delivered at the end of Q3 - so much so that I had to travel 2 hours to pick up my car. We don't know the mix of old versus new pricing, but I would hazard to guess that less than 50% of those cars have the new pricing scheme. If you not ordering a P85 or P85+ or getting delivery outside the U.S., it is likely that your order under the new pricing scheme could not have been delivered in Q3.

The upshot of all of this is that the effect of the new pricing scheme is actually in Q4, so a slightly disappointing GM number in Q3 would still get a boost in Q4 from the pricing change.�

Nov 5, 2013

ckessel Yes and no. Probably not the specific increase you're thinking of, but Tesla has been increasing prices for the last year. First the across the board increase, then more expensive rims, upped the warranty cost, added costs for the rear carbon fibre spoiler, etc. It's been a steady stream of small increases and so the average sale price of the car, at least the top end cars, has been steadily increasing.

Getting the same decked out P85 I got December 2012 would cost me a good 10-15% more now than it did then for the same car.�

Nov 5, 2013

techmaven I agree with that. Q3 is also the first quarter that had full availability of the P85+, and certainly there must have been quite a few people that waited for the early reviews of delivered P85+'s before ordering. So definitely the top line optioned out car price has been increasing. However, the big pricing change that took effect August 1st has probably little effect in Q3. That would have been 5% on the price of my P85. Tesla did make a number of options pricier while unbundling a slew of options, so even if ASP's don't shift as much, there should be a good effect on GM. That change will take effect mostly in Q4.�

Nov 5, 2013

hershey101 So I ordered my car back in Jan '13. I ordered the P85 for 105K. The exact same car today costs $120K (just in case anyone wants to compare prices). And I think it cost about the same back during the summer as well... So they definitely increased the prices on stuff I was interested in buying. (No 21" wheels or P85+ for me. The Northeast winters & pot holes don't work well for the bigger rims).�

Nov 5, 2013

DaveT I think it's stretching things to use that quote from Elon to say that it indicates they've reached 25% GM already. Elon has mentioned that he's been focusing on production issues all year (along with service during the spring and now Model X design). Saying that he's focusing on increasing production doesn't presume that they've hit 25% (ie., when the interview took place in October). Also, gross margin improvements need to be started/implemented months in advance so pretty much 99% of the GM improvements to reach 25% have already been implemented but that doesn't necessarily mean that they've reached that 25% target. All it means is that the improvements have been implemented and it could take some time to realize them. I'm not saying they haven't reached 25% GM in October, I just think it's highly unlikely but we'll see how much progress they've made with GM when earnings get released soon.�

Nov 5, 2013

fjm9898 One thing people some people might be over looking when talking about GM is that is averaged over the quarter when reported in the ER (at least this is my understanding). This is why i have always kept a 20% GM in my calculations. They would have to be at 25% now to really be any higher, or had a nice gap up, or they ended Q2 alot higher then i thought. (last being most likely the case) Doesnt hurt to be conservative though.�

Nov 5, 2013

sleepyhead My understanding is that in Q2 Tesla produced 400/week until something changed in June to reach 550/week (probably with overtime for quarter end push). So the pieces for higher GM in Q3 have been put into place in early June, and started materializing 6-8 weeks later as Elon once stated. Sigs, P+, no 40kWh, less 60kWh, should have a huge impact on GM. I think there might be a nice surprise.

I might be a little aggressive on my GM target, but I would be very disappointed if it is below 20%.

One weakness in my model is that I assumed all cars get GHG/Cafe credits (I think DaveT didn't change this either when using my spreadsheet). If EU cars don't get those credits then my revenue is overstated by about $4m and EPS by $0.02 - $0.03. Not a material impact, but something to keep in mind. I will try to research this topic later.

There are also all sorts of unknown variables that are attached to EU deliveries that are impossible to model in without having any previous EU sales. We will have to dig into the financials from Q3 to find out how EU deliveries are impacting the financials.�

Nov 5, 2013

vgrinshpun That is why I used presumably in my post. Presumably = reasonable as assumption. There was no intent to indicate certainty.

This is the first time when Elon publically stated that his main focus is increasing production. He did mentioned focus on production issues before, but increasing production was not one of those issues. In fact during the Q1 there was a specific question about increasing production which Elon responded to by indicating that it does not make much sence to focus on increasing the production before reaching the target margin. He than emphasized that main focus was reaching the target margin.

I would not use "highly unlikely" charachterization here. The guidance was that average gross margin in Q4 will be 25%. Simplifying margin progress as a straight line and taking into account that some cars produced in Q3 will be delivered and accounted for in Q4 would indicate that they need to be at 25% before the midpoint of the quarter. It is not certain that they have hit 25% margin in October, but it is likely.�

Nov 5, 2013

DaveT Sure it's possible. I'm just hesitant to say "likely" until we have more evidence. Earnings in a few hours should give us some clues. I was thinking they'd hit 25% GM in early-mid November to average barely over 25% for Q4 but if Tesla reports higher than expected GM for Q3, then they definitely could have hit 25% GM in October.�

Nov 5, 2013

vgrinshpun Got it. Hesitant to say likely = highly unlikely:smile:�

Nov 5, 2013

DaveT Sorry I should have said I personally don't think it's likely. Highly unlikely was probably too strong language. I just want to see more evidence that Tesla was close to 25% GM exiting Q3 before moving up my expectations of them hitting 25% GM in October vs my current early-mid November expectations. Again we'll find out in a few hours.�

Nov 5, 2013

DonPedro Well, counts in both ends of the quarter. For instance: 14% in Q2 might have been 9% at the start and 19% at the end. Then Q3 could be 22% by starting at the same 19% and ending at 25%.�

Nov 5, 2013

sleepyhead Bloomberg will be talking about TSLA right now after commercial break.

- - - Updated - - -

Cory Johnson says TSLA had two models, but got rid of one because of low demand and kept only one model starting at $82k. Also said that Tesla is losing money hand over fist on every car sold.

Barclays Auto Analyst says that Model S and X can support $100 share price, but to get to $200 valuation it needs to produce 500k - 600k cars by end of decade. Says that S and X can see about 70k demand worldwide. They have $140 price target. He expects TSLA to beat estimates by 500 deliveries, and also forecasts EPS beat. Says that the immediate (next year) future looks bright for Tesla, but when you look at long term it starts to get dicey. Current car is a great value against other high end vehicles, but Gen3 at $35k-$45k might have issues (it sounded to me like he doesn't believe Tesla can achieve long range battery pack at those prices).

Bill Maloney - says that the chart does not look good and today's action was weak.

Consensus - not a good idea to get into TSLA right now.

- - - Updated - - -

Ironically, I saw CJ earlier on Bloomberg today talking about Twitter and he kept talking about how optimistic he is about everything and that he always looks for positives and silver linings. That his brain is designed to always look for positives, blah, blah, blah.

So he took Twitters numbers (can't remember exact numbers but here is the gist of it): Rev - $150m, costs - $215mln, loss -$65m.

But if you strip out stock based compensation and depreciation (seriously, I have never heard anyone stripping out depreciation), then you get a $9m profit.

I never heard him ever try to find any positives in TSLA or Tesla, even though the company is the most positive thing that has happened to the planet in 2013.�

Nov 5, 2013

callnaveen Thank you so much for your help Sleepy, you the best.. .being on vacation you are contributing so much. Good luck to all.�

Nov 5, 2013

aznt1217 Looks like Elaine was spot on with the bullish case of 5500.�

Nov 5, 2013

hoang51 Actual: 5,500 cars delivered, 1,000 of those to Europe. $603 million in revenue. $0.12 EPS. 21% gross margin excluding ZEV credits.�

Nov 5, 2013

sleepyhead The reason why TSLA is down 10% has to do with the following items from shareholder letter:

We expect our non-GAAP profitability to be about consistent with Q3. Analyst estimates for Q4 were $0.20, so another $0.12 in Q4 is a disappointment. This is the major reason for the sell-off.

Other less than stellar items include:

25% increase in R&D in Q4 and 20% increase in SG&A.

Q3 results were good, but guidance is disappointing. No 2014 guidance doesn't help either.

�

Nov 5, 2013

aznt1217 .20 cents? I thought .11�

Nov 5, 2013

sleepyhead Q4 consensus was 0.20 and they guided towards 0.12 or so.

That is why the stock is tanking.

This has nothing to do with Q3 results which were good.�

Nov 5, 2013

Mario Kadastik That and I think the biggest so far is the lack of concrete FY2014 guidance. My hope is that Elon will elaborate on the battery deal and if he does throw out the 1200-1500 cars / week capacity that he did in Munich at end of 2014 and that is where they are aiming (or that they aim to about double the current production rate) i.e. all the things we know already from German interviews and London talks etc. Then this might work into a form of guidance going forward.

The stock is already slightly recovering, above $160�

Nov 5, 2013

ModelS8794 Sleepy, looks to me like ASP came in at $105k! (ex 10mm ZEV and ~8mm GHG)

And guiding for similar ASP next qtr. I find that incredible, but...�

Nov 5, 2013

DonPedro Yeah, very strong! Makes me believe they will go significantly above 25% GM in Q4.�

Nov 5, 2013

sleepyhead I think that a lot of you covered all of the positives in the short-term trading thread; and there are many positives for the long-term investor, so I will go over the negatives here that virtually nobody pointed out:

-SG&A is growing out of control. Up 34% in Q3 vs. Q2. Tesla guided towards 20% increase in Q4. SG&A is growing twice as fast as revenue,which is not good.

-R&D up "only" 10%, but forecasted to rise 25% in Q4. Once again not good.

-GAAP loss getting bigger QoQ. I don't really care about GAAP, but the stock-based compensation worries me a lot.

-EPS guidance for Q4 same as Q3 results, which is 40% lower than analyst consensus. This is the main reason TSLA tanked today; momo traders are out.

-No 2014 guidance means no forward visibility, i.e. increased risk due to uncertainty, which leads to lower share price.

-Deliveries are growing at a 5% QoQ pace, which does not extrapolate into 100% YoY growth rate, but more 30%. We expect a lot more from Tesla, but there is no evidence to point that Tesla will be able to achieve 40k deliveries in 2014. I believe they will be able to meet that number, but the market is not so sure.

-Share count is growing too fast for my liking. Another 2m share dilution coming in Q4, which looks to me like 100% is from stock-based compensation. Even though companies strip this out to get to non-GAAP earnings it is a real cost to shareholders and I don't like that companies do this. It is cheating, but all companies do it.

I wrote a couple of weeks ago that TSLA is now a buy and hold investment and people like bonnie, who stay true to this strategy will be ok. It doesn't matter if the stock goes down to $10 tomorrow if it ultimately ends up at $1000 in the future. I also wrote that playing options during earnings does not give you a good risk/reward ratio like it did in Q1 and even Q2. It will be very hard to make money with short term options on TSLA. I recommend taking a buy and hold strategy.

That said, I played this ER mostly with weekly OTM options; they will all go worthless tomorrow and I will lose a lot of money. I am not worried though, because it is part of my bigger strategy and I am now in position to buy TSLA at a discount. I will cover my trading strategy in more depth in the future, but wanted to add that I buy certain options for a reason and I always have a plan. That's why when people ask me what options I bought, I usually refuse to respond. I am ok with taking a 100% loss, because I have a plan to deal with that loss and even though I buy call options I might actually be rooting for them to expire worthless (this might not make sense to you, and that is why I don't like to disclose my positions). If TSLA went up to $200 tomorrow, I would make a nice gain. But now, if it goes down a lot, I am in position to make a lot bigger gain. Only difference is that it will take me a little longer. But I am patient and I can wait for more money in the future vs. less money now.

As it stands my Q3 options will go worthless tomorrow and my legacy bull call spreads need some work to finish at max payout. I will be sitting on the sidelines with TSLA right now and plan on taking a bigger position if the stock goes down a lot. I will re-evaluate TSLA in a couple of weeks. I took some profits on my weeklies, but kept most unhedged going into ER. I didn't lose too much of my initial investment, but my big paper profits are getting wiped out tomorrow.

It is impossible to tell how the market will react over the next couple of weeks, but I expect TSLA to go down in the short run. Then again, I am sure that Elon has some aces up his sleeve and he will dip into them to keep the price stable.

The most important take-away from this earnings report is that nothing has changed. Tesla is still on track to dominate the auto industry in the long run. Its just that it will take a little longer than some of us hoped. No reason to panic now, since fundamentals are intact.

There will be a period of consolidation, but once production constraints are resolved TSLA will take-off once again.

The way to invest in TSLA is to buy and forget. Open up an IRA or roth-IRA (if you can), put some money in it and buy TSLA at a discount. Then forget the password and don't login for the next few years. It is still a great long term play. If you are playing short-term options with TSLA then you are fighting an uphill battle.�

Nov 5, 2013

Robert.Boston I worried about this, too, but my read is that a lot of the stock compensation is defined in terms of # of shares. As the share price has risen dramatically, so to has the cost of the share-based comp.�

Nov 5, 2013

aznt1217 I don't know Sleepy, I think this is one of those situations where analysts and money managers reevaluate. I know we are down a ton right now, but the main thing holding price targets back was execution risk. The letter (to me) is another thing to allay that fear.

I also think Sg&a expenses aren't necessarily a negative. In this quarter Tesla had to do a ton of hiring because of international roll out. These will stabilize in due time.

Granted, in my mind I wrote off my Nov 200's but I still think there's a possibility of a run by the end of this week. Elaine Kwei, Andrea James, and Deutsche are probably reassessing and will revise up or reaffirm the hold because of gross margin progress and performing at or above their expectation. Except now there is the dimension of global demand.�

Nov 5, 2013

MikeC My friend's brother is a service technician for Tesla and said he was given 100 shares when he was hired.�

Nov 5, 2013

sleepyhead I am not worried about $ loss on GAAP basis, but rather the # of shares issued as stock based compensation. 2 million shares per quarter seems like a lot, by the end of the decade their will be 200m shares outstanding at this pace.

I haven't looked into details, but Tesla guided towards 139m shares in Q4 vs. 137.1m in Q3. I assume all of that is stock based comp, since there are no other potentially dilutive events coming up; that already happened in Q2 and Q3 due to convertible note offering.

edit: hopefully as the price goes up there will be a lot less shares issued to employees due to higher share price. At the same time, as the company expands there will be a lot more employees hired who will get shares.

- - - Updated - - -

There is a very good chance that you might be right.

I am not talking about the price movement for the rest of the week, but rather over the next couple of months. I see no reason to rush in and buy shares now. I am in a wait and see approach because I don't see the stock going to $200 any time soon; I hope that I am wrong because my bull call spreads need TSLA to reach $200 by Dec. expiration.

We might see a period of consolidation and I will stay patient before buying a lot of TSLA. In the mean time if I am wrong and TSLA takes off, then my BCS will make me money, so it is a win-win for me.

Another thing that worries me is that the overall market has been running really hot and is due for a pullback before the annual Santa Clause rally in December. I think that the short-term favors the shorts, but I am not willing to short the stock or buy puts. I am just thinking out loud to spur discussion.

These are just my opinions that can differ completely from the market's opinion. My TSLA exposure is going to be very low tomorrow due to TSLA tanking and I am taking a wait and see approach.�

Nov 5, 2013

DaveT +1. The beauty of common stock is that if you're invested in a good company you can wait out the bumps in the road even if it takes a couple extra years. With options, you're not just betting on the company but you're betting on timing as well. It's exponentially more difficult.�

Nov 5, 2013

kenliles +2

Strongly agree. Stuck with stock and LEAPS. Sure helps me sleep at night�

Nov 5, 2013

AlMc Precisely. That is also why it is potentially can have an exponential return. I am a stock holder at heart. Bought a couple Nov. calls just to see how they worked along with a couple Jan 2015 LEAPS. The loss on the Nov calls will be close, if not, 100%. Lesson learned, luckily at not too great a cost.

What does Sleepy say 'Buy and Hold'.....Yep. Oh, and maybe get a couple LEAPS. :biggrin:

Thanks for all the brother/sisterhood on the TMC forum. Truly 'good people'.

Sleepy...Get some sleep and enjoy the beach.�

Nov 5, 2013

aznt1217 100% agree sleepy. This is a long term investors play right now. I know you are short term oriented. I usually am a long term investor and make careful choices. I tried to play the short term game and got burned, but there's still a chance it will bump. After listening to this call I'm noticing the evolution of questions. It's as if Model S ramp up is a given, they focus SO heavily on the massive ramp up for NUMMI's former capacity.�

Nov 6, 2013

DonPedro I agree with you, Sleepy, regarding stock based comp. I also don't like that they take that out of the non-GAAP accounts, which they state they use for internal governance purposes. They should be careful not to treat stock grants as "free".

I support their use of non-GAAP wrt. lease accounting, but the credibility of those numbers is hurt by this practice.

(On the other hand, I understand their reasoning - as a young company they are rightly focused on cash flow, so they make non-GAAP as close to cash flow as possible).�

Nov 6, 2013

vgrinshpun Sleepy, do you have any thoughts on why Tesla decided not to include any 2014 production guidance in the shareholder's letter? After all the information on 2014 and 2015 production goals was provided by Elon during the visit to Germany, and he did throw around some numbers, including the plnanning " kind of next generation production line for the S and X".

The second question is regarding their use of stock as a part of compensation packages. Do you think that because of this Elon has an incentive to do some targeted release of additional information to prevent further erosion of the stock price.

I am basically a long term investor, but am using margin and options as a share accumulation tool. I feel your pain as I am also likely to take heavy loss with the Nov 16 call spreads. Ironically this ER call was all about exceeding expectations on how agressively company is planning major expansion of the production, short, medium and long term, and this is, after all, what supposed to firm up valuation that is not based on current performance, but can only be justified in context of rapid company growth.�

Nov 6, 2013

sleepyhead 1. This is what I wrote in DaveT's thread a few hours before ER:

And I still think this to be the case, i.e. they don't know when supplier constraints will be solved so they can't give guidance. If they were close to resolving the issue they probably would have given guidance.

No guidance means supplier constraints will continue into early 2014.

2. I really don't think that Elon cares that much about short term price movements and I don't think he spends too much time trying to figure out how to prop up the share price. He just does his job and has pre-arranged plans for press releases. I highly doubt that he sits with aces up his sleeves only to use them when the stock needs some good news. I don't think he is reactive to the stock price at all.

Side note:TSLA is all about buy and hold. There is still a lot of money to be made day trading the stock, but you have to know when to short it as well if you are going to day trade; requires a lot of skill. If your day trading consists of buying front month call options then you will need a lot of luck; in the long run the odds are against you.�

Nov 6, 2013

kenliles I simply could not agree more...

Save some timing on offerings and short squeezing, he's too smart to even look at the stock price imo -

well said sleepy�

Nov 11, 2013

sleepyhead TSLA is Cheap? Still not Buying

Now that TSLA is in the 140s, it is slowly becoming a bargain again, but I am still not a buyer. Not that I don't like TSLA but I just don't see enough near-term upside in order to get in. I think there is some possibility that the stock goes back into the $150s quickly, but I don't see it going much higher in the near future. At a minimum I would expect a double bottom and there should be another buying opportunity in the 130s. I can also envision a scenario where the stock goes a lot lower from here, and to be honest that is what I am waiting on before I go into TSLA full force. I still have my December bull call spreads, but the stock needs to go up 20% for me to cash in on them. I will hold them to expiration, but I have already written them off as a loss since I don't see TSLA going that high. Let's take an objective view at what is in play for TSLA:

Post ER Sell-Off - Remember that TSLA went as low as $146 a day post ER and that drop looked like it was only the beginning. Then we got news that a second Model S caught fire by running over some road debris, which caused the stock to go down to $132 but now it is back up to $145. What I am trying to say here is that the relief rally may not last too long. Yesterday evening I was thinking that if Tesla were to go down to $100, there would be a dead cat bounce somewhere along the way. This could be that dead cat bounce.

Second Debris Fire - This is not cause for concern as far as safety goes, but rather a cause for concern that Tesla might have to re-engineer the protective shield. This wouldn't be a problem, but a potential recall may be costly if not only to shareholders; bad news = lower stock price, even if actual costs are smallish. Also it might be more difficult to re-engineer while keeping battery swapping capability.

Elon Musk Blog Response - Unless Elon says that he will pay for a recall out of his own pocket, I cannot come up with a scenario where his blog post will do anything but cause the stock to go down (or at least not up by a big amount). Here is how I see the possibilities unfolding:

- Elon says that the car performed as designed and nothing needs to be changed.

- The car needs a recall and the battery shield will be redesigned for future models.

- The car will not be recalled, but future cars will have different shield design. Unlikely outcome IMO.

In either case, I see the stock going down. The market might interpret the first option as "there is risk EV's will catch fire and there is nothing anyone can do about it,". The latter two options will be perceived as costly.

Sentiment Shift - There is a clear sentiment shift with TSLA that started with the first fire and has been getting worse over the past week. There are still many people who believe that that TSLA is worth $60 like in Damodaran's DCF model. There are also a lot of people, who think like me, that there is no upside to purchasing TSLA shares right now, since you will be able to buy them cheaper next week and at worst at the same price next month. Sentiment is clearly bearish and it will take a lot more than one blog post from Elon to shift the sentiment. It might be a while before sentiment shifts to positive; probably not until we get good 2014 guidance as was the case with SCTY.

Market Perceived Growth Rate - This is the major reason why I am not buying any TSLA yet. We all talk here on TMC like Tesla's 100% revenue growth rate is a foregone conclusion and that it will continue for another 3-5 years. But Tesla has not shown that it is growing at that rate and the market needs to see evidence before multiples start expanding again; once again we need good 2014 guidance which will not happen for another 3 months. Let's take a look at actual growth rates:

Q1 4900 cars sold

Q2 5150 cars sold for a 5% growth rate

Q3 5500 cars sold for a 7% growth rate

Q4 6000 cars sold for a 9% growth rate

All this extrapolates into a 30% growth rate and not 100% as we all believe will happen. I believe that Tesla will grow revenues at 100% for at least the next two years, but there is evidence to the contrary and the market might not believe it.

Supplier Constraints - Investors are getting tired of excuses and there is no reason to buy now, when you can buy once the constraints are resolved. The market gave Tesla the benefit of the doubt in Q2, but now it will wait till they are resolved.

VIN Assignment Chart - I believe that this is the reason that TSLA went all the way up to $194. It looked for a while that Tesla was producing 700 cars per week and growing at a very fast pace. Even Wall St. analysts were using this chart to show how fast Tesla was growing. In reality it is producing 20% less cars, hence the 20% lower stock price.

Potential Upside - I believe that we need Q4 guidance before TSLA makes another big move up. On the other hand it seems like Tesla has had a lot of great news coming in post ER in the past two quarters, so I wouldn't be surprised to see more catalysts coming this week and next. But without any catalysts I don't see a need to buy TSLA right now. When that catalyst comes you will know when to get back in.

Potential Downside - There could be a NHTSA investigation or another fire. Just as there are potential positive surprises, there could be negative ones. The problem with negative sentiment is that it will take two or three positive catalysts to have the same affect on the upside as one negative catalyst will have on the downside.

Valuation - If Tesla were a mature company it would need $10b in annual sales, 20% gross margin, 10% net margin, and $10 EPS to justify its valuation. It would have to sell 100k model S/X per year. So that is still 2016 time frame. A lot of growth is already priced in even at a $145 price. Obviously TSLA deserves a growth premium, but since Tesla is only showing a 30% growth rate (QoQ in FY13), that growth premium is likely to decline until it can prove the 100% growth rate. Once again the buy point is the day of 2014 guidance (if around 40k) or supplier constraints are resolved and Tesla is producing at least 700 cars/week. 550-600 cars will not cut it. Many people still believe it is overvalued today.

TSLA's climb will not follow a channel and move gradually towards $1,000. Just look at AAPL's chart and follow the Apple PDF with the timeline. You will see that there were many periods where AAPL would get stuck in the funk at the disbelief of the Apple Investment forum members. Just look at how it hit $270 in Apr. 2010 and how it was still at $240 four months later, before going up 50% to $360 just six months later. I think that you have to pick your battles with these hyper-growth companies and right now the odds favor the shorts. I will get back in when the odds start favoring the longs again; i.e. 2014 guidance and/or supplier constraints resolved and heading towards 800 cars/week.

I still believe that TSLA will double by the end of next year, but I am starting to recognize that we on TMC are willing to give TSLA a much higher multiple since we are true believers. The market doesn't get emotional and it may take a little longer for it to realize TSLA's potential and our price targets may end up being a little too optimistic too soon. I remember reading in the AAPL PDF that the board had price targets that always took a little longer than expected to materialize. Because of this a lot of people ended up buying the wrong OTM options and some lost a lot of money because of this. I was thinking $400 at end of 2014 is doable, but now I am thinking that we are 6 months ahead of the market on TSLA, and unfortunately it will take time for valuation to catch up. At the same time this allows us to buy TSLA while it is still cheap. On the flip side you have to be cognizant that you might be buying in too early and sometimes have to be patient to be able to buy in at a lot lower rate. This is especially true if you are playing options. They might seem cheap today, but I might be buying them a lot cheaper next month if TSLA consolidates from here.

General Market - Even though TSLA is a low-beta stock, there is a real risk that it goes down even further with a potential market pullback that can begin any day now. TSLA is low beta because it defied market gravity when sentiment was positive. It will not have this magic when the sentiment is bearish.

Final Word - As much as I would love to see Tesla make a swift recovery to $170 for my BCS's to finish ITM, I really don't see it happening that soon. I feel that TSLA is heading towards a period of consolidation that may last two to three months. I don't see the upside in buying TSLA right now, so I will be sitting on the sidelines for a while longer. I still feel that solar presents a much better risk/reward profile, especially right now, and I have the vast majority of my funds invested in solar right now.

Solar Bonus - If I had to guess what happens over the next two days, I would say that YGE and HSOL load up the bases tomorrow and then CSIQ hits a grand slam on Wednesday. This is a "just for fun" prediction and the markets can be very fickle and finicky, so nothing will surprise me with solar. Q4 is going to be extremely good for Chinese solar, extremely good! And even if Q3 is only good, I am expecting big guidance and comments from CEO's about the huge solar demand. It truly is an exciting time to be investing in solar and it is only getting better every day. It is actually getting exponentially better on the news front.

Sooner or later the market catches on and it is better to be in sooner than later. I kept buying JASO on weakness over the last few weeks and now it went up crazy on what seemed like a minor piece of news. When a stock is undervalued it will go up crazy on the smallest news. Now imagine if a big piece of news comes out on a company like JASO or SOL. These companies are priced extremely cheaply and it is easy for them to go up. Unfortunately, a lLack of news makes them go down, like is the case for SOL over the past two months. I have been buying a lot of SOL lately on weakness as well. I feel like it will eventually have its day, and it tends to happen a lot sooner than you expect (which is where I might go wrong with TSLA, by waiting too long to get in).

The recent typhoon in the Philippines was the strongest storm on record in the whole world. The cause for it coulb be global warming that could have lead to rising sea temperatures, which in turn leads to stronger hurricanes, a.k.a. typhoons, a.k.a. cyclones. This is a really sad story with tens of thousands losing their lives in this storm alone. This week also happens to be the week of U.N. Climate talks in Warsaw. And the Philippines are pleading for a rapid adoption of renewable energy. This could lead to striking a big deal by 2015, the new deadline established when the previous 2009 deadline was not met for a global climate deal. It is a good time to be investing in renewables and electric vehicles. Solar is going to be a big winner over the next few decades, and the market doesn't even see it coming. Great time to be an investor.

Tearful plea from Philippines delegate as typhoon overshadows opening of UN climate talks - The Washington Post�

Nov 11, 2013

aznt1217 Man every time I read your post I second guess. I really was wondering about how to play CSIQ if there's still room to run with ER on wed. I bought TSLA and am starting to regain my losses on my ER plays.

What are you doing for CSIQ ER if anything? Them preannoucing made me think of a SCTY scenario, I am trying to see if their management likes to give guidance. Thoughts? Maybe I missed something.�

Nov 11, 2013

AlMc Sleepy...;Thanks for your mega post. It does appear that solar has more short term (days, weeks), medium term (weeks, months) than TM at this point. I still have some LEAPS and a little TM stock but more in solar, and some 'cash' that I am having 'analysis-paralysis' issues in determining proper stock purchases. I would like to commit this money to TM but I do not trust the near term price as a good time to renter.�

Nov 11, 2013

sleepyhead If you are happy with your ER play then don't change it because of me. My ER plays have not been huge successes in the past, but I know that I will hit a home run every now and then that will more than offset my strike outs. That is just a strategy of mine that makes sense for my investment purposes and can't recommend it to others though.

CSIQ is still really freaking cheap no matter how you look at it. Once you start factoring in forward earnings, as in 2014 EPS and revenue, then you are looking at a joke of a share price even at $30. The problem is that the market might take longer to figure this out, but that is why I always recommend to buy and hold. Those who bought JASO at $11, then $10, and then more at $9 in just the last month must be feeling really smart right now; I know I am.

Buy and hold.

I have no doubts about CSIQ ER. I have seen some saying that if guidance is weak, then the stock might fall post ER. That person must not have done enough research on the company, because if you do enough research then you should know exactly what kind of guidance to expect; and it should be good. Stock prices are not all about guidance anyway, they are mostly about macroeconomic factors and to a lesser, but still significant, degree - company and industry specific factors.

Just a note to all of the options players: I really don't think you all should be asking others for opinions when to close out your positions. Nobody can tell when the best time will be and it has to be 100% up to you. Don't let others influence your decisions or don't play options at all. Remember that any advice you get on closing out positions will almost always be wrong, because there is always a better time or strategy.

Remember that SCTY went from $52 to $28, or nearly 50% down before regaining its mojo (with 2014 guidance nonetheless). TSLA is still only down 30% and can still go down a lot lower before it goes up.�

Nov 11, 2013

Jonathan Hewitt Haha, sleepy I think you just solidified all my recent thoughts. I've had a lot of the same thoughts as you which started to form after the drop from $194.50 and are pretty concrete after you eloquently put everything together. I've been looking at my gains and my solar is acting like TSLA did for me earlier this year, except solar doesn't look like it's stopping any time soon. For some reason I still have 40% of my portfolio in TSLA (was much more before the drop). I think there's two reasons why I am still heavily in TSLA and I will list them in case other people are in the same boat. First, I think I want to root for TSLA and "support it" by owning a relatively large amount of it, even if short to medium term gains possibly have a poor risk/reward ratio. This obviously doesn't make sense financially but people getting emotionally tied to a stock happens all the time. Second, and perhaps the bigger issue, I got in TSLA in the 30s and really don't want the tax man to steal a large percentage of my gains before they are long term. I've already been bumped up a tax bracket this year thanks to TSLA. I know you shouldn't make investment decisions solely on tax issues but when you have such a large amount of gains it is hard not to.

My LEAPS don't go long term until May so I think I'm selling them tomorrow. I'm definitely going to keep some TSLA as a long term investment but need to think about if I want to keep all my shares or not.�

Nov 11, 2013

aznt1217 I think your post just put me over the edge. I've done my research and have been wanting to pull the trigger and needed more perspectives.�

Nov 11, 2013

fjm9898 I believe this was direct at me and that is fine, but i just wanted to lay my cards out. As you said everyone is free to do what they want and i expressed my opinion on the subject matter. The street has been real, for the lack of a better term, bitchy as of late. I do agree that CSIQ is on the positive side going into ER but the beating I have taken this ER season has made me weary of holding such a large, short term holding. I expressed my concerns on the fact that is seems like just about nothing gets a win this ER season and i have paid for it so far, so i will gracefully bow out at the expensive of being wrong and missing out, but locking in gains. Just like i was with SPWR. Pulling out of SPWR was a good move on the ER reaction, but it could turn out to be a net equal as SPWR recovers, no big deal. Not saying my pull out of CSIQ is the right move, just saying it was the safe move for me. I am still heavily invested in CSIQ, I just didnt want to risk my short term options and their major gains.�

Nov 11, 2013

Norse Analysts follow CSIQ, and I am pretty sure whatever happens in Q3 ER they will have a PT raised afterwards.�

Nov 11, 2013

kenliles Agree with much of sleepy's post and have a substantial solar position. At the same time, I'll point out that sleepy's own advice about solar (buying on bearish sentiment) is the opposite of selling TSLA here. He's saying he's not adding currently. I think TSLA might go lower as well, but if you are buying stock or LEAPS, bearish market is exactly when you should buy albeit slowly if you agree the catalyst will be later than sooner. Waiting until the sentiment is bullish on a stock that has already established much greater highs will be too late. I would advise keeping and slowly adding long term position while TSLA is stuck in bear mode, just as sleepy recommended for solar stocks, that time is now and over the next weeks for TSLA In this respect I probably disagree some with sleepy, although I do agree it may revisit the $120-$130 , the other side of current bearish sentiment is very much higher, when it switches it will be fast�

Nov 11, 2013

DaveT Hey sleepy, thanks for your post and taking your time to write your thoughts down. It got me thinking and I'll post a reply post over in my article thread.�

Nov 12, 2013

sleepyhead I agree with this. I didn't mean to say that now is not a good time to buy TSLA; it probably is. It is not a good time for me, because I think the short term favors solar, and I believe that I will be able to buy TSLA at a similar price a few weeks from now.

If you are looking to buy more Tesla on this dip then definitely buy some now and be ready to be buy more if it goes down further. I would be buying right now, but I think that solar is at an inflection point and I don't want to miss out. The main reason I am not buying TSLA is that I believe there will be a consolidation period and I am looking to buy options, which can become a lot cheaper in the next few weeks. If I was looking at shares, I would have bought in the 130s for sure. I just like the solar risk/reward ratio on shares that much more. I know that a consolidation period will make TSLA options a lot cheaper and I am patient.

There is a good chance that TSLA will shoot up and I will miss out on this bargain, but I play the odds and they are currently favoring a period of weakness.

And this does not contradict to what I recommend with solar: solar is a growing industry that is "undervalued", so you have to buy on every big dip. TSLA is a growing company that is "overvalued" so you have to be more careful on the dips. Buying the dips is obvious when nothing changes. But it looks like sentiment has changed and now buying the dips is not an obvious thing. If solar has a weak Q3 and gives weaker than expected guidance, then buying the dips will not be as obvious anymore either. Every stock requires a different strategy.

- - - Updated - - -

I never said to sell TSLA here, if you held on for so long then selling at the bottom is probably the worst thing you can do. If I were an analyst it would probably equate to a short-term "hold" rating.�

Nov 12, 2013

Jonathan Hewitt Agreed, but I also think that sleepy doesn't have a core long term TSLA position. I DO think my TSLA stock and LEAPS will do very well over the next year or two but for the forseeable future I don't see them doing better than solar. I only have so much capital and I think it makes sense to put it where I can have the best return. I'm also using some margin right now and I don't think it is very safe using on highly volatile stocks like TSLA and solar so I should sell something. At a minimum I think it's coming down to my TSLA LEAPS. I'll for sure maintain some stock assuming I don't decide to keep all of it and I have some stock in my IRA for long term purposes.

EDIT: Ok, sleepy actually straight up said he didn't say to sell. I still think I'm selling my LEAPS but am leaning towards keeping all my stock.�

Nov 12, 2013

sleepyhead Looks like HSOL and YGE both swung and missed.

HSOL is getting pummeled in pre-market on a huge miss that was due to a one time charge related to writing off deferred tax assets. Guidance was great with 13%-19% shipment growth rate QoQ. Some companies get excused from having one-time charges and others don't.

YGE had results that came in-line with expectations. Their gross margin increased by 2% to 13.7%. YGE is giving back yesterday's gains in pre-market though. YGE is a loser because it has way too much debt. It isn't anywhere near profitability with 14% GM, whereas SOL and CSIQ would be profitable with that GM. YGE needs 20%+ GM to become profitable and that is why I do not invest in them. Interest expense is eating away all of their profits and there is nothing they can do about it.

There is a reason that I don't invest in these two companies, and it is unfortunate that these two are leading off the earnings season for Chinese solar companies. It looks like they are going to drag the entire sector with them today.

Fortunately CSIQ is reporting tomorrow and I think their results will be much better. Just today they announced two new module supply agreements, one in Turkey for 2.3MW (which is like 30% of total Turkey installations) and a 32MW supply agreement in China that will be delivered this month. This is great news, since it adds another 32MW to Q4 guidance on top of the 100MW deal they announced last week in China. We know CSIQ had a great Q3 and it looks like Q4 is looking really promising as well. It's too bad they won't give 2014 guidance, because next year is looking really good for them.

I am going bargain hunting for solars today. All of the losers have reported and I am optimistic about CSIQ's results tomorrow and JKS and TSL next week. My favorite picks have yet to report, while the others are out of the way:

CSIQ

JASO

SOL

JKS

and

TSL - probably a good one, but I don't invest in them.�

Nov 12, 2013

AlMc HSOL getting hammered. I have no money in this company. Since it appears that it may be down 20% today and the problem seems to be the one time charge with an otherwise good ER do you think it is a good buy on this major dip. It would appear so to me as a speculative play.

- - - Updated - - -

Just finished reading their 2013Q3ER...think I will stay away from this one.�

Nov 12, 2013

Fast Laner Looks like HSOL and YGE both swung and missed.

How did these two make it to the line-up and also your previous post?

Could they eventually have advanced on balls?

Fast Laner�

Nov 12, 2013

sleepyhead I just wrote about them, because they are the first two Chinese solar companies to report earnings for Q3. Now that the losers are out of the way, the real fun will begin with CSIQ tomorrow.�

Nov 12, 2013

ckessel Was that just the favorites of those that hadn't reported yet or has SPWR dropped off your list?�

Nov 12, 2013

sleepyhead

SPWR is still the safest bet in solar (if there ever was one). I am talking about Chinese solar companies only here; I mentioned Chinese solar in the other part of the post you did not include in the quote. I will be buying a lot of SPWR options if it continues to consolidate and IV goes down. I am patient and I can wait.�

Nov 12, 2013

ckessel Ah, sorry. For whatever reason, it struck me as the start of a new thought when you started the paragraph about hunting for solar bargains rather than a continuation of the analysis on the Chinese companies. That and I don't really think of CSIQ as a Chinese solar, though I suppose it basically is. My brain's fault, but I'm glad I asked�

Nov 12, 2013

Mario Kadastik Any thoughts on STRI earnigns report? The stock itself is getting hammered somewhat with -11.6% and it has tripped the short sale circuit breaker.�

Nov 12, 2013

sleepyhead

Looks like we had our dead cat bounce yesterday.

Now the question is will this be a double bottom or will the stock continue to go down? I am still not a buyer, but might start nibbling at TSLA if it hits the $120s.�

Nov 12, 2013

ckessel The news highlighted when I look it up on Google looks pretty grim.

Losses Deepen At Enfield's STR As Company Considers 'Alternatives' - Courant.com�

Nov 12, 2013

kenliles CNBC tweet- Source says no discussions of a recall:

Twitter / Search - #CNBC�

Nov 12, 2013

Bgarret With all the pre-announcements and Turkey, Ontario and China deals, why not a whisper about the 200 + 300MW deal in Pakistan for 2014 & 2015....will they fold that into earnings, or is it not material? They seem curiously quiet about what looks on the outside like a major deal.�

Nov 12, 2013

sleepyhead It is definitely material and a big deal. My guess is that they are saving the announcement for ER day FSRL-style, but I don't know for sure. Maybe there is some paperwork that is preventing them from disclosing it officially. It is hard to tell, but my guess always was that they will save this big announcement for ER day for a double whammy of positive news.

If they don't announce it then I hope an analyst brings it up on the conference call. So I guess they kind of have to disclose it.�

Nov 12, 2013

smorgasbord No-one expected a 100% growth rate each quarter. Except you, apparently. We all were targeting close to a 100% YoY growth rate. 22K cars in 2013, 35K-40K cars next year, and then Model X adds to that for 2015.

In Q3, Tesla sold 5500 cars. They made close to 6500 - the difference are in the shipping pipeline. Now that the pipe's mostly filled, production should map pretty closely to deliveries, unless they add new countries that also need a new pipeline.

It's real hard to predict where Tesla will go in the short-term. As we start seeing Model X Alpha prototypes, ride events, test drives, etc., the stock could easily take off. Heck, the promising service announcement could give a boost. And yes, there is risk on the downside as well.�

Nov 12, 2013

Mario Kadastik While I agree that there is a pipeline, the current QoQ growth rates is what Sleepy was using to come to the 30% YoY growth rate region. Yes we expect 100% growth from 2013 to 2014, but the past three quarters haven't shown that this is the course right now. We know that it comes from supplier constraints right now, but Tesla has to demonstrate that they resolve those and the QoQ numbers go up enough to demonstrate YoY of 100%. Once they do (probably Q1 2014 production numbers show enough of an increase of Q4 that we can estimate full year to be 100% YoY and if the guidance already at Q4 agrees with that, then the stock price will correct back to the proper growth path.�

Nov 12, 2013

aznt1217 I was going to buy CSIQ today, but want to see movements tomorrow first I think there will be some Q3 ER jitters that I can capitalize on.�

Nov 12, 2013

fjm9898 CSIQ report before open, so you missed the boat.

Fly on the wall has CSIQ consensus at 0.36 as well sleepy, just a FYI.�

Nov 12, 2013

Mario Kadastik He can still get stock after hours...�

Nov 12, 2013

sleepyhead Yes, this is what I meant. I still believe that there will be 100% delivery growth rate in 2014, but Tesla is showing a 30% growth rate when you extrapolate the deliveries growth from Q1 to Q4E 2013.

Thanks, that is what yahoo and marketwatch shows. That 0.60 number from Rothschild is just one estimate, and that is what raised consensus to 0.36. I haven't run the numbers in a spreadsheet but a quick calculation shows that CSIQ should beat the high end estimate of $0.60.�

Nov 12, 2013

smorgasbord I still think you need to factor in the cars Tesla built in Q3, but hasn't delivered due to stocking the Euro pipeline, into the equations:

Q1 4900 cars

Q2 5150 cars for a 5% growth rate

Q3 6200 cars for a 20% growth rate

The question is what Q4 will come in at. At the stated 550cars/week, that would be 7150 cars for Q4, or a 15% growth rate. And that's if they are steady state throughout Q4.�

Nov 12, 2013

Norbert Like me...�

Nov 12, 2013

aznt1217 I screwed this one up. I didn't realize it was before the opening bell. I'll have to play the premarket game and use margin and bank on a pop.�

Nov 13, 2013

sleepyhead I understand what you are saying, but that is not how the market works. The market only looks 3 months out and all they see is deliveries. Producion is increasing faster, but so are cars in transit: next quarter it will be cars in transit to Japan and UK (just making this up, but there will be new countries) on top off Europe, and the quarter after that it will be Chinese cars in transit in addition to everything else. So even if production grows at a faster pace, so will cars in transit. Remember that the market has a short term view.

Side note: After taking some profits on CSIQ (still holding a ton of CSIQ, because it is only getting started), I started dabbling at TSLA once again today in the $139's. Bought a few June calls, J15s, J16s, and stock. I don't think the worst is over, but there is a chance that we had our double bottom yesterday (although it did not hit $133 like I think it should) and don't want to miss out. I bought longer term calls, because I actually hope that TSLA goes down lower so that I can buy more next month. If it doesn't go down then I will make money on what I bought. It is a win-win situation and that is how I invest: put myself in win-win situations.�

Nov 13, 2013

FredTMC Hi SB. Question for ya... Where are you getting q3 "produced" cars as 6500?! I don't think TM has disclosed how many were produced in Q3. If they really produced around 6500 they should've disclosed it during Q3 ER/call. IMO, this would've resulted in a smaller price hit once the street realized they had great Production increase qtr to qtr but "cars in transit" to EU resulted in only 5500 deliveries. My view is that TM produced less than 6500 in Q3, or they would've used this "transit" explanation

comments welcomed�

Nov 13, 2013

sleepyhead Its very possible that they only produced ~5,800 cars and that they stopped shipping cars in September to maximize deliveries in Q3; that could be why Norwegian deliveries are so low in October. There is no proof that production is growing a lot faster than deliveries. They can easily play that game if they wanted to to maximize deliveries each quarter. Not saying that they are, but we just don't know.�

Nov 13, 2013

FredTMC yep. I agree. My guess is TM tries to minimize the cars in transit at QTR end. I agree that deliveries (sales) is the main component the street cares about for this "growth" stock. GM is secondary. 2014 guidance would've helped support the stock price too but as we know TM decided not to issue 2014 guidance until next year. Ouch�

Nov 13, 2013

sleepyhead And this would make sense if you knew that production will grow by a very big percentage as soon as supplier constraints are resolved. Since TM expects these constraints to be resolved in about three months, and the stock was so priced so high, it only makes sense to play these games. That is probably what Elon meant when he said that the high stock price affects the way they do business (or whatever his exact words were).�

Không có nhận xét nào:

Đăng nhận xét