Aug 5, 2013

sleepyhead Disclaimer:

All views, data, trading recommendations, opinion, speculation and information found on this forum exist solely for the purpose of discussion and debate amongst the members only. TeslaMotorsClub.com makes no representations as to the accuracy, completeness, currentness, suitability, or validity of any information on this forum and will not be liable for any errors, omissions, recommendations, opinion or delays in this information or any losses, injuries, or damages arising from its display or use. All information is provided on an as-is basis. Submission of information to the forum assumes your agreement to, and understanding of these terms.

http://www.teslamotorsclub.com/announcement.php?f=119

Please find the attached financial model at the bottom of the post.

Note: All of my numbers are on a non-GAAP basis, which excludes stock-based compensation and reverses effects of lease accounting.

Q2:

5,200 cars delivered,

$568 million in revenue

$0.32 EPS

23.1% gross margin including all credit sales

FY13:

23,100 cars delivered,

$2,476 million in revenue

$1.38 EPS

24.9% gross margin including all credit sales

Analyst Consensus:

Q2:

$393 million in revenue

-$0.17 EPS

FY13:

$1,840 million in revenue

-$0.03 EPS

Highest Analyst�s Estimate:

Q2:

$478 million in revenue

-$0.05 EPS

FY13:

$2,160 million in revenue

$0.27 EPS

Q2 earnings release will be all about two items:

Demand � demand has been very strong and if you listen to Elon talk, it sounds like it is getting even stronger, �demand is not the problem, but rather supply is.� Specifically, battery production is holding Tesla back from producing even more than their current 25k � 30k annualized run rate. A new battery supply deal with Samsung will alleviate this issue. There are still many doubters that believe that demand is falling off and they will be caught by surprise on the earnings call.

Gross Margin � Will Tesla be able to achieve its 25% gross margin target by Q4? On Q3 2012 conference call, Elon mentioned that Tesla can achieve these margins with an annualized rate of 20,000 vehicles produced. At a 25,000+ run rate, Tesla should have no problems reaching this milestone. From Q1 conference call Elon said, �unless we really screwed the pooch, you'll see the 25% gross margin number in Q4.� Seems like everything is progressing a little quicker than Elon�s previous conservative guidance, which is extremely positive.

Modeling assumptions for Q2:

Vehicles Delivered � 5,200. Evidence points to 5,450 vehicles produced, so if you subtract loaners then 5,200 seems like a reasonable number.

Average Selling Price - $92,000. ASP for Q1 was just under $96k, and I expect a lower ASP in Q2 due to a higher mix of 60 kWh and 40kWh cars, partially offset by strong demand in Performance Plus models. This equates to $478m in auto sales for Q2.

GHG/CAF� credits � Same as Q1 at 3.6% of auto sales. This number is likely to increase in the near future. In June the Obama administration has increased the �social cost� of carbon emissions in federal regulations

ZEV Credits - Elon said in Q1 conference call:

"Yeah, so we�re expecting a decline in the credit revenue for Q2 and then probably fairly significant decline in Q3 and as I said back right now, we�re not expecting anything in Q4. That�s our � I mean, it might be some ZEV credit revenue in Q4, but we�re not accounting on it. I don�t have � I can�t give anymore precision than that at this time."

The expected decline in Q2 was probably due to three factors:

- 4,500 deliveries expected vs. 4,900 in Q1.

- Higher mix of 40 kWh and 60 kWh cars that generate less credits than 85 kWh models.

- Lower selling prices of credits.

Since Tesla delivered significantly more vehicles than it guided for, I don�t expect the ZEV credit revenue drop-off to be significant in Q2.

Development Services � Slight increase from $6.6m in Q1 to $10m in Q2.

Gross Margins � I used 10% gross margin on auto sales excluding any credits (I have taken out the GHG/CAF� credits as well as ZEV credits). The pure auto sales gross margin for Q1 was at 1.8%, which was a 9% increase from Q4 2012. Elon on Q1 conference call:

It's worth noting that when you see the gross margin for Q1, we're giving you obviously the gross margin average over the quarter. And so the gross margin at the end of Q1 was significantly better than at the beginning of Q1.

Average Q4 gross margin was around -7%, so let�s assume that they ended Q4/started Q1 at about -2% gross margin run rate. We can then assume that Q1 gross margin ended at around 5% - 8% range. If Tesla is to reach 25% gross margin in Q4, then my 10% Q2 gross margin number may actually be conservative. Including GHG/CAF� credits my gross margin number is 13.1%. This sounds conservative to me, but maybe I am a bit too optimistic on ZEV credits; chances are that any differences will offset.

Research and Development Expense- From Q1 shareholder letter �slight increase�, therefore I modeled a 5% increase from Q1.

Selling, General and Administrative - From Q1 shareholder letter �moderate increase�, therefore I modeled a 10% increase from Q1.

Other Income - $6m of FX gain. The Yen has continued to weaken at a similar pace to Q1 and therefore modeled in a similar number.

Weighted average shares outstanding, fully diluted �This number has increased by almost 6 million due to recent round of capital raising done in the middle of Q2; the other 6 million will kick in in Q3.

Provision for Income Taxes � This amount is very minimal at 1%. US income will still be tax free for a while due to net operating loss carryforwards from previous years. International income will still be taxed. My estimate is probably on the high side, but it is immaterial.

GAAP Earnings

Stock-based compensation - Q2 expenses under GAAP will have an additional $15million of stock-based compensation if you follow the pattern from Q1. Note that TSLA�s share price has increased significantly and might weigh on this expense category possibly leading to a number higher than $15m.

Lease Accounting � On Q1 conference call Elon said that approximately 25% of cars sold are financed through Tesla. If we assume that 40% of those vehicles are returned to Tesla after three years, then 10% of all vehicles sold will fall under the lease accounting rules.

There could have been additional one-off GAAP items as well.

On a GAAP basis, I have modeled $514 million in revenue and $0.11 EPS.

Important Notes:

Net income in my financial model is most sensitive to gross margin and ASP does not affect net income as much (but will impact revenue significantly). It is important to note that lower ASP�s will also mean lower gross margins. A 6% change in ASP changes EPS by $0.02, while a 2% increase in gross margin will change EPS by $0.07.

The wildcard here are ZEV credits. There is downside risk to this number and every $1.3m equates to $0.01 EPS. As previously mentioned I still see upside risk to gross margin and these risks could hypothetically offset each other.

Other risks in my model include higher than expected R&D or SG&A expenses and lower FX gains.

Guidance:

In Q1 Tesla announced its arrival and in Q2 it will announce that it is here to stay!

Elon�s goal is to advance the production of EV�s around the world and the sooner the better. If you have listened to his interviews, you will hear that he is not entirely convinced that it is not too late to save the planet, hence the idea to colonize Mars. Every year that goes by is one year closer to getting to the point of no return. In order to get other auto manufacturers serious about EV development, Tesla has to show them how profitable it is. Therefore, this is not the time to low-ball guidance in order to under-promise and over-deliver. This is the time to make a statement.

I think that raising guidance to at least 23,000 deliveries for the full year will be a good start. But more importantly a $1.00 EPS guidance for the full year will certainly get the attention of other auto manufacturers. Tesla has not previously guided an EPS number, but it would be prudent to do so now that they have better visibility into the next couple of quarters.

Gross margin guidance excluding ZEV credits will be in the low 20�s for Q3 and Elon will give confirmation that Tesla will achieve an average gross margin over 25% in Q4; possibly higher due to new options pricing and popularity of Performance Plus models.

Feedback:

Please let me know what you guys think about the model and help me find weaknesses in my modeling assumptions. Your input is greatly appreciated and I will try to update the model if the TMC consensus is different from what I modeled in.

Cheers,

sleepyhead�

Aug 5, 2013

aznt1217 Excellent Model. Although... you forgot one other sales driver. Clothing! jk. Let's see how close it comes in :biggrin:�

Aug 5, 2013

RationalOptimist Nice work...

Nice work, Sleepyhead. If that's close to what happens, it will be a happy week. Did European plans change? I thought 500 cars from Q2 production were reserved for Euro sales and would not generate revenue this Q.�

Aug 5, 2013

deonb I don't see a specific breakout of the composition. But I'll just ask some questions:

Firstly, did you take into account the effect of the 400 or so 40kW's that were delivered at a deep loss? Amortized over 5400 vehicles it is $750 per vehicle.

Secondly, there was a price hike (was it 3.5%?) between cars delivered in Q1 and Q2, which took effect at the end of December 2012. All cars delivered in Q1 were finalized before December 2012, so the effect of that price increase only factor into Q2 deliveries. Considered?

- - - Updated - - -

Oh yeah. Unless a boat with 500 cars sank on the way to Europe, there weren't any EU cars that were made in Q2.

Nobody in Europe has a car yet, and indications are that they were loaded on the boat in July or August. See the August newsletter over here:

http://www.teslamotorsclub.com/showthread.php/19683-Europe-Newsletter-August-2013

So if follows that all deliveries went to the U.S and Canada.�

Aug 5, 2013

sleepyhead I did not do a specific breakout of the composition, because gathering all of the data will drive you nuts and your estimate will be wrong anyway. In order to simplify I simply lowered the ASP from $96k in Q1 to $92k in Q2 and applied a 10% gross margin on pure auto sales (this was 1.8%) in Q1. I figured that the higher mix of 40 and 60 cars would be partially offset by popularity of Performance Plus as well as any price increases (including those on 21" wheels, etc.)

My model is largely driven by gross margin estimates and rightfully so, since this is what is going to drive earnings in Q2. I tried to be conservative as much as possible, but my results are blowing the analyst's results out of the water anyway. Time will tell I guess.

@RationalOptimist - There is evidence that points to Euro delivery delay until Q3, and instead Tesla sold as many cars as it could in Q2.

Edit: $750 per vehicle is less than 1% of gross margin. My guess is that on pure autos (excluding any credits) the gross margin can come in at anywhere between 7% and 15%. One thing I have learned working as an analyst is not to get caught up in the details, because you are going to be wrong anyway.

My goal here was to show that, at least in my mind, the sell-side analysts are way off in their assumptions. Therefore I posted this and would like to know if you guys see any weaknesses in this model. Why would my numbers be significantly different from Wall St.?�

Aug 5, 2013

deonb Agreed. Ok, looks reasonable.

Can't wait for Tesla to reach 17.5% GM from Autos just to go and beat Joe Peterson over the head with it*. Looks like you have that after Q2 unfortunately. What's the chances of that before?

* 17.5% GM from Autos makes Tesla profitable without any credits, whether ZEV, CAFE or T-Shirts.�

Aug 5, 2013

sleepyhead I don't have the answer to that one, but I am fairly confident that Tesla is currently producing at gross margin over 17.5%.

Elon said that once they make a change on the factory floor, it takes 6-8 weeks for those cost savings to feed into the financials. So this is my best guess (really just a guess based on my gut feeling):

Start of Q1 - running at -2% gross margin. Working 70 hours/week and paying double time above 60 hours.

Feb - March - down to 50 hours per week. Finishing Q2 at about 6% gross margin.

April - about 6-8 weeks later after implementing a change that reduced overtime significantly, so cost savings are starting to show up. Let's say 8% GM.

May - Further incremental improvements leading to 9% - 10% gross margin. Then closed the factory down for memorial day weekend for retooling.

June - Now running two shifts? and producing 550 - 600 cars/week for quarter end crunch. More cars means less fixed costs (such as manufacturing overhead) spread over to each car. So margins probably got above 15% to end q2.

Q3 - 6-8 weeks later cost savings start showing on financials so today we are probably running at 20% gross margin (plus 4% GHG/CAFE almost gets you to 25%). The recent price increases will probably bump this up a little.

In Q4 I can easily see 25% GM from Autos alone. With GHG/CAFE credits it should approach 30% after the recent price hikes.�

Aug 5, 2013

DaveT Thanks, sleepyhead. Great contribution. Here are my thoughts.

1. I think your numbers (revenue, units, earnings, expenses, GM) look fairly reasonable to me. 5200 is at the top end of my estimates because of loaners, more cars for showrooms (and test drives), and cars in transit to owners.

2. I agree if Tesla can give an EPS guidance for 2013 and forecast profit for 3rd and 4th quarters, then that will be very positive. Add to this a raised 23,000 car guidance and a profitable Q2, then we might have blowout earnings.

3. My big concern is that Tesla might have spent more in Q2 than we are expecting. Namely:

- Supercharger rollout (but this should be amortized over a number of years)

- Factory assembly personnel (this would go under auto production)

- General admin/selling at factory, stores, service centers and HQ

- Research/dev engineers

The reason being is that a Bloomberg article quoted Elon as saying that they had 3,000 employees at the factory (2,000 in assembly). I didn't believe it at first because their annual report says they have 3,000 employees as of Dec 31, 2012 across their entire company, this includes the factory, Palo Alto HQ, stores, service centers, etc. I estimate they had 2000 at the factory and 1000 across Palo Alto HQ, stores and service centers. So in a matter of just several months, Tesla grew from 3,000 total employees to 3,000 just at the Fremont factory. Now the Fremont factory also has vehicle engineering and delivery specialists there (powertrain engineering and more personnel are located at Palo Alto HQ). So, my rough estimates are they now have 3,000 in Fremont (2,000 assembly, 1,000 engineers, delivery specialists, other), several hundred at Palo Alto HQ, and at least several hundred across stores and service centers (especially because they opened a significant number of new stores and service centers in Q2. So, I'm thinking they might have 4,500 (maybe up to 5,000) employees across the company. A huge ramp up from 3,000 at year-end 2012. I was so incredulous at first, I emailed Bloomberg and they said they quoted Elon correctly. I didn't believe it, so I emailed Tesla directly and they got back to me saying that the quote was correct. And now, I've seen other Tesla employees (ie., Gilbert Passin) saying they have 3,000 employees at the Fremont factory.

Anyway, just a bit concerned that Q2 will have higher expenses with selling/general/admin and with r&d. And that this might eat into the overall profit some and Tesla will hopefully still post a profit but maybe not as high as your forecasting. Hopefully, I'm just over-concerned.�

Aug 5, 2013

FredTMC Yep, excellent contribution, Sleepyhead. I have same concern regarding #3 above. Big increases head count and new service centers and stores. Thoughts? I think your spreadsheet shows ~ 10% v Q1. I fear it may be larger.�

Aug 5, 2013

confy Sleepyhead, thanks for the post. You mentioned that your numbers were non-GAAP. What about the analyst estimates?

TIA�

Aug 5, 2013

mulder1231 Sleepyhead, did you take into account the cost of the recall? Or would that be accounted for as a one-time charge and ignored/forgiven by the analyst?�

Aug 6, 2013

CapitalistOppressor No, you are correct to be concerned. Also, folks tend to forget that Tesla promised $200m in CapEx for 2013.

- - - Updated - - -

The recall cost was small.

Even if Tesla's spokeswoman was off by an order of magnitude(unlikely, since it was just a bracket), its just not worth sweating when key pieces of the model face such gigantic uncertainty.

Sleepyhead seems to be mostly attempting to illustrate how likely it is that Tesla will handily beat the absurdly low consensus forecast, as opposed to asserting a level of precision that it simply isn't possible to achieve right now. A million dollars here or there just isn't important in that context.�

Aug 6, 2013

Buran Great posts all, this is very close to my own estimates, and I agree with your general conclusion that revenue especially will again come as a big surprise.

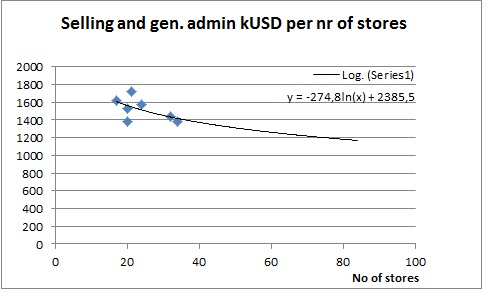

A contribution regarding issue #3, the increase in costs: In my financial model I have assumed that selling and general administrative costs is a log function of number of stores. I then get a higher increase than you do, from 47m (I assume your lower figure is non GAAP) to ~53.2m based on 39 operational stores end Q2 (all GAAP figures from Q10s). See attached graph. I think it is reasonable that they get slowly declining cost of these and hence the log in my model. In any event, I get a 13% increase Q1 to Q2, so, yes, sightly higher than your 10% estimate.

Finally, a contribution to the merchandise sales. I think this is quite a lot and really hidden in the automotive revenue. Take a typical Q of 5000 delivered. Assume 25% buy the High power wall connector (1200 USD), 10% buy winter tiers (2400 USD) 20% of all customers buys a jacket @ 100 USD, 50% a T-shirt or two or something equivalent @ some 50 USD, 10 additional people for each car sold buys something in the store without buying the car @ 25 USD, and some other assorted sales of all the cute gear for babies etc. then I get this to on the order of 5m per Q! Elon said "We sell millons" referring to apparel only. Add High power wall connector and other stuff and adapters etc for the Model S and I think this is not insignificant. Since the margin of this is likely upwards of 50% it adds on the order of 0.02 EPS in my model!�

Aug 6, 2013

NigelM Nice model sleepyhead. As it's so exhaustive/professional I felt it worth just reminding any readers of the forum disclaimer...

http://www.teslamotorsclub.com/announcement.php?f=119�

Aug 6, 2013

Norse They`ve been sold out for months!�

Aug 6, 2013

sleepyhead I took the analyst estimates from finance.yahoo.com, since I know they use non-GAAP numbers. The only difference this time around is that there will be lease accounting and it is impossible to tell if analysts are adjusting for lease numbers or not. If my estimate of 10% of cars fall under lease accounting is correct, then this will have about a $50m impact on Revenue (still puts my numbers about $40m higher than the highest estimate of all analysts). As far as net profit goes, lease accounting will only take away about $0.05/share. The bigger non-GAAP item would be stock-based compensation expense (about $0.15/share), which finance.yahoo.com does exclude.

1. I agree with you that some of my costs may be on the low side and maybe deliveries are just a tad optimistic, but at the same time you had a 14%-15% gross margin number incl. GHG/CAFE and I am using only 13.1%.

If we take away 100 deliveries down to 5100 cars then that will impact revenue by $9m, but will impact net income only by $0.02. I used an ASP of $92k that is $4k lower than Q1 due to higher mix of 40 and 60 cars. But as deonb pointed out, there was a ~$2.5k price increase that effectively started in Q2; remember also about popularity of perf. plus cars. If ASP was $94k instead then this would offset the 100 cars.

You can't subtract cars in transit, because there were cars in trans at the end of Q1 as well and these will more or less offset. There was also 100 cars delivered in Q1 buy not recognized as deliveries due to errors in paperwork.

I am fairly confident that at least 5,100 cars have been delivered assuming that the 5,454 production number is accurate. 5,200 is just my best guess, but I don't think that I will be off by more than 100 cars.

2. I really hope they do give out EPS guidance for the rest of the year. I think that Elon will give these numbers out to reward all of the loyal TSLA investors. We all know that the company will be profitable this year, so it is time to make it official to crush to rest of the shorts. Unless of course they decide on huge spending to accelarate stores, service centers, and charging infrastructure, which would be consistent with creating long-term shareholder value (at the cost of short-term).

3. I agree that costs might be higher, but let me ask you this: During what month did they open most stores and service centers? If they gradually opened these during the first 6 months of the year, then my SG&A estimate is probably close. If they opened most of them in March/April then SG&A might be a few $million more. If they opened them late in Q2, then it will have a lot smaller impact on Q2 results.

Tesla guided towards "moderate" SG&A growth in Q1 and it only went up about 3%. So I modeled 10% for "moderate" growth in Q2. Even if I model in 20% then this will only take away another $0.03 - $0.04 EPS. Anything above 20% increase is not "moderate" in my book and even 20% over the course of a quarter is stretching that definition.

As far as increase in "fremont" employees goes, I think you will be surprised how little impact this will have. I am guessing that they added 1,000 employees to run a second shift, which means that the first shift is now working only 40h/week and no more overtime. The second shift's salary is part of COGS, and since they are producing more cars there is less fixed costs/manufacturing overhead to spread over each car. I think this impact is not as big as it may first sound.

4. Even If you add another $3 - $5 million for R&D, then the company will still earn over $0.20/ share on a non-GAAP basis; and this would be my worst case scenario. Unless of course I overestimated ZEV credits significantly.

I still have a feeling that there might be upside to my gross margin number though.

Cap Op - I don't think that CapEx has any material impact on income statement, but it sure will impact Balance Sheet and Cash Flows; unfortunately I do not have enough time to model those. $200m amortized over 20 years is $10m/year or $0.02 EPS per quarter. But Tesla gets to capitalize interest expense into CapEx, so this spending might actually have a negligent impact on P&L as far as Q2 goes.

Thanks for pointing out that my main goal was to show that Tesla will handily beat the absurdly low consensus forecast. If my numbers turn out to be somewhat accurate and the stock does not jump higher, then I think that the SEC should investigate this situation. A lot of retail investors are relying on analyst estimates/recommendations, so if they got it completely wrong then the stock should continue to go up.

Buran - I agree with you that merchandise sales will be huge, especially in the future. Heck I bought an expensive $22 "future Tesla owner" onesie for my son when I walked into the store.

Could you give us some of your numbers to see how they compare to mine as well as the analysts out there? Specifically revenue, gross margins, and net income; both GAAP and non-GAAP basis.

Bottom line is that, unless I significantly overstated ZEV, Tesla should be on track to earn at worst $0.20/share even if you include the effects of lease accounting. If you add back stock-based compensation to get to a GAAP number then you are still looking at a small profit. Of course there could be one-time items that we don't know about that could be enough to push a small GAAP loss. In my mind, if I take the worst case scenario for every line item (excl. wildcard ZEV) then the company is still profitable on a non-GAAP basis.

Revenue is going to be over $500 million and that is going to come as a shock to many people. I think that gross margins will come in higher than expected, especially going forward into Q3 and Q4.

- - - Updated - - -

I edited the OP to include this disclaimer. Everything I wrote is just in the interest of spurring discussion, I do not recommend anyone to act on my numbers since following Tesla is not my full-time job and I could be wildly inaccurate in some of my assumptions.

Thanks,

sleepyhead�

Aug 6, 2013

Blurry_Eyed At Teslive, I seem to recall Jerome say that they basically doubled the service headcount in the second quarter. If that's the case, how would that impact your model?�

Aug 6, 2013

Buran Sure, here are the key bits:

I model all with the data in the income statements of the 10-Qs, and my understanding is that this is GAAP(?). I am quite unfamiliar with this as we seldom have the equivalent dual track analysis in Sweden. However, in the following I have not included the lease effect, as I think that Wall street will simply look at the figures as of they were all sales. For now. When Tesla provide better guidance, we will have to include this in the correct way.

Deliveries: 5050, think 5200 is possible, but prefer a lower estimate as there is a growing amount of cars in transit each Q since the company is expanding. There are also lags in cars entering the service system etc. and a big uncertainty of the VINs. I however believe that the VINs are not "scrambled", just messed up now with EU deliveries and continuous batching. Also, remember that Elon have said that they on occasion have had a large number of cars on hold in production, or perhaps even in body in white due to hiccups in parts delivered. I hope that in a couple of months in this will clarify and VINs will be trustworthy again.

Model S revenue: 460m based on ASP of 91700. Think the number of P85 and P85+ is high, 40s were very low, 60s are just 30% and people by ALOT of addons. The latter was a big explanatory factor to the revenue surprise in Q1.

Drivetrain: 9m, simple average of previous Qs

ZEM 56m: 20% decrease this Q, just my guestimate

GHG/Cafe: 17.6m: same per car as last Q

Merchendise exc: 5m

Total rev: 560m

Toal costs of revenue and GM. 430 with gross margin of everything 30%, it was 21% on 10-Q figures in Q1. I model 16% automotive margin in Q2, my estimate was 4% on automotive margin with GHG/CAFE included but without ZEM in Q1, and -11% in Q4 2012. I have assumed a steady growth toward target of 25% in Q4 and that means roughly 10% margin on Model S right now when the improvements have started to kick in. The rest is from the credits and merchandise. My interpretation of the credits issue is that ZEM is not counted on, but GHG/CAFE is. Exclude also GHG/CAFE and you get 12% GM on automotive.

CAPEX: Same 5% increase in R&D as you, and my 13% modeled Sales cost increase per above get me to 111m costs.

Bottom line: 16m net profit and 0.13 EPS.

Agree that a big uncertainty is actual margin on Model S. Could be more like 7-8% and that they are not on track toward 25% due to continued supply problems...�

Aug 6, 2013

sleepyhead From 10Q:

Selling, general and administrative expenses during the three months ended March 31, 2013 were $47.0 million, an increase from$30.6 million during the three months ended March 31, 2012. The $16.4 million increase in our selling, general and administrative consistedprimarily of a $7.2 million increase in employee compensation expenses related to higher sales and marketing headcount to support salesactivities worldwide and higher general and administrative headcount to support the expansion of the business, a $5.7 million increase in office,information technology and facilities-related costs to support the growth of our business, a $2.6 million increase in professional and outsideservices costs and a $0.9 million increase in stock-based compensation expense related to a larger number of outstanding equity awards due toadditional headcount and generally an increasing common stock valuation applied to new grants.We expect selling, general and administrative expenses to increase moderately for the remainder of 2013 as we continue to increaseour vehicle selling and servicing capabilities. In addition, future equity awards may result in an increase in selling, general and administrative?expenses.

I am going with a 10% increase or $4.5 million since they used the word "moderate increase". SG&A has gone up 50% over last year and if you apply 10% per quarter then you will get close to that 50% increase again. Even if I modeled in a 20% increase instead of 10%, it would only impact EPS by an additional $0.03. It is also important to know at what point in the quarter did these stores and service centers open. I highly doubt that SG&A grew by more than 20% in the quarter though. The unknowns are: ZEV, R&D, and Gross Margin.

I am more worried about the impact of higher stock price and the effect on the stock-based compensation portion of GAAP earnings, but am not exactly sure what kind of impact it will have.

�

Aug 6, 2013

justdoit What I still don't understand is why these numbers are so different from other analysts. I think the most optimistic estimate from Wall Street is a loss of 5c share. Do they have data we don't or vice versa?�

Aug 6, 2013

deonb They are counting on 500 cars delivered to Europe and not realized in Q2. They cannot discount that since that is part of the guidance and they have no prove to the contrary.

We don't really have prove either, but if there is one thing that Tesla can be relied on, it is to be late at delivering something.

�

Aug 6, 2013

sleepyhead Tesla also guided towards high teens gross margin including ZEV credits and I have 23.1% gross margin. This is a result of 5,200 cars delivered vs. 4,500 guidance as well, which leads to more 100% margin ZEV credits, thus the big increase percentage wise in gross margin.�

Aug 6, 2013

CapitalistOppressor Wall Street also assumes relatively high lease accounting impacts and low ASP's. At least the ones I have looked at.

- - - Updated - - -

In fairness that is because Tesla provided guidance anticipating strong takeup of lease financing and larger numbers of 60kWh sales.�

Aug 6, 2013

james_chen70 Sleepyhead -

Job very well done. Any +ve EPS tomorrow should be a nice surprise. Fingers crossed.

Thank you very much for sharing your research.�

Aug 6, 2013

justdoit I feel like a lot of the "good" news will be interpreted by some as "bad" news.

ZEV - Tesla still requires ZEV credits for profit and high margins. Won't be able to do it without ZEV

5,200 deliveries - Tesla purposefully delayed European shipments to improve their financials.

I wouldn't be surprised if there is an initial drop after the report followed by a strong rise.�

Aug 6, 2013

Blurry_Eyed Thanks for the great analysis, appreciate it!�

Aug 6, 2013

Bgarret When it is Blurry_Eyed responding to Sleepyhead I either feel like I'm on the "Can't Sleep" thread or I'm going to nod off at my desk.

Sleepyhead - thanks for the information. My model has 5300/$523m/.31 non-GAAP/.09 GAAP/.24c GM (including ZEV)....mine are lower based on conservative (and probably wrong) lease. I hope you are right and there are some additional guidance for 2013/2014/surprises (Partnerships, anyone - GM, Google, Diamler, Intellectual Property etc.)

Yawn....�

Aug 6, 2013

Vger Really fine contribution Sleepyhead! Thanks for writing it in English and not in Street-ese. :wink:

I think it is fairly clear that Tesla realized their mistake in trying to put all those EU cars on the boat at the end of the Q, and actively changed their mind, with the intent to boost financials in the first ER after the capital raise.

It could be argued that they should have pre-announced the impact of this, but they did not. Mid-quarter guidance revisions are so rare that I think they will easily get away with it. But clearly this is the thing that completely changes the picture, even for the bullish analysts. I think some of them raised their price targets with this in mind (DB and Dougherty), but did not adjust their estimates.

What will further drive the surprise is that a lot of the "junk press" of the Street is still reporting that analysts CUT their Q2 and full year estimates in the past month.

In the end, I trust the quality of info on TMC far more than anything in the financial press. We are not just zealots (though most of us are, to be fair), but we are just much closer to the car, the factory, the user and prospective user communities, etc. On that basis, I think the probability of a repeat of last quarter's blow out is more likely than not.

Definitely night before the big game feeling here...�

Aug 6, 2013

sleepyhead The key takeaway from my report is that this earnings call is about two things only:

1. Demand - Tesla has to show that demand is sustainable. IMO it will not only do that, but it will show that demand is actually growing and has exceeded their expectations. Anything over 20,000 US annualized demand will be a blowout, since it extrapolates to 50,000+ globally.

2. Gross margin roadmap - Tesla has to show that it is on track to achieve 25% GM excl. ZEV by Q4. I believe that they might be able to reach that number now even excl. GHG/CAFE credits.

Bonus:

3. Tesla is ramping up production to meet demand, which it is doing at a quicker pace than expected. This is a bonus one, because I think that by now everyone knows that production is ramping up very quickly.

If Tesla can show all of these three things then it will be a great earnings call. If you add a good Q2 beat on top of that, then you are talking about another blowout.

At this point the market is cautiously optimistic about Tesla and there is still plenty of room for the stock to run. Both Tesla and Netflix have about the same market cap at $15b-16b; and I challenge you to look at the financials of both companies before answering my following question:

If someone offered you to gift you one of the two companies (100% control of TSLA OR NFLX) as a birthday gift, which one would you choose? I think that this is probably the biggest no-brainer in the world.�

Aug 6, 2013

TSLAopt great way to frame the value of TSLA stock�

Aug 6, 2013

DaveT That's easy for me because I don't particularly like NFLX.

I'll be looking for 2 main things (similar to sleepyhead but just different wording):

1. Current Profit

I'm looking for profit non-GAAP, hopefully profit GAAP.

Good gross margin tracking toward 25% by year end. So, at least 13% GM w/o ZEV.

2. Guidance

Looking for them to raise guidance to 22,000... maybe 23,000.

If they can give a strong EPS for 2013 (or guide for profitable 3rd and 4th quarters), that would be awesome.�

Aug 6, 2013

brianstorms Re the 5200 and not including loaners.

It's been my impression over and over, having spoken to numerous Tesla folks, that the loaners and demo cars from stores have been selling like mad all quarter.

Does your 5200 figure take that into account?�

Aug 6, 2013

sleepyhead To be honest, I let the board consensus influence my decision to use that 5200 number. A lot of smart people here seem to think it is going to fall around 5100 or 5200.

If Tesla produced 5450 and had 100 unrecognized deliveries carried-over from Q2, that is about 5550 potential deliveries (in transit cars should offset Q1 in transit cars). Let's say 250 went to show rooms and as loaners, which leaves 5300.

These loaners are selling like mad and if I were CEO of Tesla, I would simply as many of them as possible before quarter end and replenish them first thing in Q3. Therefore, I think that a 5,400 number is a possibility but highly unlikely. Yes, this is a stupid game to play to improve your numbers, but unfortunately that is how the world works. And since Tesla is ramping up production significantly, it is not like Tesla would have to play this game for too long.

A higher stock price means more media attention, cheaper capital, free advertising etc. If I am Elon Musk and my goal is to accelerate the adoption of EV's, playing these kinds of games is a necessary evil.

Elon is going to be a living legend and I have my full faith in him. No matter what Tesla did in Q2 the results are going to be really good.�

Aug 6, 2013

Jonathan Hewitt I love when people say things can't be done because THEY can't do said things. Well, Elon is not them.

Yeah, I can't see how the results won't be really good. A couple guys at my workplace plan to buy in on TSLA after the Q2 ER on "the dip." I told them if I thought there was going to be a dip I wouldn't have bought more calls today. They looked at me like I was insane�

Aug 6, 2013

hershey101 There is so much excessive optimism in these forums and sleepyhead's great analysis made me buy a lot more today. Anyone care to weigh in on the following positions:

+2 $100 Aug '13 call @42.7

-1 $130 Sept '13 put @8.15

-1 $155 Sept '13 put @21.21

-1 $135 Jan '15 put @36.54

-1 $145 Jan '15 put @42.77

The last two seem like too far out to be any good. I have been selling puts instead of buying calls because the premiums are sooo high but if the stock tanks tomorrow I'll have to move fast to close these positions.�

Aug 6, 2013

ChrisA Nice work Sleepyhead. Like others, I also think the sequential growth in operating expenses will be much larger than 10%. Elon's comment to Jerome at Teslive was something like "I told him to deliver great service... spend as much money as needed"; and even with that, the service centers still seem to be slammed. For Q2 and for the year, I expect revenue and GM to exceed expectations, but operating expenses to be higher than expected too. My $0.02.�

Aug 6, 2013

Vger This is my feeling as well. It is REALLY hard to contain expense growth at this stage of a scale-up, and with things this Rosy. I know Elon means to, but there is good reason to feed the tiger a bit.�

Aug 6, 2013

sleepyhead How much higher do you think they are?

If they increased SG&A 17% instead of 10% then you are talking about $0.30 EPS instead of $0.32.

I still think I am being conservative on my gross margin though. Does anyone here think that gross margin on autos alone will be lower than 10%?�

Aug 6, 2013

Vger Good perspective. I think this illustrates that the impact might not be that great. They are not (and should not) be at the point where they are finessing single pennies of EPS. If their build and ship growth supports even a few cents positive profit (like last time), and gross margin growth is strong (as you rightly emphasize), I think it is still a big win, and the market will reward them... and us!�

Aug 6, 2013

AlMc Anyone know if there will be a way to catch a live feed on the Q2 report? Thanks�

Aug 6, 2013

sullitf pretty sure you just have to sign up online, check the investors page at teslamotors.com�

Aug 6, 2013

DaveT Q2 Shareholder letter will be released after close of market tomorrow (after 1pm PST).

Then, the earnings conference call is tomorrow at 2:30pm PST. You can listen in here:

Tesla - Events Presentations�

Aug 6, 2013

AlMc Excellent. Thanks Al�

Aug 6, 2013

Theshadows Call in, enter the code, give them your name and I just say "self" when they ask for company name. Then log into your trading account and watch the spikes and dips based on what Elon says and note them. You may need them later to get an idea of market sentiment around a particular topic.�

Aug 6, 2013

Jonathan Hewitt I'm going to be on the road and my android based phone doesn't do flash or Windows media player so I will have to call in!�

Aug 6, 2013

vfx Another thank you SH for the english-ease.

Late sillyness. I belive there were 800 40kWh cars (not 400) and what about store and service center construction? Just here here in LA we got Torrance and Van Nuys service centers and a Century City store. The Q before this one there was only the Topanga store opening.

The stores probably range from 250K to 2 million (the original LA store build cost) and service centers might be in the same range to outfit with diagnostic equipment and basic inventory. And there is the high end rent on the Mall sq footage and the cheaper land but larger service centers with their offsite acreage that usually includes a parking lot or garage that holds service overflow and pre-delivery vehicles.

And weren't the Superchargers we all clammer for come in at 250K each?�

Aug 7, 2013

sullitf Hopefully this isn't a horribly basic question, its been years since I took a few accounting classes.

How exactly will service centers, stores, chargers, etc. be handled in their books? It is cash spent but they are left with a depreciating asset, would only a fraction of the cost affect earnings since the cost should be amortized over the expected useful life?�

Aug 7, 2013

Warrenbonz Expenses for Supercharger expansion shouldn't be much of a factor for Q2 as it seems Tesla waited until Q3 to really begin rolling out new Superchargers in quantity.�

Aug 7, 2013

deonb Since Tesla said publically only 4% of buyers opted for the 40kWh, with 800 40kWh cars that would imply 20'000 sales before April 2013. Sweet! But no.

Superchargers are capex. Their total expense will be deprecated over several years - not at the point of construction. Same with most of the cost to build a store and service center. Agree on the high-end rent though.

- - - Updated - - -

Yes, the rule is if an asset has a useful life beyond that of the current taxable year, the cost for it must be capitalized, and the capital expenditure costs amortized over the life of the asset.

- - - Updated - - -

Just be warned - if you're used to companies like MSFT releasing their shareholder letters promptly at 1:01pm, Tesla is not one of them... In May, Tesla released it at 1:30pm.

Waiting for that shareholder letter after 1pm will feel like waiting for a SuperCharger to arrive in Fargo. Find something to do in that time or you'll drive yourself nuts.�

Aug 7, 2013

maekuz You made me look: There is a grey dot on the Supercharger map at Fargo - in 2015.�

Aug 7, 2013

AlMc Since I think I read somewhere recently that North Dakota is the second largest oil producing state, I am hoping that they don't fight TM as Texas has done. :wink:�

Aug 7, 2013

Citizen-T I believe there is a good ol' fashioned phone number you can call.�

Aug 7, 2013

vfx Right. 4% is the number Elon stated which is probably why the 800 cars number was thrown out there. Someone figured 4% of the 20,000 annual number. Could that still not be right? Was it 4% of reservations, or 4% of sold? 4% of delivered? I thought reservations made the most sense in that Tesla could see the writing on the wall.�

Aug 7, 2013

TSLAopt Any ideas on how to get that phone number? I went to the IR site but couldn't find it�

Aug 7, 2013

fjm9898 Even if its 800 cars to the 20k year then that would only be 200 this quarter.�

Aug 7, 2013

deonb All the 40s were delivered within this quarter. They weren't spread over the year.�

Aug 7, 2013

vfx Not all the 40s have been delivered. There are some stragglers.�

Aug 7, 2013

FredTMC yeah, I haven't found it yet either.�

Aug 7, 2013

Johan For earlier calls it has been:

Live Call: (877) 312-5519 / (760) 666-3771 (International)

But not sure if it will be the same for this call?�

Aug 7, 2013

maekuz Did you register here: Tesla - Events Presentations ?�

Aug 7, 2013

TSLAopt Yes and it only offers to listen via Windows Media or Adobe Flash, neither of which I can use from my iPad or iPhone unfortunately.

(there is a windows media app I downloaded on my iphone but i can't seem to even register from my iPhone, seems the mobile IR site doesn't allow that)

- - - Updated - - -

Thanks Johan, will try that later�

Aug 7, 2013

Citizen-T I don't see it right now. I'm sure it was there before. You could just call the generic investor relations number and ask them, I'm sure they will provide it.�

Aug 7, 2013

kevin99 Haha... that is a funny one. How did you guys come up with name like this?�

Aug 7, 2013

EV2BFREE "Vehicles Delivered � 5,200. Evidence points to 5,450 vehicles produced, so if you subtract loaners then 5,200 seems like a reasonable number."

At Teslive the consensus seemed to be that they were not holding onto the loaners and selling most of them. It could be to just make sure that they make a profit in Q2, who knows. I think that 250 loaners seems like a generous number.�

Aug 7, 2013

kevin99 sleepyhead, thanks for putting in the effort for the analysis!

I haven't seen anyone asked on the ZEV credit. I see the on sheet you have ~ $68m,same as Q1. I thought there will be less ZEV credit in Q2, right?

If your estimate of ZEV credit is true, then it is short's deja-vu again: Look, Tesla make profit because they have the ZEV credit!

�

Aug 7, 2013

sleepyhead Kevin - It is actually $62m vs. $68m. I figured that Elon said it would be lower this Q due to lower car sales 4500 vs. 4900, and lower selling price.

If I applied 4500 vehicles delivered then my ZEV calculation works out to $54m vs. $68. Since they delivered a lot more than guided, that raises the ZEV number to $62m. I basically used $12k of ZEV income per car delivered vs. $13.8k in Q1.

There is a real risk that this number is overstated.

Once again, I am hoping that my gross margin number is conservative and may possibly offset any decline in modeled ZEV income.�

Aug 7, 2013

Citizen-T Remember that ICE auto sales have been above expectations as well, it is possible that demand for ZEVs has stayed stronger than Tesla expected when they gave that guidance.�

Aug 7, 2013

james_chen70 Sir Sleepyhead -

You were right on!�

Aug 7, 2013

deonb No. He had $558m. Actual was $551m.

Totally unreliable :tongue:

Seriously. Congratulations!�

Aug 7, 2013

sleepyhead ZEV came in at $51m vs. my $62m. If you change those numbers I will be extremely close in my model.�

Aug 7, 2013

Johan Well done sleepy!!! Props!

(Will you do my taxes this year please?) :tongue:�

Aug 7, 2013

Adm Sleepyhead, get out! The black and whites are moving in! They finally found out who broke in to Deepak's office! :scared::wink:

Nice work sir!�

Aug 7, 2013

c041v Well done Sleepyhead. I'd like to thank you and all the others that laid out Q2 with an impressively accurate prediction.�

Aug 7, 2013

ongba Congrats sleepy on a great job!�

Aug 7, 2013

MikeC Sleepyhead, you are bad ass. I owe you a drink next time if you're ever in LA.�

Aug 7, 2013

austinEV Yeah, nicely done.�

Aug 7, 2013

Discoducky Super Kudos Sleepyhead!�

Aug 7, 2013

kevin99 Great job, sleepyhead! And kudos to folks putting in the effort, DaveT, maekuz and many others! We all learned!�

Aug 7, 2013

fjm9898 I remember wanting to choke sleepy a few days ago, now i cant remember why�

Aug 7, 2013

Goldfishes sleepyhead well done! I took a look at your model this afternoon and was excited because it was close to my estimates! Extremely far from anything seen on the street, and very accurate. The so-called "comparables" are nothing like Tesla, and the auto industry ER analysts are having a hard time modeling that out. That's why I love this company. Long from $34.�

Aug 7, 2013

marvinat0rz Wow. Dead on. Mad respect and hats off. Congratulations, and thanks for your brilliant analysis =D�

Aug 7, 2013

sleepyhead Thanks guys. I could not have put this together without the wealth of information and contributions from the members here on TMC. This truly is a special place to be.

I hope that at least one person decided to buy some shares and made some money based on my analysis. That makes all the work worthwhile.�

Aug 7, 2013

mkjayakumar I simply cannot believe that someone can do such an accurate analysis. Just 7M off of 558M. That is close to 99% accuracy.

You beat the pants off all those Wall street analysts..�

Aug 7, 2013

Sparky I did. Woke up this am and saw the drop and considered things for about 30 secs before throwing some more shares into the pot at $133.50.

Thanks for your hard work and insight.

Tomorrow's my factory tour. I will enjoy the drive up!�

Aug 7, 2013

mershaw2001 Thank you to all who participated. At the drop today, I bought all that i could based on the analysis here.�

Aug 7, 2013

twinklejet Perhaps sleepyhead, julian, curt and all the others who have put in so much effort into not only analyzing but providing and reporting their analysis for the benefit of the rest of us here can provide their paypal (yes elon's old project) email addresses or something for donations especially those who have made or will make a million or two thanks to these awesome guys! Call it a virtual beer?�

Aug 7, 2013

Norse I totally agree, but there are so many. What sold me Tesla is Sal Demir. I have also got alot of help from sleepy and Johan. Julian, Curt, CapOp and alot of others have really been helpful aswell. But yes, I will donate.

This forum is just so great. I just hope its stays this why, tho something this good, really cant last forever.�

Aug 7, 2013

Jackl1956 Julian, Curt, Sleepyhead I thank you. My kids thank you. My ex-wife (dammit) thanks you.

You guys are the best.�

Aug 7, 2013

arashlzy Thanks Sleepy, Premium Coffee on me next time you are in LA�

Aug 7, 2013

emupilot The combination of your analysis, others like it here at TMC, and all the online articles showing the cluelessness of everyone outside this forum convinced me to get more call options yesterday and today. My retirement account will benefit nicely from it tomorrow. Thank you!�

Aug 7, 2013

Mitthrawnuruodo Thanks Sleepyhead, I expect to make more money tomorrow than I did all last year. Going home shopping this weekend�

Aug 7, 2013

Mitthrawnuruodo someone on the forum predicted that after a Q2 beat the NHTSA would release its 5 star crash rating. Holy crap you were spot on!!!

http://www.teslamotorsclub.com/showthread.php/19915-NHTSA-crash-tests-videos�

Aug 7, 2013

gym7rjm Thank you sleepyhead. I made money from your analysis. If we ever cross paths... drinks on me.�

Aug 7, 2013

makinthdonuts Yeah thanks Sleepyhead, you nailed it with your analysis. Though this may be the last ER to catch Wall St. off-guard, I'm happy for everybody who got in early and enjoyed the show today.�

Aug 7, 2013

Johan Logically you should be right - this would be the last "big surprise" earnings. HOWEVER, those guys are STUPID so let's talk again as we approach Q3 call�

Aug 7, 2013

Jonathan Hewitt Huge thanks! My brokerage jacked up my account today and gave me more calls than I wanted, which now turned out to be good but thanks to everyone here (especially your numbers) I stayed cool and kept them, which should treat me well tomorrow�

Aug 7, 2013

DaveT Wow, that's awesome. Great day (of any day in the calendar year) for your brokerage to give you more calls than you wanted.�

Aug 7, 2013

kevin99 So who predicted it? Who wants to claim it?�

Aug 7, 2013

sleepyhead I just looked at Tesla's Q2 numbers and for pure auto numbers excluding any credits or development services Tesla got:

$497,347 of revenue and $430,001 in cost of revenue for a gross margin of 10.3% on pure autos, 13.5% on autos + GHG/CAFE credits, and 22% including ZEV credits.

I modeled in :

$484,000 of revenue and $430,560 in cost of revenue for a gross margin of 10.0% on pure autos, 13.1% on autos + GHG/CAFE credits, and 23.1% including ZEV credits

I overstated ZEV by $11 million, since it looks like market prices for ZEV credits are coming down, hence ZEV revenue will drop off quickly as predicted by Elon on Q1 CC.�

Aug 7, 2013

kevin99 Remarkable!

Funny things is I wasn't aware of your model until this morning after I was busying capturing the dip and putting in my bet. This forum has strict rule about not posting links or things like that. However that is how i missed it!�

Aug 7, 2013

blakegallagher That is remarkable ... nicely done.�

Aug 7, 2013

Larken I have been looking on ir.teslamotors.com for the reply from the ER but cannot find it. Does anyone have a link to the reply? Thanks and congrats everyone!:biggrin: Viva Tesla!�

Aug 7, 2013

blakegallagher If you go Tesla - Investors Overview you have to register for it. Its on the bottom right part of the page and its labeled

Tesla Motors, Inc. Second Quarter 2013 Financial Results Q&A Conference Call

Its right above the shareholder letter�

Aug 7, 2013

deonb I did.

I held up your analysis as the truth (still have that spreadsheet open from this morning!), and compared it to the article after article that came out today stating the old numbers, and when we hit $135 today, I went 'screw it':

I closed out my safety 15% put position that I planned to go into ER with, and changed everything to calls instead. Those puts would have been virtually completely lost going into tomorrow. (100, 120, 125, 130, 135, 142 Aug 9th & 17th).�

Aug 7, 2013

blakegallagher

Wow .... nicely done !!!�

Aug 8, 2013

Causalien Yeah it helped.

I had a huge vertical going in(120, 150), with only half of the upper call sold. The plan was to sell the other half nearer earnings and come out with no risk exposure at all, but I didn't do that.�

Aug 8, 2013

CapitalistOppressor This is essentially the same thing I did. Once the stock fell so much pre-earnings, I felt like my put firewall had already captured a ton of value compared to my worst case expectation post earnings. So I dumped those and put some of the profits into calls on the theory that I was prepared to write off the insurance money anyways, so why not bet it on what I really felt would be a strong report, lol�

Aug 8, 2013

sleepyhead Great job in all of your research CO, it has really been beneficial to me and everyone else on this forum.

What is your view for the next few trading days? I feel like the stock has some room to run only because:

1. It traded at $145.86 before ER, and with a good report there has to be room (theoretically) for at least 20% upside from that number.

2. A lot of weak longs cashed out and new shorts came in over the last two trading days prior to ER.

3. Institutional money might start piling in.�

Aug 8, 2013

deonb Gift to sleepyhead

What do you give to someone for a job well done?

Well, more work of course!

I have translated all the Q2 earnings report statements into an Excel spreadsheet and changed numbers to formulas where I could. Triple-checked the numbers. Should come in handy now that we know how lease accounting will work.

You're welcome to use this for any purpose. May I suggest modeling Q3

View attachment Tesla Q2 2013.xlsx�

Aug 8, 2013

destroid Thanks again guys. In addition to the great research here, some of the best info has been pointers to official Tesla info/interviews. Careful reading makes it clear that conservative guidance and great execution is going to keep this company strong for many years.

I bought a few shares during Q1 and missed most of the big run-up post Q1 before getting into options trading. So far post Q2 is going well and my Model S test drive is scheduled for the weekend. Most positions were centered around Sept 150 calls as I thought this was achievable, even with a modest Q2.

It's been a wild ride this week but sleepyhead's (and many others) spot on analysis of Q2 gave me the confidence to hold my positions and accumulate more in the face of drops like Wednesday pre Q2 earnings. Now it's time to buy more stock and LEAPs for the long game...�

Không có nhận xét nào:

Đăng nhận xét