Mar 18, 2013

luvb2b hello all. my first post here. been following this company a long time and i luv them.

i have been thinking about first quarter earnings a lot lately, esp after the last call when elon was adamant they would be profitable. until the 10k was released i couldn't make the math work. you guys have probably read the comments on seeking alpha etc talking about how there is no way tesla could make a profit. for example:

Despite Tesla's Light Results, It Could Be Turning The Corner - Seeking Alpha

the light bulb for me came on with the revelation that the various environmental credits added up to $40.9 million in 2012. using 2750 model s sales, that number works out to an insane $15k per car. considering they only earn the credits in a dozen or so states, it's even more amazing as it implies the credit value per vehicle sold in a qualifying state is probably something like $25-30k. all guesswork on my part. further research indicates that the 85kwh pack seems to qualify for maybe 50+% more credits than the 60kwh pack, although this is not clear to me as there are two types of credits at work: ghg and zev.

now a second light bulb has come on lately in reviewing the various delivery threads. we are starting to hear about vin numbers as high as 87xx getting scheduled delivery at the end of march. there are multiple reports in vin #8000s. considering the delivery numbers were 2750 last year, it seems like they must be well past their target of 4500 vehicles this quarter. is it possible they will produce 6000 cars in q1? that's what that vin number 87xx seems to indicate. i don't want to be so optimistic, so i am working with a number around 5200.

finally my last light bulb is in reading the forums about the problem reports. it seems that even though the number of model s on the road will triple this quarter vs. end of q4 2012, the number of problems are not exploding. that's consistent with what they said on the call, that the problems and issues with the car have gone down substantially. in some ways the biggest risk they face is a recall, but that might even be manageable if it was a small item (10000 cars x $2000 to fix each is still only $20m plus whatever reputational hit they take).

i am very curious what people think of my estimates as i have laid out below, if they sound realistic? also i really wonder if that delivery number could get to around 6000 the way the vin numbers are progressing. anyone have thoughts on that? every time i read about someone going to a service center sounds like they are loaded with model s's being prepped for delivery.

anyway, i run the math this way:

on revenues:

model s avg price $85000 x 5200 = $442 million (note: maybe low based on mix of p85/85/60 & options)

enviro credits $15000 x 5200 = $78 million (note: using $15k per car in credits, see above)

add development services = $5 million

total revenue = $525 million

on gross margin:

assuming they get automotive gross margin (excluding enviro credits) to +5%, which seems plausible given higher production. gross margins would be:

model s: $22.1m

enviro credits: $78m

dev services: $3m

total gross profit = $103.1 million

on operating expenses:

now figure $63m in r&d (declines from prior q as they projected) and $47m of sg&a (increase from prior q), gives you $110m in gaap expenses. take out the non-cash items, about $13m in stock based comp and $7m in depreciation and amortization... you got $90m in non-gaap expenses.

on ebitda:

implies ebitda of $13.1m, or about 11-12c per share. high estimate on the street has non-gaap eps at 2c. there's substantial upside to this if my delivery numbers end up being conservative, which based on the vin's i'm seeing is possible.

on incremental upside:

each additional 100 units would add $8.5m in revenue as follows:

revenue model s: 75000 x 100 = $7.5m (lower for 60kwh deliveries)

enviro credits: $10000 x 100 = $1m (lower for 60kwh deliveries)

assuming higher efficiency on later units, the gross margin impact of an additional 100 units may be $1.75m as follows:

10% gross margin on model s = 10% of $7.5m = $0.75m

enviro credits: $1m

total ebitda impact of additional 100 units: about 1.5c per share.

on reservations

if there's one worry i have it's here. the reservations seem to have fallen quite a bit in q1 vs. q4. it wouldn't surprise me if they got only 3k new reservations. if they ripped through 6k existing reservations, had another 1.5k cancellations, then the end of q1 reservation count will be: 15k (q4) - 6k (production) - 1.5k (cancels) + 3k (new) = 10.5k reservations remaining at the end of q1. if reservations don't pick up in q2 this will get the shorts blabbering again.

on future quarters

in light of the above, the comments on the call about future quarters start to make sense too. musk had said that the impact of enviro credits would decline, but margin would increase to compensate. so just hypothetically if you were to assume for q2:

5000 units x $82000 sale price = $410m sales plus

5000 units x $5000 enviro credits = $25m credits equals

$435 million total revenue

gross margin improve to 20% on automotive, then gross profit:

on model s: 20% x 410m = $82m plus

enviro credits: $25m equals

$107m gross profit

and once again you'd be talking about positive ebitda, maybe even 15c per share? incremental upside for each additional 100 units would be around 3c per share i'd guess.

and that's higher than the previous quarter even though the total revenues are $435m vs. $525m as estimated above.

summary

basically in summary, i am proposing that the shorts have far underestimated the value of the enviro credits, and that the production has scaled up faster than anyone expected.

thanks for your inputs.�

Mar 18, 2013

Zzzz... I read an article about Tesla supplier few days ago. That plant was producing parts at a rate of 500 per week... Do the math. If you want, I could find a link.�

Mar 18, 2013

FredTMC Great post. Thanks

couple comments.

Regarding Gross Margins. I distinctly remember from the Q4 call that the enviro credits were not part of the Gross Margin target of 25% per car. TM hopes to get to 25% GM by end of this year.

I also recall that TM was looking to have GM in "the teens" for Q1.�

Mar 18, 2013

jeff_adams I wouldn't be too worried about reservations. It seems like they are starting to ramp up in Europe and Asia. When Tesla can promise delivery to those markets, the numbers will surge�

Mar 18, 2013

c041v Excellent addition.

I have a comment regarding the average price per unit. Being somewhat ignorant of the geogrpahical breakdown of the tally, I believe it is worth noting that in Canada, the price of a fully loaded 85 kwh Performance is just over $120,000 CDN. I think even a decent 60 kwh model will run into the mid 80's. I'm not sure what the prices are like in Europe or any other country outside of the US, but given the sales split proposed by Elon, I believe it is worthwhile to perhaps consider a higher selling price, especially in future quarters. The Canadian dollar is within a few percent of parity, so it's not like the forex will account for too much of a difference.

It may also be worthwhile to consider the S derivatives that will undoubtedly boost margins with minimal expense to Tesla.�

Mar 18, 2013

hcsharp Tesla claims to have priced the Canadian version to bring in virtually the same profit as the US version.�

Mar 18, 2013

Zzzz... Yeah, difference comes mostly from an import tax and extra delivery expenses. May be Tesla's Canadian prices were priced somewhat conservatively, to make sure an extra expenses are covered, but difference would be non material, probably a grand if not less extra profit per unit.

- - - Updated - - -

I would love to see Tesla insource battery cells production, or buy cells produced in North American plant. At least for Canadian market that would mean tax free import. But realistically insourcing wount happen anytime soon. But might be that would be a good idea to do such thing for GenIII, which would be oriented on more price sensitive market... And Nissan is already manufacturing cells in US for the new Leaf.�

Mar 18, 2013

luvb2b Zzz: please post the link or that supplier article. TIA. 500 per week x 12 weeks would be 6000 units.

FredTMC: correct, accordingly I separated gross margin on automotive from the value of the credits, for example note that for my q2 rough-in I used:

gross margin improve to 20% on automotive, then gross profit:

on model s: 20% x 410m = $82m plus

enviro credits: $25m equals

$107m gross profit

I agree with the comments on CAD sales.�

Mar 19, 2013

Eberhard please remember, elon told, that the production can be ramped up to 60.000 unit/year (including Model X?) before more assembly lines have to be added, just by moving from one shift to 3 shifts and maybe working 7 days/week.�

Mar 19, 2013

luvb2b agreed that reservations in those markets should ramp. but q1 has been slow relative to q4, for example 18500 was reported in us jan 15 and 19711 on mar 3. that's less than 30 per day in the us for most of the quarter. data from the michiganmodels threads seems to point to around 3000-3500 total new reservations for q1.�

Mar 19, 2013

Zzzz... Here we go.

Key point:

That's why a part of perhaps the most advanced automobile ever made ships from Chautauqua County, 500 every week.

But even more interesting is another claim:

Jamestown Plastics' president Jay Baker disclosed Tesla wants 650 of the liners by early autumn.

From the context it looks like 650 per week by September. That seems to imply that S production in September should reach 650 units per week.:smile:

- - - Updated - - -

I contacted "news", hope GCR will write an article about this disclosure...�

Mar 19, 2013

gregincal Total reservations shown in that thread has been about 42 per day for the first two months of the year (as you say, 30 per day is US only). That would be 3800 for the quarter which is probably a minimum, so your estimate seems low. This is the slowest quarter of the year for car sales in general, though.�

Mar 19, 2013

luvb2b interesting post on yahoo finance today by temagami67. he estimated revenues as follows:

Model S 4800 units, $98k ARP = $461M.

Roadster 12 units, $140k ARP = $1.7M.

Toyota 250 units, $30k ARP = $7.5M.

ZEV+GHG 4800 units, $12k = $56.4M.

Devt Serv = $5M

Total Revenue = $531M.

compared to my estimate he's slightly higher, with lower units, lower enviro credits, and higher selling prices than i had. however the conclusion is generally the same, that revenues will beat estimates by a wide margin. the street consensus for the quarter is $465m and the high estimate is $528.4m. i'm pretty sure at some point the analysts are going to have to raise these numbers.

also saw delivery scheduled for another 87xx and a 88xx vehicle. so they must be on track to produce 6000+ cars this quarter. that's so much better than i ever imagined, and i bet the higher production rates translate to higher gross margins too.�

Mar 19, 2013

Clprenz I am quite interested in the recent pick up in production, I would be fantastic if they brought it up to 25k a year and possibly higher as Zzzz said. I also emailed the author to ask for source. I think I will be picking up some more shares in this dip!!!! Fantastic news, just waiting to hear one of Elon's Tweets that the SEC would freak out about!!

�

Mar 19, 2013

Grendal I don't think we will ever see any similar tweets from Elon, because the SEC probably gave him an earful and possibly a firm hand slap for the last one.�

Mar 20, 2013

Yuri_G Remember, even if those VINs are delivered this quarter, that doesn't necessarily mean all of the VINs before them were delivered. I would expect the number of cars delivered in Q1 to be close to the 4500 goal.�

Mar 20, 2013

JRP3 In a recent video, this one I think, Elon said they were delivering 500 cars per week.�

Mar 20, 2013

mulder1231 My buy order got filled yesterday at $35. Today looks like a move away from the $35 level, hope this trend will continue all the way to the next earnings call, as expectation/speculation starts building.�

Mar 20, 2013

avatar Hi - Does anyone know when the Q1 reports are going to be out? Even roughly?�

Mar 20, 2013

carrerascott Mid April? Based on Q4 coming out in mid February.�

Mar 20, 2013

blakegallagher Hopefully before April 20th ..... have some options that expire then ... hope to get the big upswing from report before I sell them off�

Mar 20, 2013

gregincal Actually that would be mid-May. Early May is probably a good guess, though. Last quarter was quite late.�

Mar 20, 2013

Curt Renz The last four earnings reports were released on:

2012 MAY 09

2012 JUL 25

2012 NOV 05

2013 FEB 20

On average that is nearly 38 days since the end of each quarter. So the next earnings report likely won�t be released until sometime in May.�

Mar 20, 2013

luvb2b wanted to add a quick thought on gross margin for the quarter (excluding enviro credits). read this excerpt from the last conference call:

copied from:

Tesla Motors, Inc. TSLA Q4 2012 Earnings Call Transcript

elon: For this quarter and for probably most of next quarter, you have to decide what the relative focus is and I think the important thing for us to focus on right now is production efficiency and improving gross margin rather than scaling up production... It's really important that we improve the manufacturing efficiency and kind of reduce the number of temps essentially. We still expect to see an increase in full time employees from beginning of quarter to end of quarter, but it is really important that we make some significant progress in reducing the size of the temporary labor force and addressing the manufacturing inefficiencies. In any company, you've got to focus on what's important at any one time and production efficiencies, thanks to � if we wanted to, we could raise production right now to 500 units a week, but that's probably what we could do right now, but we would do so at the expense of efficiency and would have a lot of overtime and that kind of thing. So, right now, it's really just production efficiency...

elon mentions production efficiency about 6 times in this one paragraph. it's repeated several other times during the call too. he states several times they won't scale up production until they have efficiency first. we have very strong data points indicating production is at 500 per week, thanks to the various links people have posted here and the delivery information from other threads.

i think the logical conclusion is that they must have made pretty significant progress on improving gross margin. in my model to start the thread i estimated 5% gross margin on an 85k car, and 15k in enviro credits per car. the 15k in enviro credits is possibly too high, but on the other hand the information above has me thinking the 5% gross margin estimate is probably too low. with as important as increasing margin was to them, it probably is the case that they have made substantial progress on this front. i guess i'm saying on further reflection that maybe my gross margin estimate leaves some further room for upside.

i wonder when the shorts will figure out all these pieces.

make 500 cars per week. then 6000 cars produced in the quarter. add 15k in enviro credits per vehicle. fold in gross margins skyrocketing. mix in 5 million shares newly shorted in the last month.

it's a recipe for a strawberry short-cake.�

Mar 21, 2013

Curt Renz Thank you for your fine analysis, luvb2b. I just want to note that there are 13 weeks in a quarter. Therefore, 500 cars/week x 13 weeks/quarter = 6500 cars/quarter.�

Mar 21, 2013

Zythryn Don't get your expectations out of alignment with reality.

500 cars/week now doesn't mean 500/week at the beginning of the quarter.

They also had the first week off, so that would be 0.

While I would love to hear a surprise 6000 number, I am expecting 4500. If we get more, awesome!�

Mar 21, 2013

gen3_in_utah Thanks for link. Great news.�

Mar 21, 2013

hershey101 I agree with Zythryn, historically TSLA has had a tough time hitting their goals (recall Q4 sales, production of Model X etc.) so we shouldn't be so excited about the sales figures.�

Mar 21, 2013

smorgasbord I think the credit-math needs to be redone.

A Model S is a Type III and so gets 4 ZEV credits (http://www.arb.ca.gov/msprog/levprog/cleandoc/clean_2009_my_hev_tps_12-09.pdf). Prices per credit had been around $5000, but with more and more qualifying cars coming onto the market, the law of supply and demand indicates that price per credit should decrease. So, while right now Tesla might be making as much as an additional $20K per car, that's not something they can count on moving forward.

Here's what Tesla's recent 10K says about them:So, they're not able to sell all the ZEV credits they get, but are able to sell of the GHG credits. I don't know the value of the GHG credits.�

Mar 21, 2013

luvb2b curt, as zythryn mentioned, it is not 500 cars/week for the entire quarter. my production estimate of 6000 vehicles is coming from the fact that only vin numbers up to around 3000 had been produced as of the end of q4, and now we are seeing vin numbers of 8800+. vin 88xx said delivery could be scheduled march 28th, and with production running 100 per day one could assume in the neighborhood of 6000 cars will be produced this quarter.

from a revenue standpoint there is a lag from production to delivery, i estimate around 10-14 days. meaning you should expect that of the cars produced in the quarter 1000-1400 to will not be delivered in time to book revenue. the unit estimate of 5200 i got by taking the 500 or so model s that were produced but not delivered as of the end of q4, then adding 4600-5000 that should be produced and delivered this quarter (based on my production estimate of 6000 above, subtract 1000-1400 that will be in process of delivery).

i understand people not wanting to get expectations up and be disappointed. however in prior quarters we could tell that they weren't meeting consensus production timelines by looking at vin numbers and deliveries, i think this quarter we see the opposite. i'm trying not to be optimistic, but rather assessing the available data as realistically as possible. as an investor, knowledge that there may be a revenue or earnings beat vs consensus expectation is very valuable information. that's why i feel accuracy is paramount. from the long-term standpoint of the company, i realize a few hundred units this way or that isn't going to matter much.

an aside, on this forum it seems like sometimes when i post the post doesn't show up right away? i assume because it's a moderated forum. is there any way to see my posts that are awaiting approval so i don't post twice? i guess you could pm me with the answer?�

Mar 21, 2013

avatar The tesla motors twitter account just tweeted that production was 400 cars/week.

Tesla Motors (TeslaMotors) on Twitter

Looks like we are being too optimistic.�

Mar 21, 2013

carrerascott Tesla just posted this to their Facebook page (and probably twitter):

#WattsUp: We've ramped up! The Tesla factory is now producing 400 Model S a week!Based on that, they won't have come close to 6000 in this quarter. If they had been doing 400 per week since Jan 1, there are almost 13 weeks in Q1, that would be 5200. But with the missed first week (4800) and likely haven't been doing 400/week all along if they are saying they've ramped up.. then we could be looking at closer to 4,000 for Q1. Of course the twitter/facebook account may not be accurate, so who knows.

?�

Mar 21, 2013

avatar You totally stole my thunder....�

Mar 21, 2013

carrerascott Wonder if that has anything to do with the stock going from nicely positive to negative now...

�

Mar 21, 2013

avatar Something definitely doesn't add up. In this video: Elon Musk in conversation at Tesla Motors | 18 March 2013 - YouTube

Elon CLEARLY says Tesla is delivering 500 cars per week. Tesla motors website says they are building400 cars per week. Maybe cancelation rate is higher than we all think? Why would they build at a slower place than delivery rate?�

Mar 21, 2013

Yuri_G I think it's a social media snafu. Tesla said they were producing 400 cars per week at the end of Q4 per the most recent earnings report. Tesla probably meant to reiterate what Elon said recently with 500 cars being delivered and/or produced per week.�

Mar 21, 2013

Zzzz... Wondering same thing here..�

Mar 21, 2013

avatar You are most likely correct. Tesla really needs to get a handle on its corporate communication teams. It seems like the wild west and chaos over there. Thats a pretty big typo to make.�

Mar 21, 2013

Citizen-T I've seen from two different sources (one being Elon himself in the video above) that production and/or delivery is at 500/week. I would not give as much weight to that little blurb on Twitter. It's clearly out-of-date information.�

Mar 21, 2013

Curt Renz If it is indeed a typo, then an hour has gone by without a correction.

Does anyone know who on twitter is "WattsUp"?

Tesla executives must have noticed the tumbling share price that followed the tweet. If it was in error, they may be in consultation regarding a correction. They may fear that someone could be accused of manipulating the share price for day trading profits.�

Mar 21, 2013

Clprenz Their twitter has been great and responses directly to the my question, If they could clear up the production output confusion. They responded with,"@clprenz It's often upwards of 400"�

Mar 21, 2013

avatar That is super confusing. "Updwards of 400?"�

Mar 21, 2013

ckessel *shrug*, 400, 500. It's all more than 20,000 a year. I can believe it has varied as they've ramped down temporary workers (production goes down) while working on optimization.�

Mar 21, 2013

Zzzz... No I did not: Thinking about Q1 2013 earnings - Page 2

Someone even gave me rep for posting that link

Edit: opps, nvm

PS. apparently still sleeping...�

Mar 21, 2013

FredTMC Stock fell today

mainly because the market overall went down midday (IMO)�

Mar 21, 2013

luvb2b Twitter vs. VIN mystery

i saw the tweet and also clprenz's question back at tesla, who confirmed that production is "often more than 400 units".

the vin numbers imo are the most accurate tell. as you can see below, they were very accurate for production at the end of q4. at this point you'd need a many-hundred unit skip in vin's to have even just 5000 cars produced. vin's are pointing to 5500-6000 cars produced. elon's statement and the frunk liner article are the confirming data points.

i studied this very closely for last quarter before drawing any conclusions for my model. what i found is the latest vin that was legitimately scheduled for deliver prior to 12/31/2012 was indicative of the actual number of cars produced. here's a sample of data form timdorr's spreadsheet sorted by vin's around the 12/31/2012 date. notice how cleanly this data would allow you to have predicted 3000 vehicles made in 2012? estimating this way actually underestimated the 3100 units tesla said they produced in 2012!

for vin's past 3033, i researched any that claimed a delivery date range starting in 2012. in every confirmed case the delivery date was in 2013, meaning that tesla was overly optimistic giving them a delivery date and more than likely the vehicles were not really produced.

vin# delivery start date 2924 12/30/2012 2925 12/29/2012 2940 1/10/2013 2942 1/7/2013 2943 12/15/2012 2948 12/29/2012 2970 12/28/2012 2975 12/15/2012 2991 1/5/2013 2998 1/3/2013 3010 1/8/2013 3033 12/31/2012 3059 1/11/2013 3062 1/6/2013 3072 1/9/2013 3081 1/12/2013 3082 1/6/2013 3092 1/7/2013 3094 1/10/2013

right now we have reported vins of 8700-8800s that are scheduling for delivery prior to the end of the quarter. even if there was somehow a 200 vehicle skip in vin's you'd still be at 5400-5500 units already produced this quarter because the vin's ended at 3100 or so for 2012. i don't think there's going to be that many vins skipped. the 87xx-88xx's are being scheduled for delivery as early as 3/28/13, which means you still got a couple days of production to add. i think production based on vin's is predicting 5700-5800, and then add another 200-300 for the end of the month to bring production for the quarter to near 6000.

vin delivery start date actually delivered 3157 12/15/2012 posted his car was on a truck 12/29/12 on teslamotors.com, no confirmed date 3233 12/15/2012 redsoxdoc on tmc said delivery was around 1/15/13 3319 12/15/2012 jbherman on tmc said delivery was on 1/16/13 3229 12/26/2012 arrived 1/7/13 in dallas based on teslamotors.com post 3277 12/31/2012 meursault said delivered 1/9/13

as far as deliveries, recall there were 450 cars that were produced but not delivered at the end of 2012. so you take these cars, add the production, and subtract 1000 for two weeks of production in transit... for me this gives the following table of cars produced vs. likely deliveries.

the way the numbers are i just have a hard time seeing how they could deliver less than 5000 cars this quarter. production estimates based on the vin would have to be off by more than 300 units for that happen. i guess we'll see at the next report. i placed my bets accordingly and not changing until i have strong reason to believe my estimation procedure is going to be off by hundreds of units.

if produce likely deliver 6000 5450 5800 5250 5600 5050 �

Mar 21, 2013

gregincal Thanks for that post. My VIN math had come to similar conclusions, but I didn't want to post without pulling together the evidence, which always seemed to take too much time. Your post saved me all the effort. Elon himself said when asked whether Tesla would be publishing sales figures that the best way to track sales was to look at VINs.�

Mar 21, 2013

avatar I hope this is true. But to ensure that we take a little salt with our kool aid, I'd like to state this is the most optimistic scenario for TSLA in 2013. Heck if TSLA delivers $0.15/share each quarter we won't need the shorts to drive tesla shares through the roof.�

Mar 21, 2013

Krugerrand It's well known that they have built more than they've delivered. A car doesn't come off the line and immediately become delivered in the next second. Batching for location would hold up vehicles for delivery as would any issues that had to be addressed with a car from a QC aspect. And I'm sure there are other reasons, like waiting for people to show up at the factory or at a store to pick up their cars.

It's therefore not hard to understand that on any given week they might very well deliver more than they built that week. Nowhere does it say that they've maintained the 400 built to 500 delivered ratio week after week after week after week. That could just be happening this month, or from the time Mr. Musk made his statement.�

Mar 21, 2013

clmason Per the latest Blog post "During the past three weeks we have averaged more than 500 Model S deliveries per week, and it looks like we�ll be setting another record this week."

Music to my ears!�

Mar 21, 2013

erha Sounds great, but we still don't know how many cars are being produced. I guess they have quite a bit of cars to deliver after their problems with ramping up deliveries.�

Mar 21, 2013

luvb2b well that helps a lot. now we know weeks of feb 24-mar 2, mar 3-9, mar 10-16, and mar 17-24 will total more than 2000 deliveries. i suspect the pace will stay at 500+ that last week of march, so say 2500-2600 deliveries in the last 5 weeks of this quarter.

assuming the first week of the quarter was off, then the next 7 weeks from jan 6-feb 23 averaged how many deliveries? 350 per week? 375? 400?

350 per week gets you to around 5000 units for q1 revenue purposes: 350 x 7 + 2500 to 2600 = 4950 to 5050 units.

375 gets you to around 5125-5225 revenue units for q1.

400 gets you to around 5300-5400 revenue units for q1.

i just don't see this quarter being under 5000 units. i am still going with the 5200 estimate that kicked off this thread. consensus estimates are too low.�

Mar 21, 2013

anticitizen13.7 Google Finance shows a Q1 2013 report scheduled for May 6th. Is this confirmed or just a prediction from Google?�

Mar 21, 2013

carrerascott Yea, sorry I meant mid-may. About 1.5 mos. after the quarter ends.

- - - Updated - - -

I think based on last qtr, it's a guess.�

Mar 21, 2013

Curt Renz Indeed, Google predicts May 6. However, NASDAQ and Zacks anticipate it will be released May 8. The Tesla webpage for upcoming investor events indicates nothing for now. In February, Tesla reported later than predictions found on various sites.�

Mar 24, 2013

luvb2b From Twitter:

@DeanJFalkenberg: @elonmusk Are you really producing more than 500 cars per week now?

Answer from Elon:

"Yep."

As in "Giddy-YEP!"�

Mar 24, 2013

carrerascott I wonder how much these warranty purchases are going to add to the income report for Q1. I already paid mine. I'm sure lots of others have even though they're not due for a month or so. If 1,000 owners buy the ~$4000 plan, that's and additional $4mill in Q1. Not sure if that's treated as pure income/profit or what, but surely it will help.�

Mar 24, 2013

hershey101 This was discussed previously on another thread I think. Based on my understanding, warranty/service purchases are counted as liabilities until the work is done, or the warranty period is over. So, if you are getting the 4 year service for $1,900, I think they can only count $600/yr after you have gotten your car serviced.�

Mar 25, 2013

Robert.Boston That's right -- it helps cash, but not income or profit. OTOH, getting the 3G program set up will ?help all three.�

Mar 25, 2013

hershey101 If the $30/month predictions are accurate then I think most people will choose to not get 3G.�

Mar 25, 2013

carrerascott I think most people will bite the bullet and get 3G because they don't want to lose all the cool factors (web browser/Google maps). I'm assuming it's month to month and cancelable once wifi tethering is activated.

To your friends in the car: "Yea I paid $102,000 but the $30/month was just too much, so the browsing doesn't work, the Google maps don't work, the app doesn't work, etc..."

Yes $30 is too much, if this is the price, but it's a drop in the bucket compared to the price of the car, service plans, etc...�

Mar 25, 2013

Robert.Boston Regardless of whether the sign-up rate is high or low, currently Tesla is paying the 3G charges for everyone. After the 3G program is in place, Tesla will, at a minimum, no longer be paying customers' 3G costs (except for Sigs, who get the first year free). To the extent that they are marking up the 3G pricing, they might make some profit on top of this cost-savings, but I'm thinking that Tesla will be setting the 3G rate at something close to break-even.�

Mar 28, 2013

luvb2b my research has uncovered some recent public information of moderate reliability which indicates production this quarter was 5400 units. i can't share the source unfortunately, but those who dig enough should find it.

there were 450 units produced but undelivered at the end of last quarter. so this quarter has 5850 units available to deliver. assume 700-900 are in transit. then sales should be 5000-5200 units.

$500 million revenue for the quarter clearly in play with the enviro credits.�

Mar 28, 2013

neroden I certainly won't. None of it matters to me.

Don't use it, don't use it, don't use it. Also the car only cost $80-something thousand.

There will be a fair number of us who will not pay for the 3G. Tesla, however, is stuck paying for 3G connections to our cars for service purposes. I would expect Tesla's 3G bill to remain pretty much constant, and for Tesla to simply have to eat the cost.�

Mar 29, 2013

NigelM OK, connectivity pricing/sign-up is all speculation as no pricing has been announced yet and it isn't going to affect 1Q13 earnings in any case. But for the fact that the subject can impact future financials I'm tempted to move the discussion to: 3G-Pricing-Speculation

Let's keep this thread to relevant 1Q13 earnings discussion please.�

Mar 29, 2013

luvb2b refined q1 2013 model results

using the data point i mentioned earlier and some of the other inputs on this thread i have refined my model a bit further for q1 2013 earnings:

on production and delivery:

5,400 model s produced in q1

plus 450 model s which were in delivery backlog as of 2012 q4

equals 5,850 total model s available for delivery in q1

i am modeling delivery of 5100 units, with delivery backlog of 750 units

on revenues:

model s avg price $89000 x 5100 = $454 million (updated average price slightly higher based on survey data)

enviro credits $10000 x 5100 = $51 million (lowered credits to $10k per vehicle)

add development services = $5 million

total revenue = $510 million (lowered vs my prior estimate of $525 million)

on gross margin:

assuming they get automotive gross margin excluding enviro credits to +7% (raised slightly based on known higher production levels)

model s: $31.8m

enviro credits: $51m

dev services: $3m

total gross profit = $87.8 million

on operating expenses:

now figure $63m in r&d (declines from prior q as they projected) and $47m of sg&a (increase from prior q), gives you $110m in gaap expenses. take out the non-cash items, about $13m in stock based comp and $7m in depreciation and amortization... you got $90m in non-gaap expenses.

on ebitda:

implies ebitda of $-2.2m, or about -2c per share. although no longer positive, the street has non-gaap eps at -7c. there's some upside to my numbers from better gross margin and credits. my estimate may not be comparable to the street if the non-gaap they are using excludes depreciation. i have a feeling elon will be a couple cents better than i'm forecasting, but i could only get there thru higher margin or credits.

on incremental upside:

i'm not expecting much more unit upside than this as i now feel my unit numbers are pretty well nailed down.

each extra point of gross margin adds about $5m net profit.

each additional $1000 of credits per car also adds about $5m net profit.

if credits came in at q4 levels the upside would be almost $25m and eps would be nearly 20c per share. so basically what's happened is the upside in earnings this quarter will come largely from the credits, which are tough to gauge.

on reservations

with a lot more favorable press and users getting cars in march i think new reservations could be closer to 3400. cancels likely uptick due to the large number of configuration requests and negative nyt press. i am estimating 10,700 end of quarter reservations after cancels/deliveries.

my reservations model looks like this for the rest of the year... bold/italic = forecasts

on future quarters

Prior Count Plus New Minus Sold Minus Cancels Equals End Count 2012Q3 11500 2900 250 950 13200 2012Q4 13200 6000 2400 1800 15000 2013Q1 15000 3400 5200 2500 10700 2013Q2 10700 4000 5500 1800 7400 2013Q3 7400 4500 5600 1400 4900 2013Q4 4900 5000 5600 1400 2900

in light of the above, the comments on the call about future quarters start to make sense too. musk had said that the impact of enviro credits would decline, but margin would increase to compensate. so just hypothetically if you were to assume for q2:

5500 units x $82000 sale price = $451m sales plus

5500 units x $5000 enviro credits = $27.5m credits equals

$478.5 million total revenue

gross margin improve to 15% on automotive, then gross profit:

on model s: 15% x 451m = $68m plus

enviro credits: $27.5m plus

dev services: $3m equals

$98.5m gross profit

and once again you'd be talking about positive ebitda, maybe even 7c per share? incremental upside for each additional 100 units would be around 2-3c per share i'd guess.

q3 should be very good considering average prices will likely be better due to european deliveries of higher models. i've got numbers in the range of 20-30c per share ebitda.

for now q4 shapes up to be the worst as selling prices declines, unit volumes go up, and credit impact is minimized. even so, slightly profitable ebitda.

for the year maybe 30-40c ebitda i would guess. the reservations increasing is the most important thing in the later quarters.

summary

q1 2013 estimate: 5100 units delivered, 5400 units produced, $510m revenue, $87.8m gross profit, -2c ebitda, 3400 new reservations, 10700 end of quarter reservations�

Mar 30, 2013

kenliles Q4 could be more positively impacted (on a per unit price standpoint) if Asia sales start ramping then- not sure how Tesla is modeling that market penetration, but seems like that would be about the right timing;

thanks for the great effort on the numbers.. very helpful�

Mar 30, 2013

imherkimer One item that I am curious about is revenue from selling the battery and drive train to other car manufacturers such Toyota and Mercedes Benz. I read that even these little Smart Cars I see around are now being outfitted with Tesla drives. I don't see any of this being included in your revenue calculations. Perhaps the data on this is not available or difficult to ascertain at this point. Maybe it is not even really a significant revenue source yet. Although, since MB and Toyota are both selling and/or introducing in short order vehicles equipped with Tesla electric drive tech, this will surely also become a significant revenue source over time, especially as the larger market for EVs opens. Wondering if there is any way to get a picture of this side of Tesla's business plan and partnerships.�

Mar 30, 2013

CapitalistOppressor That accords closely with the data I gathered for the blog I posted today. I didn't include March data because by its nature these self reported delivery dates suffer from a lag before they get into the spreadsheet. But when I was doing my projections earlier in the week ~2,200 March deliveries seemed likely, with initial data from the shift in the trend that happened in early March pointing to delivered VIN clusters @~8,000 by April 1st.

With ~3,000 deliveries by March 1st anything in the range of 5,200 deliveries for Q1 is likely. I'd put a non-scientific +-200 (ie. educated guess) to that number.

�

Mar 31, 2013

luvb2b i included $5m of development services revenue. none of the other vehicles seem to be selling meaningfully. if they were you could include more.

- - - Updated - - -

great blog post you had. we used the same source data to some extent so your blog helped confirm my calculations.

there are 4 sources i used to estimate production/deliveries:

1. tmc reports just like you. these point to about 5600-5800 cars produced and 5200-5400 deliveries.

2. elon video from march and tweet pointing to 500/wk deliveres and production, assuming 425/wk in other weeks and 500/wk for march gets you to 5400 cars made and delivered. 425x8 + 500x4 = 5200

3. tesla blog which confirms elon. some may consider this the same source as number 2.

4. one public source i kept secret that confirms production of 5400 units. assuming a number of vehicles in transit gets you around 5100 deliveries.

i started out with 5200 deliveries two weeks ago. think that's well within reality but decided to be a bit more conservative based on 4 above. even so, all signs point to the street estimates being handily beaten.�

Mar 31, 2013

luvb2b i have been thinking a lot about the guidance the past few days. here are the comments from cfo ahuja on the call:

"Deepak Ahuja - CFO: I think if you consider the combination of Model S sales of our powertrain sales, our development revenue and mid-teens gross margin, I think the guidance would probably lead you to somewhere along those lines close to something in the breakeven range to slightly positive, should be close to break-even. We were hoping to beat that."

i've been going over the numbers a few times, and it's very hard to make it work. but ahuja seems to indicate that yes, clearly the guidance should get you to breakeven. The biggest missing piece in the equation would be the credits. i created a table comparing the income statement in q4 with guidance and management projections for q1 (see below). i used aggressive reductions in expenses and put gross margin at the high side of mid-teens. i used $10 million for development services revenue. and i still couldn't get to positive non-gaap on my spreadsheet.

so fine, then i started taking up the average revenue per vehicle. $90k to $100k? not enough. $105k? still not positive non-gaap. average revenue per car has to be $110k to get to positive non-gaap earnings. i think there's been reasonable consensus that the average selling price is only about $90k. the implication is that the remaining $20k per vehicle is coming from credits.

i had been struggling to figure out how they could go from $15k per vehicle last year to $20k per vehicle this year in credit sales. all along i had assumed that tesla had sold credits for all 2,650 vehicles sold last year. but considering they were closing sales furiously in the last weeks of the quarter, did they have time to sell all the credits before the end of the year? for example, let's say they only sold credits for 2,100 cars produced in 2012. in that case the average credit revenue per vehicle would be $19,500 per car. yikes.

in that case they have an additional 550 credits they could sell built into they guidance for q1, on top of the 4,500 from current quarter forecasted sales. could the credits this quarter be closer to $20000 per vehicle on average? that's what the guidance seems to imply... how else can they reach $110k average revenue per car to make the guidance consistent with their statements of breakeven non-gaap?

i can't emphasize how important this question is, because if that $20,000 number is correct it will be almost $100 million contribution to revenues and gross profit with 5,000 units sold. if they could swing the automotive gross margin ex-credits positive then earnings will be... gasp! breathtaking.

any comments? maybe i will make on more revision to my model, which is currently assuming $10k in credits per vehicle. also i should note tesla's non-gaap earnings includes amortization. my q1 model was for ebitda, so there will have to be another adjustment i make there too.

Revenues 2012Q4 Guidance 2012Q4 A Auto Sales 294,377 4500 x 110k???? 495,000 B Dev Services 11,955 Assume $10 million 10,000 C=A+B Total 306,332

505,000

Cost of Sales

D Auto Sales 278,710

E Dev Services 3,765

F=D+E Total 282,475

419,150 G=F-C Gross Profit (loss) 23,857 17% of revenue 85,850

Operating Exp/Income

H R&D 68,832 lower 15% 58,507 I SG&A 45,908 down 5% 43,613 J=H+I Total 114,740

102,120 K=G-J Operating Income (90,883)

(16,270)

L Interest Income 85

- M Interest Expense (27)

(100) N Other Income 746

500 P=K+L+M+N Income before Tax (90,079)

(15,870) Q Provision for Taxes (147)

(150)

T=P-Q Net Income (89,932)

(15,720)

Reconcile to Non-GAAP

T Net Income (89,932)

(15,720) U Stock-based Comp 14,416

15,000 V Warrant Liability Chg 958

1,000 W=T+U+V Non-GAAP Income (74,558) slightly positive 280

�

Mar 31, 2013

Yuri_G I'm guessing the Q1 delivered Model S number is closer to 4500 than 5000, given the first week off in January. Also, I saw the owner of a high 7000 VIN with multi-coat red in another thread here saying he is waiting for the delivery button to appear. Once again, just because there are VINs in the 8000s being delivered does not mean that all of the VINs prior to that number have been delivered.�

Mar 31, 2013

CapitalistOppressor No it doesn't, which is why I only looked backwards to January and February so I could include the outliers.

By March 1st there had already been a solid 3,000 deliveries and the increase in delivered cars (which shadows production) was already visible and shifting the trendline. This data was with VIN's in the 6,000 range and the outliers were visible and accounted for. Those 3,000+ deliveries included 1,300+ deliveries in January (low because they took a week off) and 1,700 in February.

In early March the pace of deliveries increased relative to the previous trend, and we have anecdotal evidence that Tesla increased production to 500+ cars per week at that point. We are a month away from that data now, and the outliers are accounted for.

So there are at least three lines of evidence suggesting you are wrong. The one that you address (the inaccuracy of estimating current deliveries based on VIN number) points to 5,000+ deliveries by the end of the quarter, but is inaccurate for the reasons you state. In a few weeks the outliers in that data will resolve and it will become more reliable.

But the delivery data pointing to an acceleration in deliveries at the beginning of March is solid and the trend line it established supports the current delivery data. The 500+ car per week production rate in March is also solid. We have supplier reports from February which foreshadowed it, personal observations from folks on the factory tour reading messages congratulating the staff for the new production rate, and blog posts from Tesla itself boasting of it.

3,000+ cars were already delivered by March 1st. That is as close to a factual statement as we can make without an official announcement from Tesla. Tesla would have had another 400-500 cars being processed for delivery at that point. At a 400 unit/week production rate they would have produced another 1,600+ cars in March and ended the month with ~4,600-4,700 delivered cars and another 400-500 cars in process.

However, at the actual production rate of 500 cars (which began in late February) they would have delivered a minimum of 2,000 additional cars by the end of the quarter, with another 500+ in process.

Here is what George Blankenship wrote on March 21st -

Again, 3000+ cars were delivered by March 1st. You can see the acceleration that week, which would correspond to the first week of the three that Blankenship is referring to. He refers to another record for deliveries anticipated for the week he wrote the blog. If you do the math, Tesla would have delivered 4,500+ cars by the end of that week. They still would have had a full week still remaining in March, at a time when they are flowing 500+ deliveries per week.

Every line of evidence points strongly towards Tesla delivering more than 5,000 cars in Q1 and your concern only addresses one of those lines of evidence.

Here is one more line of evidence. Accounting for the week off in January, Tesla spent 7 weeks at a 400 unit/week rate and by the end of March would have spent another 5 weeks at a 500 unit/week rate. That is 5,300+ vehicles based on public reporting, with the only assumption being that Tesla continued at the 500 unit rate for the week following Blankenship's announcement. Because of the + in every week, I find reports of 5,400 total units in Q1 to be highly credible.

There were several hundred units in transit at the end of Q4 last year. I can see the delivery spike that they created at the beginning of January, and simple physics dictates that they existed. That is 5,600-5,800 cars available for delivery in Q1. At a minimum 500 of those will likely still be in transit at the end of the quarter, which leaves us with 5,100-5,300 cars likely to be delivered. 5,000 is a very conservative number and 4,500 just is not credible.�

Mar 31, 2013

Yuri_G

Thanks for writing the blog, I wasn't sure what you were talking about at first until I checked the blog link at the top of the page. The data points to your estimated numbers being correct. Have you done the same regression for 2012 Q4 to see if it checks out? It seemed like Tesla was going to make 2500 deliveries easily, but came up short.�

Mar 31, 2013

CapitalistOppressor Actually I did that in February when I was trying to come up with my prediction for Q4 earnings here -

TSLA Investor Discussions - Page 484

Here are the relevant passages -

Actual numbers were ~2,400/~2,650.

Honestly when I did the calculation for 2012 deliveries my numbers were very close to the final numbers. However, if you look at the graph I posted on the blog you can see that the data points in 2012 almost all looked like "outliers" because their processes were so messed up. Because the points were all so far from the implied trend I decided to give Tesla the benefit of the doubt by assuming they barely made it, only because I knew they were making a massive effort to do just that. The actual analysis showed them coming up short though, but not by a huge amount. (actually just below 2,400.. I find it interesting that Tesla reported "approximately" 2,400.. lol)

Actually, I am still very happy with my predictions in that post. I just completely forgot to factor in the ZEV credits, which pissed me off in retrospect because those were a big part of my initial research and reason why I invested so much money in July 2012. If I had utilized my own research I think i would have come close to actual Q4 revenue.

The only parts that I feel squishy on are are the cancellation rate and when Tesla would become profitable. Here is what I wrote about cancellations -

The interesting thing here is that actual experience is conforming with my predictions, but thus far Tesla denies that there have been substantial cancellations. I suspect that if there have not been cancellations, there have at least been substantial deferrals that don't count as cancellations only because they have not been refunded their money.

Hopefully we get some resolution in the next conference call, but I suspect we wont know for certain until Q3. As it is though, even with 5,000 additional deliveries Tesla has not sold enough cars to be able to turn around new orders in 6 weeks (as they are doing) unless there have either been substantial cancellations or else the majority of people on the wait list want 40kWh, standard suspension or multi-coat red.

As to profitability, I am anticipating a big quarter for revenue, and major reductions in production costs. I've never been accountant enough to translate that kind of info into GAAP/non-GAAP profits or however its booked. Certainly quite a bit of profit on operations though, ie much more actual cash coming in than going out. When you do that usually the accounting works out in the end, so I am looking forward to them reporting a profitable quarter.

One thing folks need to be aware of on ZEV credits is that there is a quota each year. With as many credits as Tesla is generating, its entirely likely that they will saturate the market and thus not be able to sell all of the notional credits that they are generating. They are right not to count on that for profitability going forward. But around 2017 the quota will rise dramatically, which is likely one reason that Tesla is delaying Gen 3 until then.

Here is the graph from the blog btw. I should mark it up with the 2012 trend and the new trend starting in March. But you can see visually that 2012 was a mess, and it got a bit messy again in February with the introduction of the 60kWh but then started to improve as their production and delivery processes dialed in. You can also see a distinct curve to the right (below trend, which indicates faster deliveries) starting around the 5,800-6,000 VIN mark and heading generally in the direction of that lone outlier on the far right.

�

�

Mar 31, 2013

mulder1231 I guess we know now and won't have to wait till next earnings report:

Tesla Motors announced today that sales of its Model S vehicle exceeded the target provided in the mid-February shareholder letter. As customers who note their Model S serial number this weekend will realize, vehicle deliveries (sales) exceeded 4,750 units vs. the 4,500 unit prior outlook.�

Mar 31, 2013

luvb2b yes, and add to that gaap profitability:

"As a result, Tesla is amending its Q1 guidance to full profitability, both GAAP and non-GAAP."

Tesla Model S Sales Exceed Target | Press Releases | Tesla Motors

this is what i predicted in my first post in this thread. estimates have to go up. can't get to gaap profits even with $500 million in revenue at 20% margins.

the highest street estimate is for 2c non-gaap. this guidance implies at least 11-12c non-gaap eps.�

Apr 1, 2013

ppl This also explains tomorrows announcement. He had to wait for this before he could announce exercising the options without claiming to reach performance goals�

Apr 1, 2013

CapitalistOppressor We still don't know the actual delivery number. Any number higher than 4,750 would satisfy this press release. Based on the language and timing of this release it makes me question whether our VIN analysis in this thread helped forced this announcement somehow.

Also clearly seems related to Tuesday's announcement by Elon. Any lawyers know if he needed to legally announce this in order to exercise his options? There were stories last week that he had run afoul of the SEC with his tweet regarding the announcement, so does this fix that? The argument is that he provided material non-public info with his tweet, so maybe making the non-public info public before his Tuesday announcement will keep him from getting fined?

Interesting tweets -

How would exercising options be arguably more important than having their first profitable quarter, and cancelling the 40kWh model? Those both seem like bigger announcements than Elon pumping ~$40 or $50 million into the company by exercising options that will make him a richer man. Those options are payment for services rendered. Will seem super odd to call his pay package more important than the company being profitable.�

Apr 1, 2013

Cattledog Seems like the link might be that the exercised options will be directly pumped into something - supercharger expansion, second production line for Model X because S sales are through the roof, etc.�

Apr 1, 2013

Citizen-T Agreed. Seems like he will exercise his options, then Tesla will announce what they are going to do with that money. To me faster roll-out of the Supercharger network doesn't amount to being more significant than profitability. WHAT DO YOU HAVE UP YOUR SLEEVE, ELON?!?!?!�

Apr 1, 2013

Yuri_G I'm sure it has been said already, but maybe fast tracked Gen III development?�

Apr 1, 2013

Citizen-T I can't imagine $50 million is enough to do that. Besides, I think battery tech is what is holding Gen III up. It isn't clear that more money would change anything there.�

Apr 1, 2013

HawaNY Quick novice question: to plow the 50 m or so from his options back into the company, how does that work? Does he have to actually sell them, or just borrow against them somehow? And it does dilute the stock by a bit either way right (although small in the big scheme of things, I understand)?�

Apr 1, 2013

Citizen-T This is not all going to be technically correct, but will give you the idea:

The options allow Elon to purchase stock that previously didn't exist at some fixed price well below the current price every else has to pay. If he buys those shares, he's effectively placing a new private investment with Tesla. That's how Tesla nets a few million dollars. Elon can then either hold those shares unto the end of the world, or he can sell them on the open market. If he sells them, then he too will make millions of dollars (because he can sell them at today's prices, not the fixed price he paid for them).

Yes, current shareholders will be diluted. This is inconsequential if the $50 million Tesla gets from the deal provides growth that it couldn't have achieved without it. In other words, we need to split the pie into more pieces, but the pie might grow a lot depending on what Tesla does with that money.

Now, where things get really interesting is if Elon exercises the options, then sells his new-found shares, then turns around and does something with that money to help Tesla. A double-whammy.�

Apr 1, 2013

30seconds just to add on to Citizen-T's post - his description is true for every company that issues stock options to employees - Google, Pfizer, Microsoft, P&G. The shareholders & board vote to create a dilutive option pool that can be earned by employees that gives them a right to buy stock at the price point set at option pool creation. This is accounted for in the financials. If the employee has earned the options (typically they are given over 3-5 years) and the trading price is in excess of the option price then the employee can buy the stock directly from the company at the option price.�

Apr 1, 2013

HawaNY Much appreciated. Right, so the $50 million or so is the amount that Tesla would get automatically, and if Elon sells them first and then uses that money for Tesla, that would be more like $250 million, I suppose. Now that's a lot of superchargers.

But he's probably not allowed to sell all just like that, right? Has to do some kind of set schedule to avoid insider trading right?

Thanks 30seconds too--really helpful.�

Apr 1, 2013

Johan Previous reported insider trades have very often been "option exercised" (i.e buy) followed directly by "sale" (on the open market). So no, I think he is allowed to.�

Apr 1, 2013

kenliles I believe these are all fully vested- He can buy and sell them all at once if he wishes; In fact, on the same trade with most brokers�

Apr 1, 2013

HawaNY OK, thanks, so Elon would have the ability to put more like $250 million into the company based on just these options, right, if he sold them right away?�

Apr 1, 2013

luvb2b wow how did this thread get sidetracked off of earnings?

i really don't think elon exercising options is a very big deal at all. you're talking about a guy who's planning a mission to mars. when he says "really exciting" it's gotta be better than exercising options. it's gonna be something very exciting from the common man's point of view imo.�

Apr 1, 2013

kenliles that's my thought too - any option conversion is a small part of the announcement if at all;

HawaNY- CitizenT on another thread is working through those numbers to see what that total might amount to- but yes, could have those kind of implications, depending on how it's done

and back OT- this may actually make Q1 earnings report one for the history record books;�

Apr 1, 2013

HawaNY How could a cash infusion, for superchargers or whatever, something on $250 million level, with minimal dilution impact (just $50 mill worth) not be a huge deal? Free money at a time when cash flow is seen as THE fundamental risk to the long term survival of the company.�

Apr 1, 2013

kenliles It would be a huge deal for the company and even the stock;

But to Elon tweet audience those things are virtually meaningless, to accomplish the goals he's set for himself and Tesla, they are just mechanism to achieve -

it may well be the vehicle by which the headline announcement is funded; but what will be done with that money IS the key excitement - otherwise it's just another cash raising...�

Apr 1, 2013

Zythryn So has anyone tried a calculation of the margins Tesla reached this quarter?

We know the number delivered, that they made some profit both GAAP and non-GAAP.

If we assume a minimal profit, what can we figure out?�

Apr 1, 2013

CapitalistOppressor Here is my current analysis on the 4,750+ sales announced for Q1, starting with the relevant section of my last post on the matter -

Umm yeah, not so much...

They don't appear to have hit 5,000, but there are additional factors to consider. The math, and GeorgeB's blog still point to them having delivered 4,500 cars, with one week to go in the quarter. Two items -

The week ended with Easter.

Tesla knew they were going to report an excellent quarter, and so might have had reason to pull a page from the Silicon Valley playbook and slow down deliveries in the final week so they could have a head start on the next quarter. Microsoft and many other tech companies are notorious for modulating sales to game quarterly expectations in this way.

Either way, I look forward to the VIN data over the next few weeks to see how March actually sorted out. I still do not see how there could have been fewer than 3,000 sales by March 1st. 2,750 just does not fit the VIN data at all unless Tesla has reserved hundreds of VIN's for company use.�

Apr 1, 2013

HawaNY HawaNY- CitizenT on another thread is working through those numbers to see what that total might amount to- but yes, could have those kind of implications, depending on how it's done

and back OT- this may actually make Q1 earnings report one for the history record books;[/QUOTE]

Thanks, so many investment threads, hard to know where to invest! I'll try to find it. Sorry if i too off track. Anyway well know tomorrow. Should be fun.�

Apr 2, 2013

ppl Thanks, so many investment threads, hard to know where to invest! I'll try to find it. Sorry if i too off track. Anyway well know tomorrow. Should be fun.[/QUOTE]

Nobody mentioning cost side. They pay for batteries with yen. Yen down 30% will signicantly reduce cost elevating margin�

Apr 2, 2013

mulder1231 Hilarious 7 min discussion Tesla's Revved Up Sales: Bloomberg West (4/1) on how on earth Tesla could be profitable in Q1.

You can see the disbelieve on their faces, especially Cory Johnson.

One speculation I hadn't heard earlier was the idea that large number of the 15,000 Model S reservations were from shorts, putting down the fully refundable $5K without intention to ever buy the car. Interesting plot, but what good would that do them?�

Apr 2, 2013

Doug_G Ah, nothing like a good conspiracy theory. The problem with conspiracies involving thousands of people is only 10% of people can keep their mouths shut.�

Apr 2, 2013

scriptacus According to Cory Johnson, all Model S now cost $100,000+ because there is no 40kw option. Also according to Cory Johnson they were only able to make 367 cars per week. The last Tesla related thing I saw from him was him questioning their ability to sell 20k/yr by implying that the 5k sold last year was a demand issue, not a supply issue.

Stellar research from him, once again.�

Apr 2, 2013

Citizen-T Oh, and don't forget that they are giving away the Supercharger option for free to incentivize people to buy the car. This is why it is so easy to make money in TSLA. The people we are trading with have bad information. Works for me.�

Apr 4, 2013

ppl Anyone considering dropping yen into cost calculation on earnings. They pay for battery in yen that has already been devalued by 30 % compared to US dollar. Today bank of japan announced even more aggressive policy to devalue yen (of course will not see that effect till 2 nod or 3 qtrs. ) but the initial 30% will show up I'm 1 qtr. battery a major cost of materials for the car�

Apr 4, 2013

Robert.Boston The question is whether Tesla agreed on a fixed battery price in yen or dollars. My guess would be dollars; o/w, Tesla would have had a huge F/X risk. Even if they had fixed the price in yen, they should have entered into a currency hedge to remove that F/X risk. So, in any case, I don't expect that they are getting much upside from the yen devaluation in the short run. It certainly could help reset pricing in the next round of contract negotiations, though.�

Apr 4, 2013

Clprenz Q1 estimate

Just to peep in, I ran multiple scenarios and I came up with a EPS of .1 to .17 . thanks to Tesla for telling us that they are profitable on a GAAP basis and have delivered 4750 cars, you can only have two other factors. The price for each emission credit they are selling and what profit margin they have reached. For my estimated that they spent 113 million, 55 million in general and 58 million in R&D. I think that the most probable case is 16% margin and 10,000 per car. Which out to EPS of .05, with total revenue of 491 million. And a aprox. profit of 6,304,000

We could also see an even better scenario of 12,000 per car in credits which brings up the EPS to .13!

These estimates are all using Cold hard facts that on average each person add 12,000 on each car.

My production estimates are as following :

900 60�s

2300 85�s

1550 P85�s

Any thoughts? or opinions�

Apr 4, 2013

DrJohnM Thank you for the analysis.

Just one question that you could help me with... You have USD55m expenses for General but I would assume that the majority of that would be factored into your margin calculation. I assume that the margin is the (unit sold price) - (the unit cost to produce). Should I assume that the unit cost to produce should include all inputs, such as materials, energy and labour? If so, General should just be the bit that is not producing cars or in R&D. Is it overstated?�

Apr 4, 2013

ppl 2011 filing of their contract has the entry of currency paid redacted. So only insiders no this (no I am not with the high command). However it also has clause that with 60 day notice either party can exit agreement so they could renegotiate this at anytime�

Apr 4, 2013

mlascano So what happened with Elon's options? Were they exercised? Would we get an SEC filling alert if so?

I'm assuming no one knows for certain but there was so much speculation around prior to Tuesday's announcement...�

Apr 5, 2013

Soundart

Luv, I appreciate you sharing your analysis. I'm just curious how you've adjusted your model given Teslas sales info earlier in the week. Are you able to reconcile to their sales/profitability figures?... And do their figures contradict that of your unrevealed source?

Apologies if you've already addressed this, but I didn'tfind it.

Thanks.

P.s. First time poster, long time telsa fan (both car and stock).�

Apr 5, 2013

luvb2b i need more clarity on whether the doe warrant liability is being reversed. some analyst reports say it is. once i figure that out then i can post an update. my unrevealed public source is only production, not sales.

sales of 4750 seems a bit low to me. it would imply 1100 vehicles in transit based on my production estimate of 5400.�

Apr 5, 2013

Mnlevin This is all very interesting, and sounds like there is alot of "inside knowledge" here. My question is WHY did the CFO strike and SELL his options on April 1??? Did he need the money? Does he think the price will fall?? is he not a long term believer in the company?�

Apr 5, 2013

JRP3 It seems that some at Tesla are taking very small salaries and using the stock as income.�

Apr 5, 2013

Nicu.Mihalache This was a date set one year in advance (Automatic Sell - Tesla Motors, Inc. (TSLA) Insider Trading Activity (SEC Form 4) - NASDAQ.com).

So the real question is why a press release with new guidance few weeks before the earnings release?�

Apr 5, 2013

aznt1217 You do realize you are insinuating illegal activity lol. Like the post after said it was set in advance. Announcement came at end of Q1, where Elon believes it's a turning point for the company. They just want to garner even more demand so they can ramp up production even more and gauge the market even more for the next year.�

Apr 5, 2013

vgrinshpun I remember hearing from Tesla Manufacturing VP (Gilbert Passin) that maximum capacity for the Model S platform "line" is 100,000 units per year. This dove-tails with Elon mentioning 500 cars/week production during the Q4 2012 call. 500 cars/week --> 25,000 cars/year (one shift). This would correspond to 75,000 cars/years for a three shift operation, increasing to 105,000 cars years for the operation in three shift, seven days a week.�

Apr 5, 2013

Curt Renz Only about 20% of the factory space is currently being utilized.�

Apr 5, 2013

kenliles true and that's a great resource to have for future; but I think the issue at hand is what production could be accomplished under the same CapX (no more lines). I'm not sure 500/week is just one shift though. Is that a known?�

Apr 5, 2013

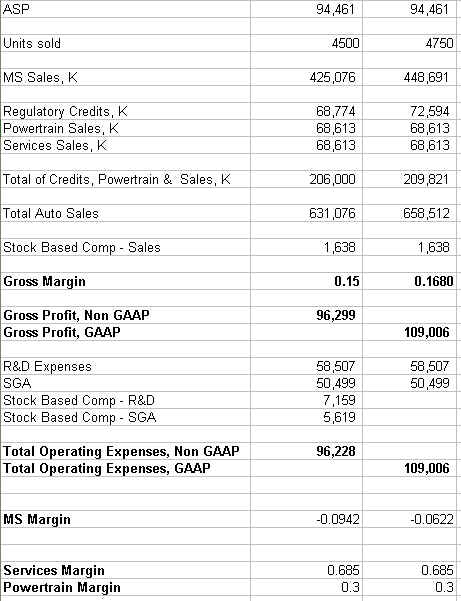

vgrinshpun I am trying to determine what was the Model S Q1 margin. I've put sizable portion of my resources in TSLA because I believe in their great potential, but somewhat concerned that they are yet not able to make money on Model S.

The analysis below is based on Tesla�s original Q1 2013 projection made during the Q4 2012 call and in the corresponding letter to the shareholders: break even on non-GAAP basis with mid-teens gross margin (assumed 15%) on a volume of 4,500 cars. It also uses Tesla revised Q1 results released on April 1: breaking even on the volume of 4,750 cars, GAAP basis.

According to these calculations the original Q1 projection was based on -9.4% margin. Using revised projection yields improved gross margin (16.8% vs 15%) and improved, though still negative, Model S margin of -6.2%. Note that original projection seemed to be using essentially the same margin as Q4 2012.

During the Q4 2012 call Elon was emphatic that Tesla will meet or beat internal goal of 25% margin on Model S without considering the regulatory credits. It is hard to understand how the margin could improve from -6.2% to 25% assuming that Tesla was already able to eliminate most of the manufacturing inefficiencies during Q1. Could it be that Tesla will realize step improvement in battery cell pricing once production increases into the second half of the year?

Any thoughts on the analysis?

Assumptions:

Regulatory credits per car � same as Q4 2012

Total for Credits, Power Train & Sales � as required to break even on non GAAP basis (4,500 cars)

Power Train Sales = Services Sales

Stock Based Compensation � same as Q4 2012

Services Margin - same as Q4 2012

Power Train Margin = 0.3

- - - Updated - - -

Based on what Elon said during the Q4 2012 call the 500/week is a one shift output. This also matches the goal of under 5 min for final assembly time per car that was mentioned in the National Geographic mega-factories video.�

Apr 5, 2013

30seconds I can think of a number of factors that would improve margins in Q2/3 over Q1

1. Volume based purchase discounts that continue to kick in at different levels

2. Reduced need of rework at factory line as improvements made

3. Reduced need of rework by rangers / service centers as improvements made

4. Falling battery costs

5. No 40kWH pack to produce

6. Higher price points than anticipated�

Apr 5, 2013

luvb2b wow you're going to find this is way off the truth. the services and powertrain sales are not going to be $68 million dollars each for the quarter. so your revenues are going to be off by probably at least $120 million (you're way high).

also there's a few shortcuts you seem to be taking trying to work through to get to the bottom line figures that are probably making things harder than they should be. if you look back through my posts i had a table of their income statement projection with formulas on the left hand side. i would suggest following that template with your own numbers, because that will at least get you matching up line item-to-line item with what tesla's report will look like.�

Không có nhận xét nào:

Đăng nhận xét