1/1/2015

guest More on Solarcity valuation:

GTM Research: Distributed Energy Resources Will Soon Receive Locational Valuation | Greentech Media�

1/1/2015

guest I looked at SCTY and peer companies like SPWR. I liked SCTY's focus on rooftop deployment and power purchase agreements, because I believe that distributed generation and a more decentralized grid is the way the electricity industry is going. SPWR and others still have a lot of resources devoted to utility-scale solar farms. Finally, SolarCity has a good relationship with Tesla (for obvious reasons -- Elon is the chairman of SolarCity's board), and I'm guessing that this will give SolarCity an advantage with integrating storage solutions like PowerPack and PowerWall.

The one thing that gives me pause about SCTY is the financial side of it. I spent a lot of time trying to understand the different and sometimes convoluted ways that SolarCity formed tax partnerships with financial institutions. This was much more complicated than understanding Tesla or most any other company I've looked at.

In the end, it's a leap of faith. I started investing in TSLA before the first Model S rolled off the production line, and the outlook was so uncertain that the company could have cratered at any time before May of 2013 (1st quarterly profit announced). I had no idea if Tesla would make it. SolarCity seems to be past the "survival" phase, but I'm thinking it may be 5-10 years before we see how well its unorthodox business model shakes out.�

1/1/2015

guest US Supreme Court Rules in Favor of Demand Response | Greentech Media

This is also good info. Note that things like the virtual power plant using Powerpacks in hotels was possible in SoCal was possible because California has it's own non-interstate ISO. Now FERC Order 745 opens this sort of thing up nationally.

This change really is a big deal. The Electrical Power Supply Association fought Order 745 because they knew it would open up a level of competion that would eat into their profits. I have long maintained that power generation is an industry headed for a glut of capacity in which no one makes enough money to survive. Blocking Order 745 was key to protecting this industry.

So what happens as generation becomes an unprofitable business to be in? Well utilities need to get out of power generation or suffer capital destruction. Utilities need to move toward an network and service model. The better job they can do of helping prosumers trade surplus power, capacity, storage, etc. to one another the more valuable the network becomes to participants.

It's going to take some of these yokels longer to figure this out. For example, NV Energy's plan to build a $900M gas peaker is monumentally dumb in light of the recent SCOTUS ruling. For example, DR programs in other neighboring states can start to undermine the value of a peaker in Nevada. This is an interstate issue, not a Nevada issue. So the Nevada PUC cannot protect them from out of state competition.

Try to grasp what this means. Suppose the wholesale price spikes up to $6/kWh in a multistage market. Utilities in one state may have set up really effective aggregation programs with their customers and as an aggregator they are entitled to some portion of the proceed. So thsee pro-DER utilities call up power from their customers that then sells this into all the surrounding states. So these utilities get to share $6/kWh mostly exporting into the other states. Meanwhile all the other utilities are paying through the nose for power at $6/kWh selling it to their ratepayers for $0.15/kWh. And guess what a state like Nevada has folks with solar and batteries that are not interconnected. So these folk are just charging their own batteries while NV Energy is losing almost $6 on every kWh they sell. These kinds of events happen a couple of times per year.

The implication here is that utilities that do a good job of cultivating and aggregating DERs among their own customers have resources that they can export into interstate wholesale power markets. The utilities that figure this out first will have an edge over the rest.�

1/1/2015

guest Got to just mention Solarcity has seemed to have raised $450mln in past month or so to little or no fanfare by the market.

Also, now the casinos are starting to sue the Nevada PUC because of mystifying reason for exorbitant exit fees. If the casinos are against you in Nevada, PUC/NV Energy are looking to good with the people of Nevada. Bet that solar referendum hits 55k in the next 1-2months now.�

1/1/2015

guest Germany says solar and wind have won technology race : Renew Economy�

1/1/2015

guest Wynn Las Vegas files lawsuit over fee to leave NV Energy - Las Vegas Sun News

�

1/1/2015

guest 1.2-million sq. ft. solar panel 'Gigafactory' in Buffalo almost ready

Had not realized the buffalo plant could be bumped to 5GW. Sick.�

1/1/2015

guest Buffalo Niagara has lowest December jobless rate in 9 years - Business - The Buffalo News

�

1/1/2015

guest German energy minister states (basically): "Game over - wind and solar wins":

Germany says solar and wind have won technology race : Renew Economy�

1/1/2015

guest Solar and Wind Could Be the Dominant Source of Power in the US by 2030

Here is an interesting study that shows how extreme use of HVDC power lines could integrate 78% wind and solar into the US power grid by 2030 without use of batteries. It's an interesting technical scenario, but it seems to take for granted the cost of so much transmission. We see Europe moving in this sort of direction where heavy use of long distance power lines balances out the grid so that high levels of renewables can be integrated without much use of batteries. But there is a fundamental problem here. The cost of transmission lines is not likely to decline that much over time, while batteries are declining some 7% over time. So if you work out a levelized cost of transmission for say a 1000 km line and compare that to the levelize cost of storage to obviate bidirectional transmission eventually batteries are cheaper than trading power regional. So by the time this proposed scenario could be built out it could already be economically obsolete.

Does anyone have estimates on the cost of HVDC power lines, maintenance, and energy losses. I'd like to do a little modeling.�

1/1/2015

guest Of course the Germans aren't interested in caps at peak, they're going to be 200% solar at peak before you know it. All those deals they pushed through to link the European grids are going to pay huge dividends when German utilities are selling their neighbors all their peak supply at a huge premium with no fuel cost!

The next phase of solar in Germany will almost be more interesting than the initial rooftop rollout. How does their open electricity marketplace end up functioning? How much economic advantage does Germany reap by being first to market with massive excess wholesale solar at peak?�

1/1/2015

guest jhm and others here eloquently laid out the case for the impeding generation glut and how NG (and other) peaker plants will soon be stranded assets. Well guess what, the Germans did these calculations years ago and acted accordingly politically and policy wise. This even as they are not and optimal country for solar (too far north, too much clouds). 5-10 years ago all other countries in Europe were laughing at Germany's "ridiculously expensive" investments in solar and wind. We'll see who gets the last laugh...�

1/1/2015

guest Agreed, and this is very much like my point about pro-DER utilities in a FERC Order 745 market. Proactive utilities have an opportunity to build up distributed solar on a low capital basis and export it to the wholesale market capturing value well beyond their service area.

So Germany is already doing this. Last year they had EUR 2 B net export of electricity to the rest of Europe. Critics have tried to dismiss this energy trade saying that Germany is effectively using the rest of Europe to balance their grid. This is the claim that you need alot of fossil generation capacity to balance intermittent renewables. But this is ridiculous from the economic view point. German is exporting higher value power than it is importing. The next export in euros proves that they are actually doing more to relieve their neighbors of the cost of balancing their grids than the other way around.

Thinking more about Order 745, I think this dies have implications for NEM. Consider that a utility wants to argue that solar feed-in rates should only be compensated at wholesale prices and moves to dismantle NEM in their state. Very well, they are opening the door to FERC regulation of the inter-state wholesale market. Could one argue that all solar power that solar customers generate, not just the surplus exported to the grid, is in fact demand response, and under Order 745 must be compensated at the real time wholesale price? So at anytime the solar customer is generating solar power or discharging stored energy for self-consumption while wholesale prices, the customer is entitled to the excess of wholesale to retail, and when exporting surplus is entitled to the wholesale price. I think such an arrangement could create pretty substantial value for customers with solar and batteries, perhaps higher compensation than under NEM. FERC has set a basic standard to assure that DR is not undercompensated below the wholesale price. So it is incumbent on utilities to demonstrate that they are cheating their customers who participate in DR. NEM probably avoids this scrutiny because it is a transaction of local energy that does not impact wholesale prices. But once the utility tries to offer something else that is supposedly based on wholesale prices, it seems they have just opened the door to FERC oversight.�

1/1/2015

guest Is there absolutely no way for the DoE to weigh in on FiT's and net metering? Can they force the hand of state regulators by setting some kind of variable minimum of net metering as a percentage of some other price/cost?�

1/1/2015

guest Whats Coming Net Metering 2.0 Decision | Greentech Media

California timeline for Solarcity mass market solar+storage is now becoming more apparent.

retail net metering will be retained through 2019. At the same time, Over the same 3 year period California will establish distributed resources(solar+storage,etc) first priority on any grid infrastructure investments given equal or more benefit with fossil fuels. They will also establish the value of distributed resources(solar+storage) to the grid.

by 2020, this new system will be codified and Solarcity will operate within the interoperability standards across the industry mandated by California utility commission. The same interopersbility standards of which Solarcity itself is establishing right now in 2016. Having 1/3 of entire distributed solar market has it distinct advantages in proliferating this standard across a wide array of assets in an effiecent timeframe.

so, as such, I expect the stock to jump Each time more pricing of services becomes available. Then we investors and interested investors can apply these revenue streams across the gigawatts of installed capacity and determine a somewhat clearer outlook post 2020.

As I've stated before, I expect it to demonstrate solarcity's significantly undervalued stock price. However by the time this becomes this clearly obvious, the stock price will not be where it is today.�

1/1/2015

guest I'm not sure. The Supreme Court's dissenting opinion, written by justice Scalia I believe, spelled out the arguments against Federal incursion on the states' abilities to be the arbiters of such regulation. So once you veer away from the effects that clearly are interstate ones, you fairly quickly get back to states' rights issues, and the questions you raise sound to me at first glance too specific to be considered national in nature. Happy to be shown wrong.

On edit: I probably should have written "...not only the dissenters...but the majority opinion as well took into consideration..." etc.�

1/1/2015

guest FERC explicitly stated NEM is retail and not under its jurisdiction.

Wholesale markets are explicitly under its jurisdiction and confirmed as such by Supreme Court decision.

States jurisdiction is retail. Feds jurisdiction is wholesale.

How this relates to Solarcity is that they will begin offering wholesale market services from consumer solar which traditionally falls under NEM, retail markets. Solarcity is able to now migrate into the Fed jurisdiction confirmed by Supreme Court, which makes ever more difficult for utilities to block/slowdown Solarcity,etc...

consider the implications of the value of Solarcity grid services now... Solarcity now can potentially march into any wholesale market across the country and there is nothing the utilties can do about it. If Solarcity successfully migrated from state NEM to federal wholesale business model, they have essentially kicked open the entire 50 state Union for business and there is nothing outside overturning a Supreme Court decision anyone can do about it. Talk about mitigating regulatory risk... This obliterates it...�

1/1/2015

guest Two questions:

That was my understanding of net metering, defined literally as compensation at the retail level(rate). So how the hell is the NV PUC allowed to create a net metering rate that does not exist on the retail side? Perhaps that's the essence of the legal issue. I always just assumed the new 3 cent rate was simply ridiculous, but still legal.

I made this comment on another board, is it accurate? (LOL.....perhaps I should be checking accuracy before spouting off)�

1/1/2015

guest I think since the Nevada PUC decision is still relatively recent, a lot of legal questions are being examined by all parties just as we discuss this ourselves right now. We haven't heard the end of what violations/problems the PUC decision has manifested, so it's just a matter of seeing responses unfold now.

ive said this before, Solarcity is already working on a business model beyond net metering and seems to be setting up and working with a policy framework it has intimate knowledge of. In essence, they are not adjusting to the system, the system is adjusting to them... they are reengineering a new game of which they'll be playing within. To understand this, only further supports the undervalued nature of its stock right now. Again, when this becomes explicitly obvious, you will never see stock prices we're seeing right now again...�

1/1/2015

guest This is why I focus on install cost, particularly customer acquisition cost, and don't get concerned when people point to all that heavy cost out on the edge. They're into some crazy stuff that takes a lot of money to develop, but the payback is simply astronomical if this is executed properly. Another reason I was fine with a post-ITC shakeout and subsequent marketshare lead increase, I think it would have helped SCTY consolidate their frontrunner position in solar.

Finding the point where the wider investing public is convinced of this model is going to be more complex that I thought, but the roadblocks are being removed almost daily. I'll just stick with "soon" as my official time horizon.�

1/1/2015

guest Right. NEM is safe for the utility that wants to avoid FERC scrutiny on feed-in tariff, but when they step out of that safe place, watch out. Solar and battery owners can take their case to FERC if they believe their utility not giving them full wholesale compensation.

Additionally, when SolarCity is selling grid services in the wholesale market, it becomes a power producers among the rest. Other IPPs operate solar and storage assets, so I see no room for distinction. The distinction between centralized and distributed energy assets would seem immaterial. It's the ability to put MWs of power into the grid at will that matters. I am speaking at a practical and market impact level. The legal distinctions will be thoroughly challenged. But from a practical viewpoint, if you've got your hand on the lever for charging or discharging 100 MW of batteries, you can seriously impact wholesale markets. It matters not how spread out your fleet is.�

1/1/2015

guest The single biggest concern with Solarcity is regulatory risk. That's it. The fundamental premise of solar and energy storage developing into a superior technology to fossil fuel is undeniable. In a market with 1% penetration, Solarcity is explicitly in a position to grow significantly over many years to come. The only thing that is slowing this process unnaturally is regulatory risk. Eliminate much of the reflgulatory risk and the stock goes bat****.

What Solarcity is doing right now in California, Hawaii, and New York is specifically aimed at reducing that risk associated with NEM and much of the traditional state energy politics. Like orange is the new black, wholesale is the new net metering business model.

Also aquisitiion costs dramatically drop with less regulatory risk. Less risk leads to greater capital investment. Capital investment leads to greater scale. Scale leads to more referrals, etc.. Also, changing the permitting and inspection process also is a massive boon for referrals. Solarcity said if the permitting/inspection process was streamlined (like Germany),they could meet a customer, design the system, install the system, and have it turned on within a day. Imagine what would things would like when this is the case? California is already moving in that direction with regard to permitting...�

1/1/2015

guest So if NV Energy pays you 3c/kWh while it sells power into the wholesale market at 9c/kWh, they are effectively selling your energy in the wholesale market but are not providing fair compensation. This is not fair to you, and it is not fair to all other power producers who are being undercut in the wholesale market. Clearly, FERC needs to safeguard against such exploitation. This may go beyond the details of Order 745, but it is in keeping with the Court's view of FERC's authority to regulate the wholesale market. When utilities exploit retail customers to undercut the wholesale market, this is a problem.�

1/1/2015

guest You must be new around here.�

1/1/2015

guest I'm in touch with my excellent local installer on a weekly basis just shooting the **** and they consider SCTY the enemy. The potential benefit solar has for nonsolar utility customers and the benefit SCTY's efforts will have for local installer nationwide needs to be articulated better. We're all on the same team here and there's enough marketshare for to last everyone for decades before we move on to storage or the next thing. What we need to do is get out message straight.

I'm really excited to see how Pennsylvania can drift down the path that NY has taken now that we have such an amazing governor. Out state legislature is a hot mess, but there's plenty of things he can do to tip the scales. It will only take a handful of larger states setting up a decent regulatory climate for SCTY to take off and solar momentum to reach unstoppable. So hard to tell when that will be.

NY, CA, PA, MA, OR, WA, TX, NC, NJ, MD, Florida(?), VA(?) Once there's stability in a handful of those states it's game over. Now that TSLA and SCTY have had this experience in Nevada, they're more prepared with a list of legislative "must haves" when picking sites for the next gigafactories.�

1/1/2015

guest The thing is with Solarcity leading taking on all these battles, the local installer also wins. A rising tide lifts all ships. Ask a competitor to Tiger woods(in his prime) if they liked competing against him they would say no. But they would say they love him under their breath because that second place paycheck was massive, and thst in addition to the benefits from 20 million people that saw him win second place. Before tiger woods, golfing as a profession made a fraction of what it does after. This is no different here.

So, installers competing with Solarcity may not enjoy losing to Solarcity in marketshare, but never, ever have they had so much business because of them at the same time. The industry before Solarcity was but a fraction of what is today and what will be every day after.�

1/1/2015

guest California public utilities commission decision tomorrow now published:

http://docs.cpuc.ca.gov/PublishedDocs/Published/G000/M158/K060/158060623.pdf

looks like vote will happen tomorrow, no utiltiy alternative accepted.�

1/1/2015

guest Could I kindly ask for an ELI5?�

1/1/2015

guest Revised Proposed Decision on NEM 2.0 Just Released

looks like solar won and utilties lost. California appears good to go for rooftop solar growth.�

1/1/2015

guest SolarCity Promotes Radford Small to Executive Vice President, Global Capital Markets

did solarcity securitize my solar loans for $185mln or $200mln as this announcement claims?

if so, must have had high demand/oversubscribed again.

also, California will grandfather for 20 years, so looking good for future securitizations coming down the pike soon.�

1/1/2015

guest Love Radford Small being in charge of financing. He needs to be the investor relations face of the company too, but that's a separate complaint.....

California utilities seem pissed, that is a good sign.

California solar advocacy group says "This proposed decision rejects utilities' bad math on solar and stands with consumers.". That may very well be true, but does not highlight the benefits of solar to nonsolar rate payers. That continues to be a big hindrance to wider acceptance of reality. Get off the back foot and express solar's true value to everyone. Not doing so reinforces the "solar vs nonsolar" resentment that the utils are trying to cultivate.

Good day.

- - - Updated - - -

Have not read yet, but wanted to post that Bloomberg is starting to dig deeper. I mean....they spent the time and effort to make this nice gif, that's a good sign.

Who Owns the Sun?

�

1/1/2015

guest Live webcast of today's meeting in California: Admin Monitor - California - California Public Utilities Commission�

1/1/2015

guest Passed 3-2.

better then expected decision. This stands until 2019.

stock should rise�

1/1/2015

guest yay!�

1/1/2015

guest Laugh out loud I logged in just in time for the vote it passed 3 to 2, was it basically the prosolar plan that I submitted yesterday�

1/1/2015

guest Yes, it is. The testimonies were good and all pro solar.�

1/1/2015

guest Summary of California's decision by Vote Solar:

Today saw a major victory for solar choice in San Francisco. After many months of deliberation, the California Public Utilities Commission (CPUC) voted to adopt new rules that uphold net metering for future solar customers of the state�s large investor-owned utilities (IOUs). The decision, put forward by CPUC President Michael Picker and approved by the Commission in a 3-2 vote, represents a balanced path forward that will support consumer savings, local jobs, healthier communities and climate progress.

As any of you regular Vote Solar blog readers will know by now, understanding how solar�s benefits and costs fit into our changing electricity system is complex and groundbreaking stuff. Today�s decision was the result of a thorough Commission-led stakeholder process from the state that knows solar best, our nation�s largest rooftop solar market by a long shot, and we hope other states will take note.

Here are some key elements of the decision:

The decision doesn�t keep everything as it was under California�s current net metering program. Instead, it makes a few compromise changes that will apply to customers under the new IOU net metering program:

- Rejects demand charges, fixed charges and standby charges proposed by the utilities and the Office of Ratepayer Advocates that would apply only to solar customers, and finds that none are reasonable or cost-justified.

- Upholds net metering for customers who go solar in 2016 and beyond. That means future solar customers who send excess clean energy back to the grid to be sold to their neighbors will continue to receive a kWh-for-kWh credit for that energy (though they will also pay some new charges on those exports too� see below for info on new non-bypassable charges).

- Ensures that customers who go solar under the new net metering tariff can stay on that tariff for 20 years from the date their solar array is interconnected � which is key for reducing customer uncertainty around future policy changes. The Commission will review the net metering rules again in 2019, but any changes would not apply to customers who have already gone solar before that date.

- For the first time, extends eligibility for the new net metering tariff to customer-sited facilities larger than one megawatt in size, so long as the customer pays all interconnection and distribution system upgrade fees.

- Removes a utility-imposed roadblock to virtual net metering in multi-tenant buildings, requiring that the utilities� virtual net metering tariffs must allow one solar array to serve multiple service delivery points in multi-tenant buildings.

- Establishes a Phase 2 of the proceeding to develop new policies to expand solar access for residential customers in disadvantaged communities.

There are ways we think this decision could have been even stronger, but all in all the CPUC has provided a solid foundation for keeping rooftop solar growing in California. In doing so, the CPUC has stood strong against intense pressure from the state�s three powerful utilities � PG&E, SCE and SDG&E � which have attacked net metering for years and in the last few weeks even mounted a last-ditch, inside-outside campaign to weaken the Commission�s strong proposed decision. The CPUC also chose a markedly different path from Nevada�s Public Utilities Commission, whose recent decision to weaken Nevada�s net metering program has resulted in the loss of hundreds of local jobs and significant new costs for residents and small businesses that go solar.

- Requires solar customers to pay non-bypassable charges on all the energy they consume from the grid, regardless of how much clean energy they export back to the grid. We consider it reasonable that solar customers contribute in this way to public purpose programs, like energy efficiency rebates and rate subsidies for low-income residential customers. These new charges are expected to add approximately 2-3 cents per kilowatt hour for energy exported back to the grid, equivalent to about $6-8/month for an average residential solar customer. (The Commission removed two categories of charges from the list included in the December proposed decision, following clean energy advocates� argument that rooftop solar reduces the need for new transmission and new large-scale power plants.)

- Puts a small interconnection fee in place to ensure that customers cover the costs to the utility of plugging into the grid, another reasonable compromise. The amount of the fee may only include the following Commission-approved utility costs: Net Metering Processing and Administrative Costs, Distribution Engineering Costs, and Metering Installation/Inspection and Commissioning Costs.

- Requires all residential customers who go solar under the new net metering tariff to take service on a time-of-use (TOU) rate schedule, meaning rooftop solar generation will be credited more during times of peak electricity system need. (Note: current NEM customers will be able to stay on their rate design plans) We commend the Commission for moving towards TOU rates, which if properly designed empower customers to respond to price signals, and which demand charges or other fixed charges largely fail to do. Vote Solar will work with the Commission to help shape future TOU rates that are fair for solar customers, and we will strongly advocate for programs that begin to shift load, with the help of demand response, storage and other innovations, to the hours when solar produces most energy.

Instead, the Commission stood with hundreds of social justice, faith, environmental, business, labor and health groups, schools and local elected leaders, as well as with California ratepayers from all across the state, who late last year delivered more than 150,000 petitions in favor of protecting net metering and expanding solar access � by far the most public input the CPUC has ever received on any issue. In recent months, major newspapers including the LA Times, San Francisco Chronicle and the San Jose Mercury News have all editorialized in favor of upholding net metering and continuing the state�s push on solar progress. Last weekend, rock legends Bob Weir, Sammy Hagar and Michael Franti joined the campaign, hosting a pop-up performance celebrating California sunshine that ended with a march to the CPUC steps in support of net metering.

So the list of those to thank for today�s historic solar victory is inspiringly long. It starts with forward-thinking Commissioners and staff at the CPUC as well as Governor Brown, whose vision of leading the world in clean energy and climate progress this decision helps achieve. It includes all the clean energy and public interest advocates who worked tirelessly in the Commission proceeding to build the case for keeping rooftop solar affordable and expanding access to more Californians, and the many more community leaders for whom this was the first time they�d participated in a CPUC proceeding. But we couldn�t have achieved this victory without the hundreds of thousands of ordinary Californians that heard what was happening and spoke up for solar. Today�s vote really was a win for all of us � our communities, our state and our planet. Thank you!

Comment by me, Gene: California would have been a better environment than Nevada for Tesla's Gigafactory �

�

1/1/2015

guest Can someone suggest good, broad solar ETFs?

I have absolutely no doubt whatsoever in my mind that solar will come to dominate world energy and do so more quickly than many people expect. However, I don't know exactly how the solar landscape will look in 15 or 20 years and would like to rely on my understanding of the physics and engineering advantage of solar in general rather than my limited understanding of the business advantages of individual solar companies over each other.�

1/1/2015

guest The one I know is TAN. Holdings here: Fund Details - Exchange Traded Funds | Guggenheim Investments - Investment Management for Financial Professionals

�

1/1/2015

guest I don't know exactly how ETFs are managed and manipulated day to day, but it's hard to simply bet on an industry since many individual players will go busto even as a handful of others go on to rule the world. Think of picking out Chevrolet from the thousands of US car companies at the turn of the century, not an easy task.

I have heard that SCTY has a major position in most solar ETFs. I think the biggest one has SCTY at 5-10% or something like that.�

1/1/2015

guest Yes, I've just been looking. SCTY is 9% of KWT. I understand your point, but with an ETF you can cope with a few of the companies going to 0 as others will pick up the slack as long as the overall pie keep growing. And as new entrants enter the market the ETF is likely to include them in its portfolio. It saves me having to pay attention to each entrant and make the decision of whether I want to invest or not, I just average out. As long as the pie keeps growing, the ETF should keep growing.

Of course you'll never get the returns that you'd get if you picked out the winner that has a 40% market share 15 years from now, but that's not what I'm after.�

1/1/2015

guest Wouldn't you want to shift to a time-of-use rate platform if you have a decent solar array? You'd be kicking out the most juice at peak hours and would be compensated more, no?�

1/1/2015

guest I have solar and I have TOU. It works for me as I charge my car at night. The only cases I can think of where TOU is a bad choice is where someone needs to run A/C or a pool filter during the daytime.�

1/1/2015

guest BREAKING: California regulators preserve retail rate net metering in 3-2 vote | Utility Dive

"The new solar net metering program will begin in 2017, or as soon as net metering caps are reached in each utility service territory."

This is a key point we must all take explicit notice.

caps will be met over the next 2-3 quarters, and probably will accelerate sooner because of the selling point of getting the net metering rates before the switch.

with that being said, expect stronger then already strong demand as a result.

again, I'm not sure if Solarcity will change its 40% compounded growth target, but I'm sure they will increase install projections now over the next few quarters. It's safe to say they will have strong q2/q3 booking/install numbers at least in my opinion.

Overall, I expect strong guidance at the q4 conference call on FEB 8th. It's pretty much a no brainier with this news out of California. There are still GW+ of installs to go under current caps. Lots of room for eager consumers to get in under old NEM for Solarcity.

20 year grandfathering a massive incentive alone.

�

1/1/2015

guest In related news, I wouldn't be surprised if SEC got wind of insider trading by Jim Chanos on Solarcity. He clearly had prior knowledge in the lead up to the NV PUC decision. His comments on subprime and customers defaulting just 2 months prior(during which the case was in the PUCs hands for decision) would be clear enough start for investigation alone.

He also stated he wished he could short more just before the decision came out as well.

where there is smoke there is fire as they say... It would be very interesting a massive case like that on chanos would do to his hedge fund fortune...�

1/1/2015

guest Why would you say it's clear he had insider knowledge? Is there some specific circumstances, statements or such that suggests that? Couldn't it just be he was betting on the Nevada vote going the other way, based on his knowledge of the politics and people involved?�

1/1/2015

guest I have solar, and use PG&E EV time of use plan. It's the best choice even with my pool pump and heavy A/C use (fresno). The only thing I actually schedule around TOU is car charging, which I do overnight.�

1/1/2015

guest No, because non-grandfathering was not even a part of the discussion between rooftop and NV Energy. It was purely a PUC decision that came as a big surprise to rooftop solar industry when it was announced on December 22nd.

The only way people would default on their leases is if keeping the solar system would cost them more then if it wasn't on their roof. That is the case in Nevada right now, so it is essentially made Solarcity a sub prime lender.

These are the exact reasons chanos made a big short bet. The only market where this timing was possible was in Nevada. His short was perfectly placed right when the NV PUC was making its decision early September and was then set to give a decision by the end of December, by which they did. That time period where he established his short position.

he was tipped off in my opinion and I also think others(involved in the proceedings)made a lot of money with him(or attempted to make a lot of money).�

1/1/2015

guest There's nothing stopping you from running your pool pump overnight, especially in winter. Even in the summertime, when I'm using my pool solar heater, I'll only run 2-3 hours during the day and the rest overnight. Easy to schedule, and it's about 1/4 the cost.. something to think about.�

1/1/2015

guest SolarCity Statement on California Net Metering Decision -- SAN MATEO, Calif., Jan. 28, 2016 /PRNewswire/ --

solarcity stating its time to install as fast as they can in this new "paradigm shift."

Does this mean greater then 40% compounded growth is back on?

"Paradigm shift" s definately a statement solar+storage and aggregation is happening in a big way. No looking back.

It is definately going to be an interesting q4 conference call.�

1/1/2015

guest From a cost perspective that would be smart. If you talk to pool people they will tell you that filtering the water in the dark isn't very productive--biologically there's much more need for filtering during sunlight hours.�

1/1/2015

guest The Tesla Powerwall is finally rolling out. First stop: Australia

first powerwall up and running in Australia. Reported as having Massive massive demand for it there as well.

I expect the same is happening here is the US and that signals Solarcity is looking to have incredible demand as well.

The signals are clear in my opinion. Solar+powerwall has commenced ramp up.

This may also indicate we should start getting solar+storage updates from Solarcity. Will be looking for this at q4 conference call. Again, I feel guidance is going to be the star of the call for this and many other reasons.�

1/1/2015

guest That's a good point. I haven't had chlorination issues (even with my salt generator), but I also have my pool covered when not in use. When it's in use, the pump's always on. But if for some reason you don't have a pool cover, you'd at least need to supplement during the day.

Still, in winter there's little excuse for daytime pumps. Depending on where you live, if it ever freezes your freeze guard comes on. That's extra pump time. So if you already run your pump overnight, you're cutting that extra energy usage as well.

Thanks for the clarity either way. I'd forgotten about "naked" pools, and that's an important distinction. Um.. SolarCity. (just trying to stay on topic)�

1/1/2015

guest I have to think Nevada backing off de-grandfathering and headed toward a full voter ballot smackdown plus this California net metering decision would be enough to send this stock to the stratosphere. Is no one doing the math? Is it not clear enough that these grandfathered PPA contracts have inherent value and will have almost no defaults? SCTY needs a net retained value clock somewhere on it's investor relations page.�

1/1/2015

guest Garnaut – time to write down value of power grids : Renew Economy

Wow, I feel like I stepped into an alternate universe reading this. If utilities don't write down their grid asset, they push the economy into even greater inefficiencies. I love the blunt economic framing here.

California and Nevada is the tale of two states. CPUC has chosen a path that will support the entire economy of the state, while NPUC has chosen a path that adds friction to economic advancement. Is it too much to expect that a PUC consider the total impact of policies on the state economy. Industrial firms like Tesla and Switch could flourish in Nevada, especially as they are allowed to make full use of the solar, wind and geothermal resources of the state, but NPUC is willing to compromise that by seeking to protect the profits of utilities in the state. California, on the other hand, is willing to harness the economic potential of renewable energy, which will be a boost to every business that has chosen to operate in the state.�

1/1/2015

guest At this point I'm thinking $50 was the short squeeze we were expecting (those shorts covered and new ones entered the game). So one way to look at it is the market was valuing SCTY at mid 20's before ITC extension, and mid-30's after. Another way to look at it is market was valuing SCTY at $50 after ITC but China, oil and Nevada knocked it down to 30's. There's also interest rates rise somewhere in there, which seems important. Now we have very favorable California and federal demand response decisions that barely moved the stock. So that would mean market doesn't think the last round of positives is of much value compared to last round of negatives. Eventually SCTY will show the money or at least show the path and force price action, but if we're assuming market got some modicum of rationality in it it's all said and done for now.�

1/1/2015

guest /disagree, the market has to be spoon feed and solar city has been radio silent on all of this�

1/1/2015

guest The market will only trend up on scty. But, I think cautious until solar+storage value is understood. The instant those numbers are understood, investors will flood in.

key points in this valuation:

sunspec aggregation/interoperability pilot preliminary results this year at some point, most likely late 2016.

APS solar+storage pilot preliminary results by the end of 2016

New York value of solar determination late 2016

Kuai utiltiy solar+storage system turned on by approximately q3.

Sales of solar+ storage officially apart of quarterly reports.�

1/1/2015

guest I'm starting to think it's still solar in general that is the problem. Well educated progressive friends of mine still regurgitate the disinformation of "unfair cost shifts" when I mention Nevada. They read one article on the topic and assume the worst. This is why I feel let down my the SCTY PR team.

It'll pass though. By the end of this summer everyone will know. One would think.�

1/1/2015

guest Great article, thanks!

Question:

So in this article, Garnaut says:

So is he saying they need to discontinue the rate increases that happen every year due to this technology shift? If so, what happens to the people who have a PPA and in year 12 their rate is higher than the utilities due to the esculator? That wouldn't be good......

I love this:

�

1/1/2015

guest Most other solars are up today. Might SCTY be struggling simply because of the efforts of the shorts?�

1/1/2015

guest Cramer said sell scty, buy fslr at some point in the past 24 hours.

on another note, California decision yesterday has set up a big solar+storage market. The time of use rates scream powerwall purchase. As will any states that develop time of use.

This time of use rate plan will effect all rate payers down the line, so all the more incentive to get solar+storage for non solar rate payers.

The early adopters this year understand buying Solarcity solar with powerwall has far more value then currently available. They understand it will be an over the air upgrade for when the wholesale market opens up. At that point, not only can they use the battery to mitigate time of use rates, they also share 50/50 with Solarcity in a demand response contract with the utiltiy. The savings from both could really drive down that $/kWh much great then solar alone (or being a non solar rate payer in general). In addition, greater reliability occurs because if the grid in general goes down you can island and run off storage.

Also, services may increase as more value is monetized as Solarcity develops more functionality over time. Again, nothing more than an over the air update.

The moment people experience this, it will create a convert/advocate for life. And that's a massive tailwind for reducing acquisition costs as referrals will be through the roof(and referrals are damn good already).�

1/1/2015

guest As I understand his argument, he is saying that the transmission network was over built for current level of utilization. Shareholder and perhaps the government need to bear the cost of this over spending on unneeded capacity. BAU is the recover the cost of this bad investment from ratepayers. Even though this can be done legally, the economic problem is that ratepayers have alternatives in solar and batteries. The attempt to collect on the is bad investment is inducing customers to get solar and even go off grid. These investments that customers are making further impair the value of network investments. So if network operators persist with BAU the future write downs will be even more severe. They are actively destroying value with their current rate plans.

The alternative is to write down the bad investments now. Set new rates that accurately reflect the marginal cost of supplying power in real time. This would both lower power bills and make customers more sensitive to consumption behaviors that truly drive the cost of infrastructure. That is, peak consumption is what drives the capacity requirements for the network. So when customers pay more for using the network at times of peak consumption, they are in fact paying for the capacity requirement they are imposing. So how this helps is that it avoid an artificial inducement for customers to use solar and batteries just to avoid paying retail rates that are well above market value so as to recover costs on bad investments. With better rates solar may still be induced because it offsets peak demands on the network, but customers with batteries will not be induced to charge their batteries at peak demand times just to avoid buy power at times of low demand. And no one is induced to leave the grid. All of this leads to making economically optimal use of the network, which supports the long term value of the network and minimizes the need for further write downs.

Suppose Wal-Mart accidentally spent way too much building out a new store. Maybe the contractor screwed up or something. So Wal-Mart decides it will simply add an extra $2 to every shoppers purchase to recover the cost of the overage in building costs. Would that work? Hell, no. All it would do is drive away customer and make the building nearly worthless. Wal-Mart would never do this. They would write down their loss on the building (and capture a tax break doing so) and sell their goods at their everyday low prices. This way they maximize net income at this store even though the had to take a capital loss.

This sort of thing is so fundamental to any business that operates in a competitive market place. And economics explains why this is so Utilities are a gross exception. They act as if basic economic theory need not apply to them. So they are actually destroying economic value, but as long as they are propped up by a political system investors are happy. Eventually, however, the political support will unravel and investors will lose big time. So the challenge is for management to have the integrity and will to do the right thing to preserve the longterm value of the business. Yet management is caught in a classic over valuation trap, which induces them to perpetuate value destroying practices.

I'm not worried about PPAs on solar systems. Things will get much worse for ratepayers before utilities are even able to match PPA rates, much less beat them. Consider in Australia an utility that charges 25c/kWh and makes only 10% profit. So their bloated cost structure is at 22.5c/kWh. How are they going to cut that cost structure in half? Write-downs help, but it is a very slow process of cutting all the fat. Additionally, in Australia most solar is owned not leased. In either case pay back is very fast when the utility is charging 25c/kWh. Even under a PPA, one would easily get full payback long before the utilities can offer a fair price.�

1/1/2015

guest cost plus system incentivizes high costs. 10% return on high cost is much better then 10% on low costs.

thsts why Solarcity is advocating for utilities to get paid on procuring other people's infrastructure(like solarcity's network of rooftop solar+storage).

on that line, Solarcity is going to start making two separate revenue streams from each install they do. They will collect a monthly payment from the customer AND a monthly payment from the utility demand response contract. So, each solarcity install maybe worth multiple times what they are worth today.

I think if you just think about that for a few minutes, one might really understand the magnitude of how undervalued solarcity(and tesla) really are right now...�

1/1/2015

guest I see. Thanks for the explanation.�

1/1/2015

guest Just look at Germany. They are doing everything they can to protect all ratepayers at retail(far more than US regulators will), and their retail rates continue to drift upward even as wholesale costs absolutely plummet because of renewables. It takes a looooong time to "work off" these short sighted investments such as the totally unnecessary new $1B NV Energy peaker plant. It is physically impossible for retail grid prices to do anything better than drift upward for the next 10-15 years, unless there's a gov't bailout or something moronic like that. I guess we shouldn't discount that possibility in this country.�

1/1/2015

guest Short interest is way down as of Jan 15th, but we can hope I guess.�

1/1/2015

guest That's right, cost plus 10% profit motivates unnecessary cost.

How about this? Simply fix the profit per kWh sold. For example, 2c/kWh for renewable energy and 1c/kWh for nonrenewable energy. This allows the utility to maximize profit by switching to 100% renewable energy while reducing costs to motivate higher consumption. Regarding distributed solar and batteries, solar feed-in power adds a cent profit for practically no incremental cost, and tapping aggregated batteries to offset fossil peakers also improves profitability. Generally the utility is motivated to minimize prices to increase volume, this can only be done by improving the utilization of network assets. Demand response mechanisms are properly encouraged because they smooth out utilization from peek to valley.

So right now utilities make about 1.5c/kWh profit. So under my plan they would need to move to 50% renewable to get back to that. This could be phased, say the nonrenewable profit rate starts at 1.4 and shrinks down to 1.0 over 20 years. This would push utilities to 50% renewable by 2035 just to maintain their profit, but in actuality I think utilities would move much more quickly than that. I think we could get to 90% re enables by 2035 under this plant. What about inflation? Have a provision that the 2c for renewables can be indexed to inflation once, 90% renewables have been achieved. So again this would reinforce moving quickly to renewables.�

1/1/2015

guest Isn't the current pattern the definition of a pennant? Brushing up against the upper bound preparing for a breakout?�

1/1/2015

guest This is pretty much what my statement was, they'll either have to show the money or tell a story that'll make investors change their mind about the valuation vs. current. I hope they'll have enough time before ER to crunch the numbers given the new California and Fed decision news and update the guidance based on that.

- - - Updated - - -

this I'm looking forward to, seems might happen earlier than expected in CA that moved well beyond basic net metering. We'll get to see if SCTY really has a superior integrated solution including the control software/cloud computing part, and will be able to establish/influence the standards. They also seem to be quite willing to go into various partnerships so I'm exited to see if/how quickly can this become a driver for wide adoption of true home automation. Before it was just a matter of cool factor/convenience, now folks will see an actual monetary value (via power bill) of having their fridge and AC unit being connected to an intelligent control system.�

1/1/2015

guest Who owns the sun? - Moneyweb

Here is a fascinating article about Nevada situation with amazing new info given out from Lyndon Rive.

Sandavol was completely emotionally involved and paranoid the rooftop solar was out to smear him from the start of 2015 when the whole legislative process happened. He also had his two long time friends, both nv energy lobbyist in his ear constantly like lady Macbeth. Obviously, he was not neutral like he says he is... add more lies to the evidence now.

Also interesting to note that the legislation originally planned to be voted on proposed lifting the cap to 10%, but then was taken out and new anti net metering language put in. What changed this movement early in 2015 process? From there it just went down hill.

also Solarcity came to Nevada before buffet boought nv energy a few months after.

Lots of interesting stuff in here...

- - - Updated - - -

Solarcity is the one to provide the data by which all else will be judged/monetized industry wide. many of these hedge funds don't get that fact. When Solarcity says it's experiencing 99.9% transfers of all leases to new owners, it's based on actual real world data, not hypothesis as they work from. When Solarcity says they receive 99.4% of all payments on time since 2006, that's hard fact from actual business transactions, not theories they conjure from academic studies.

and it's no different with powerwall energy storage integration and grid services. Solarcity has firsthand knowledge (and only at this depth and scale) of how this really works in the real world. If they are hinting that this his a massive advantage and adds another revenue stream to the company, then everyone ought to listen. It's the same for tesla as well.

its boggling to me that so much credence is being given to fund managers thst have no idea whatsoever is actually happening in the real world of distributed solar. But in the end, which I feel will start this year and become painfully apparent over the next two years, everyone of them will lose a lot of money or get out of short position before they do. Ultimately, they love money so in order to make any of it they will take a long position at some point in there.�

1/1/2015

guest http://www.solarcity.com/sites/default/files/SolarCity%20White%20Paper%20-%20Integrated%20Distribution%20Planning_final.pdf

Now with California net metering set, here is the current phase of what the net metering decision sets up. Solarcity is, at this very moment proving out this next phase(outlined above). My feeling is California will sign off on as soon as some supporting data comes out soon. That will be a monumental moment to say the least, because all of the number crunching will happen and the capital markets will go nuts wanting to be apart of its development. Abs, tax equity, facilities, bonds, etc...

Energy Storage QA with New COO Chris Beitel - SimpliPhi PowerSimpliPhi Power

Great insight into energy storage market in this interview... another interesting development is silevo's Chris beitel has taken a COO job with an energy storage start-up. Elon has stated he's always on the look out for new tech and getting into business with those that meet tesla criteria. He said currently a couple are a 3 out of 5 on his scale, which means tesla should be in preliminary talks.

Im wondering if Chris beitel' start up is on that list if preliminary talks? Since beitel is an insider to Solarcity/silevo, does he see a big opportunity to sell to tesla(maybe Solarcity) just as he did with his silevo start up? Could this potentially be a pre selected acquisition target if all works as planned?

listening to the interview, Chris sure sounds exactly like Elon and the Rive bros when describing a scalable technology(as well as the important aspects of a commercially viable energy storage product). Exactly how he approached silevo and we all know how that turned out....�

1/1/2015

guest Minor point on spelling: ISTM that is Sil-Evo, not silveo. Makes more sense that way?�

1/1/2015

guest Love/hate relationship with iPhone autocorrect...�

1/1/2015

guest

Did you mean: Autocorrupt? ;-)�

1/1/2015

guest Swarms of workers turning SolarCity into complex panel factory - Strictly Business

�

1/1/2015

guest An Op-Ed in the NYT about the Nevada bait-and-switch.�

1/1/2015

guest Best piece to date and was almost enough to get me to actually pay for NYT's online content. I'd still like to see someone clearly and with actual figures illustrate how these real dollars are being shifted from the citizens of Nevada to Berkshire shareholders. I mean, it's got to be in billions from 2014 through 2016.

These nonsense rules will be overturned within the calendar year no doubt, but what about the economic impact to Nevada? Not to mention the ~$2-3B profit swing for Berkshire.�

1/1/2015

guest From discussion in another thread, filed under potential causes for concern......

It's one thing to say Warren Buffett bought NV Energy at the wrong time in 2013, Dominion is willing to do the very same thing today in Utah. Obviously consolidation while valuations are low is going to happen regardless of outlook, I just find this moderately insane.

The minute residential solar gets any foothold in these states companies like NV Energy and Questar become worthless, so what's the logic? Do they really think solar is some kind of fad that can be beaten back?�

1/1/2015

guest Yeah, just like Internet, donchaknow. The Swedish minister for communications became infamous mid-90's when she declared Internet to be just such a fad that wouldn't last very long. Pretty shrewd lady otherwise ...�

1/1/2015

guest This sounds like the over valuation trap. Pretty much all utilities are over valued in the present situation. Management will try to preserve the illusion that their company is worth its valuation. One way to do that is to buy up weaker competitiors. This creates the illusions of dominance and growth. Shareholders are lead to believe that their dividends are secured on a stronger base of business. All this deflects from the fact that utilizes are stuck with a cost structure that requires rates higher than distributed solar. There can be no security in any business model that is so deeply undercut by competing technologies. I suspect that the smart utilities are the ones selling out to the likes of Dominion and NG Energy. They may look weak, but they will walk away with capital that can be reinvested in other areas. Just look a coal. The smart money divested a long time ago. Dumb money will stick around to hire the bankruptcy lawyers.�

1/1/2015

guest Tuck this Elon quote away for Jul/Aug. When Tesla announces powerwall v2, they'll likely announce some trial results. Could be an ah-ha moment for SCTY investors.

�

1/1/2015

guest NV Energy files ideas to soften solar rate hike

looks like NV energy is backtracking a little on their big announcement about grandfathering in existing users�

1/1/2015

guest De-Grandfathering was never going to fly and they knew it. You need to put something batshit crazy out there so you can "compromise" by paying consumers 2.6 cents for wholesale juice at the same time you pay yourself 10 cents.

Bernie and Hillary should be pivoting to Nevada soon, let's hope they make this a major issue.�

1/1/2015

guest http://www.streetinsider.com/dr/news.php?id=11270039

This is a surprising forecast. US solar up 67% in 2016 to 15 GW. 10 GW to utilities, but 5 GW distributed. If SolarCity takes 1/3 of distributed. That would be about 1.67 GW.

I do expect that SolarCity will do quite well in the commercial segment. Killing demand charges with Powerpacks and solar is a winning play for SolarCity. I think commercial can be the surprise segment fir solar as the gap between utility scale and commercial installation costs narrow.�

1/1/2015

guest IIRC the commercial portion of the bar chart was much fatter in the 3Q presentation than in quarters past. Certainly helping drive that $1.92 install cost and should only accelerate. Corporations are waking up to the savings faster than the huddled masses.

I'm not too bullish on 2016 considering most folks were likely ramping down to cut costs then you add in that the pressure is now off to complete projects before the ITC expires. I think both will have a decent muting effect on installs across the board. From there on out it's a rocket to the moon as soft costs trim to grid parity everywhere.

2017 $70's and $80's will still be in the money, but starting to think it's my 2018 $90's that will be the big home run. Hoping 2018's drop before Friday so I can load up again.�

1/1/2015

guest Silver Lining For Natural Gas As EIA Forecasts Price Hike | OilPrice.com

So this is interesting, the US EIA is starting to model forecast that in coming years natural gas and coal will decline in power generation due to advances of renewable energy. This is the sort of fossil offset that I've been talking about. The EIA seems to think that as gas is squeezed out of power generation, it will find higher prices in other markets. This strikes me as magical thinking. Apparently, they are not quite recognizing price competition in the power markets is what is driving down the price of gas. In any case the price may moderate, because currently levels may not be enough to sustain growth in production.�

1/1/2015

guest Options strategy for potential rosy guidance on the earnings call next week? Are we all a bit gun-shy at the moment? Could we get a big pop? Or a big drop like last quarter?�

1/1/2015

guest I have no clue what is happening lately. It seems to me we're just caught in the oil collapse undertow...which seems to me the glut will only get worse with renewables displacing fossil fuels.

I saw this interview which I think makes sense, but I don't know how this effects SCTY. Maybe a strangle?

http://www.cnbc.com/2016/02/02/gartman-pickens-is-wrong-on-oil-heres-why.html�

1/1/2015

guest Anyone with a short interest update?�

1/1/2015

guest Well the Dec 2016 oil future is trading at $40/b. So if you really believe Pickens prognostication of $52/b by year end, you ought to load up on these futures with 30% upside. Serious, Pickens is uttering nonsense. The world is adding oil storage capacity everywhere to buy up this glut. Over 3 billion barrels in inventory. By the end of the year, inventory could easily exceed 3.3 billion even if the market balances. That storage is ready to reverse flow at any price above the futures curve. Storage is currently putting a floor at about $30 and also implies as $40 cap over the next year or so. This is why Gartman can be pretty confident in a $27 to $47 trading range.

Remember storage is now the swing producer for oil.�

1/1/2015

guest I liked the detail that Russia simply can't stop pumping because their Siberian pipelines will freeze up the minute flow stops. There is simply no end in sight for this glut, talk about a global stimulus(for developed non-petro countries).

Back on topic.....no one wants to take a stab at how this quarterly call will be received? SCTY has to have learned their lesson from last quarter and is carefully crafting their language. They are in the enviable position of being able to give very aggressive(and realistic) guidance relative to the tone of last quarter's call. Will they pull the trigger or just keep it bland?

CA net metering is now locked in, ITC is now locked in, grandfathering is all but locked in. I think they go a bit past neutral to the aggressive side spouting positive guidance out toward 2017/18 and we see a nice jump. The idea that this company is fairly valued at $3B is asinine at this point. Give the investment world a glimpse of what 80% growth looks like in 2018.�

1/1/2015

guest Will SCTY recant it's pledge from last earnings call to be cash positive by the end of 2016? That plan was in response to the potential ITC expiration which is now generously extended. If they feel compelled to announce this return to more rapid(expensive) growth will it be taken as a negative on Tuesday's call?

Will the increased revenue projections that go along with that aggressive expansion lift sentiment more than potential continued high sales cost weighs it down?�

1/1/2015

guest All good questions. I hope they give some details on Silevo and where they are at. I feel like this gets way too little coverage from any analyst for something that will be so substantial to the company. Paying 250 million to get a state of the art 1 billion dollar factory is crazy and it got so little coverage. We are actually getting pretty close now to when Solar City starts installing the equipment to make the solar panels. I think Spring of this year is the timeframe with full production (10,000 panels a day) spring of 2017.

I am also very excited to hear more about the Powerwall v2. I hope Elon talks about it in the Tesla Earnings call and does not hold the details quiet until the product launch.�

1/1/2015

guest Ralston Live | Vegas PBS Shows | Vegas PBS

man, Bryan Miller once again represents on this PBS interview show. Says we'll hear soon on lawsuit on gov Sandavol and gave warning of another lawsuit on the PUC if they don't toss out current rate decision after reconsideration next week.

Wow, There are so many other legal and legislative actions in motion now I can't see how nv energy and the Nevada PUC will survive if they go solarcity's way:

-- A state referendum on overturning the PUC recent net metering decision is gathering signatures and looking for a state wide vote in November 2016.

-- A Nevada constitutional amendment to open electricity market and dismantle monopoly structure just filed today.

-- A class action lawsuit(anti-trust)bait and switch on nv energy by two Nevadans now in motion.

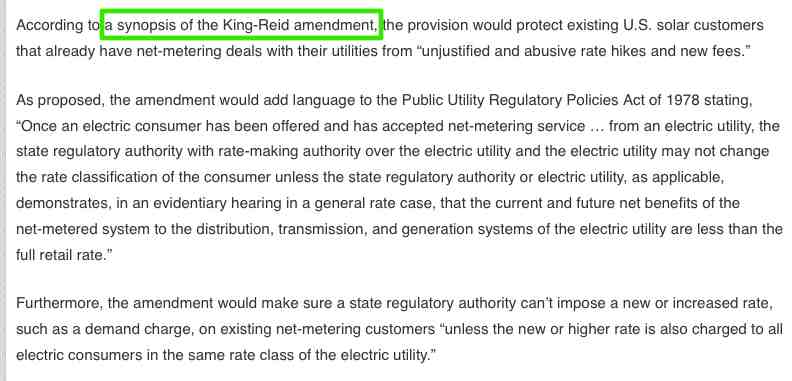

-- Also, the current federal energy bill has a supported amendment to prohibit non grandfathering of net metering customers under agreement terms at time of signing up, and also to ensure commissions assess all benefits before changing retail net metering (senator reid&King).

This is a clear battle ground now. I feel nv energy not only burned solar industry but they have also messed with the casino/gaming industry. Change will happen and nv energy will not like it at all.

I feel there is such a large movement, such a momentum now that we ought to take this as a sign Solarcity and rooftop solar is going to have a winning result after all is said and done over this next year.

I read on more and more Solarcity employees social media that the new mantra is to grow "as fast" as they can. With that, I feel guidance is going to emphasized at the conference call. This guidance ought to give an indication of a longer term outlook, maybe a new look at 2018 goals again. Like the million customer goal affirmation as well as growth rate expectations (40% sustained or increases).

I hope we can start to get solar+storage projections. How many sales they are going to aim for for 2016. This will really be important for breaking through in stock price because we all know this is the "holy grail" for expanding the business into a post NEM centric compensation model, such as grid services. an update on their California aggregation could be helpful here as well.

The tesla powerwall 2.0 is interesting. I'm hopeful Lyndon could give more color by addressing solar+storage sales over the 2016 year. I feel he can be general enough not to look in specific number expectations, but can be explicit enough to assure ramping product offers in applicable markets. I really really think this would impact investors in a positive way to start including energy storage goals in guidance outlooks.�

1/1/2015

guest About the Powerwall 2, I had heard from a long time SolarCity employee that it would be bigger (capacity wise) and cheaper. We'll hopefully find out soon enough. If so, I'll order one.�

1/1/2015

guest If management gives out lofty storage guidance, without provide any detail on the expected ROIs and such, I will throw up on the keyboard.

Storage is cost.

If argument is that grid services will pay for (battery cost + transportation cost + installation costs + profits), that's a load of baloney. Why won't grid get it's own batteries from Musk or wherever else?

As a shareholder, you want storage to be postponed as far away as possible.

With full net-metering, you literally get infinite battery with zero losses (100% 'round trip efficiency' in battery language) for FREE.

Why would you want to ever add costs to the system, when you have this for free??

Jeez, you are the very same people fighting for net-metering, aren't you??

Any mention of storage (other than in the context of HI) in today's world will doom the stock. Expect another 20 to 30% slide on that. Because it means that management is not confident in continuing net metering (free battery).

PS: For clarity, every time a powerwall is sold, Tesla makes money. Guaranteed. Both revenues and profits. It's not some iffy proposition based on some esoteric money falling off sky.

PPS: Did I say this already? As a SC shareholder, you want storage to be postponed away to as far as possible.�

1/1/2015

guest I hear what you are saying Steve. It makes sense. I'd still buy one just because I need a new toy!�

1/1/2015

guest

You are So wrong here! You seem to think that solarcity will install all of this storage for free to the consumer. I think there will make money on every storage system installed before the added on grid Services. So just so we're clear if you're a solarcity shareholder the sooner solar systems are installed with storage the better. Imo anyway.

In unrelated news one of the new public utility commisioners in Arizona will not be voting on any cases that involve solarcity because his son works for solarcity. I'm not sure if this is good or bad it sucks that the one person throw Solar is not going to be voting on anything that has to do with solarcity

Newly appointed Arizona utility regulator to recuse himself from SolarCity cases | Utility Dive�

1/1/2015

guest I'm sure jhm will provide a better analysis but in short, look at the rate plan that California adopted. Even residential solar installation with a battery now is able to arbitrage due to variable rates. It is better than net metering. Even without the battery but with intelligent use of resources one could lower the power bill even further. The trick is it's not that easy to implement and that's where SolarCity has a chance to shine. This is where one needs sophisticated software that predicts spot rates, knows how much sun there is on that day (including the weather forecast), and based on that decides when to charge, when to discharge, and when to run the freezer.�

1/1/2015

guest SolarCity releases report on saving billions in electricity costs - LA Times

Breaking:

Solarcity publishes plan(solar+storage)to potentially save $1.4 billion annually to the California grid

Plan link within just released blog post:

SolarCity Blog�

1/1/2015

guest That would be a valid argument if maintaining status quo for the grid were an American priority. We are more interested in life, liberty and the pursuit of various other fun things. Why does "the grid" have to exist as an entity with feelings rather than just a utility can be morphed into any form suits us best?

I kind of agree here. Going to the "early option" on storage smells like desperation. I'm fine with painting the picture for NV Energy as a threat, but don't start talking implementation until we're at 50-70% of peak demand in these sunny locales.

Relax. The faster we can get to a truly open energy market, the faster solar/wind/storage takes over. As an investor we should probably want a few years of insane solar ramp up with just net metering, but the real revenue comes when the services are needed in the next phase. These guys are just impatient.

This blog post has me very bullish on the Tues call. They're learning PR lessons and taking the right steps. Fingers crossed.�

1/1/2015

guest Any rational reason for this tanking? Good lord I hope the shorts are piling on.

The 2018 options are getting delicious.�

1/1/2015

guest Back to pre-ITC extension levels huh. Damn tempting to convert some stock into LEAPs.�

1/1/2015

guest $80 Jul15 calls $.25? Oh the temptation! Get thee behind me Satan!�

1/1/2015

guest Senate Democrats Block Energy Bill After Republicans Dont Agree To Aid For Flint | Politicus USA

energy bill (federal net metering measures) stalled right now due to flint funding issues with republicans.

solarcity is currently selling storage as back up which is a massive market in itself. However, this is a penetration strategy for future grid services as policies are put in place to open the market, which I posted today's development above.

solarcity solar+storage will offer 13 services to all 3 primary stakeholders on the grid. That's 13 services that have monitary value and Solarcity is helping to price those services in their plan outlined in their blog post pdf.

Commissione picker is willing and ready to move forward on viable data and Solarcity is right there offering it. That is a significant indicator forward progress is happening on grid service pricing for all of us to model.

In the meantime, Solarcity is selling solar+storage as back up. We all know that this is just 1 of 13 services to be priced in. I say again, back up is just 1 of 13. Let's not forget this as these values become integrated into cost structure of adding energy storage to their product offering. It is painfully clear, specifically in California, thst when Solarcity sells these products as back up, that is not the end goal when those systems are in operation. It's like I've said before, the opportunity for "upgrades" are a significant selling point for early adopters of back up. The systems will be set up for software updates to integrate these other 12 services as policies are developed. And as Solarcity has already stated, they have 50/50 revenue share of these added grid services with customers written into their contracts already.

Current stock price is completely divergent to this reality which is extremely interesting for those that like to time entry points in accumulation strategies.�

1/1/2015

guest Observation : SolarCity's white paper has received very little attention and has only been retweeted 15 times. There are currently only 7 people viewing this thread.

We need a few celebrity re-tweets/vocal support to raise awareness and to force politicians to ACT soon. Maybe a comment from Elon?

Investors are waiting for politicians to do the right thing. Many have been spooked or scared out of the market by the recent volatility. Meanwhile Fisher and Musk have been accumulating shares.

Release the Hulk!�

1/1/2015

guest I get bonuses in September, so I hope this thing stays "undiscovered" until then�

1/1/2015

guest Keep in mind that customers want this. So certainly some cost will be borne by the customer. However, for those customers who prefer not to have a battery, I am sure SolarCity will offer solar only systems too. So this is an issue of customer choice. There is no need to project our personal values on all customers. This in fact is the fundamental mistake that opponents of PPAs make. They are personally convinced that solar ownership is so superior to leasing that they fail to see the very simple point that most solar customers actual chose to lease. So let customers chose to add batteries to their system. Many of them will, whether you or I see the value in doing so.

In no way does offering batteries reduce SolarCity's opportunity to sell solar systems. If anything, I expect that offering Powerwalls will increase public interest in solar. So this reduces marketing costs. Second, offering batteries is an up sell opportunity, so revenue per sale will increase.�

1/1/2015

guest Great target I think. Hopefully the spread will be reasonable. I've been thinking next week will be good timing to get ahead of the ER. I guess the market is pricing cheap fuel prices as slowing SCTY growth and some new guidance would be welcome.�

1/1/2015

guest I really enjoy hanging out with and listening to people much smarter than myself, but sometimes feel like a farm boy at an astrophysics convention. I'm wondering if anyone would be willing to spend 5 minutes creating a primer of sorts for those of us with zero investing experience? I found this forum when looking for SolarCity news and it is absolutely one of the best sources on the internet for such news. But I'd love to know more about the investing side, which would probably make following this thread even more interesting than it already is.

What is an option? What's the difference between a 2017 option and a 2018 option?

I have a general idea what stock is, but what are LEAPs? What happens when you convert a stock into a LEAP? What's the upside? What's the downside?

What's a 25� call for $80 on July 15? I'm guessing that the $80 is stock price, but what's the 25� for? And does spending that quarter get you good things if the stock is above $80? What happens if it's not above $80?

For assorted reasons I follow solar in general and SolarCity in particular. I understand the business side of things, but not the investing side of things. I'm also real tempted to buy some of the Solar Bonds available on their website - small return but for a good cause.

If anyone's interested in chiming in and using small words to explain a complex concept, it would be appreciated.�

1/1/2015

guest Moderator Note:

A call to all to follow Forum rules and TOS: Posts in the TMC are your words, which express your thoughts. You are permitted and encouraged to augment them with links to other sites, but a bare link - one with no member input - like the one just excised, are considered rude and an evidence of laziness.�

1/1/2015

guest Whoops, my bad! Was trying to make it easier.

Here's the normal link to khan academy american call options video.�

1/1/2015

guest Californias distributed resources proposal could benefit grid, solar and utilities | PV-Tech

More indication solarcity's solar+storage grid services is moving along and will be entering the wholesale market soon. For those following along, this is fantastic(and exciting) news. Again, there are 13 different services identified from what Solarcity offers with it's products.

Here's a quote from cal ISO (one of the three stakeholders for those services):